The Retirement Gambit: Trump Opens $12 Trillion in 401(k) Funds to Crypto While Half of Bitcoin Is Already Underwater

The Labor Department wants your grandmother's retirement account to hold bitcoin. The timing could not be worse - or, depending on who you ask, more perfect.

The collision between traditional retirement infrastructure and crypto volatility is about to become a $12 trillion experiment. (Pixabay)

On Monday evening, the U.S. Department of Labor dropped a proposed rule that could fundamentally rewire how 150 million American workers save for retirement. The rule, prompted by a Trump executive order from August 2025, would allow 401(k) plans to include cryptocurrencies, private equity, and real estate alongside the traditional stock-and-bond allocations that have defined retirement investing for decades.

The announcement landed on a day when nearly half of all circulating bitcoin was already trading at a loss. When oil closed above $100 per barrel for the first time since 2022. When crypto stocks were down 60% from their highs. When the largest liquid staking protocol in DeFi was proposing a $20 million buyback because its governance token had collapsed 95%.

The timing tells you everything about where crypto sits right now: simultaneously courting the largest pool of passive capital on the planet while drowning in its own stress indicators. This is either the bottom of the market meeting the biggest demand catalyst in crypto history, or it is a government-endorsed invitation for retirement savers to catch a falling knife.

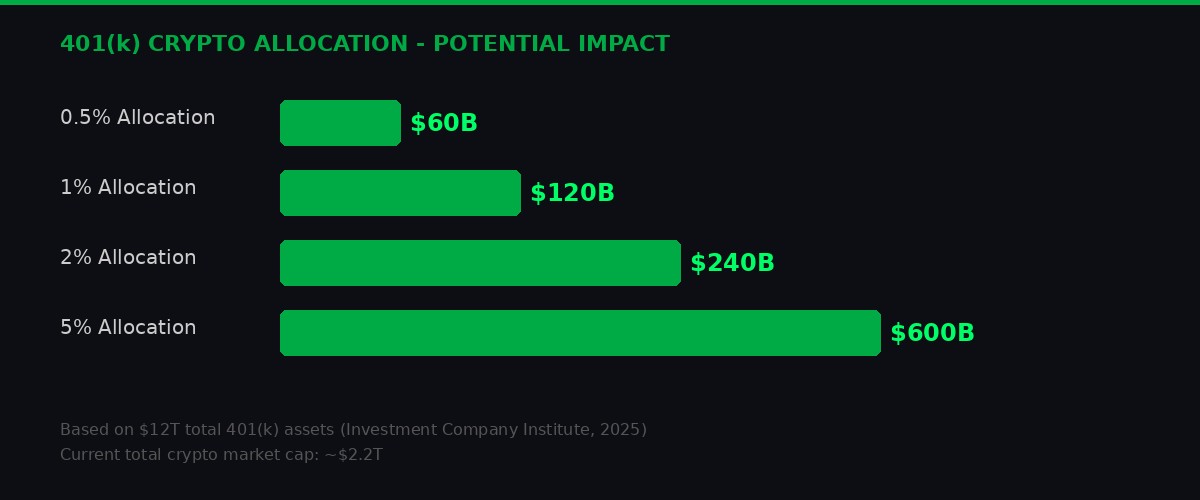

Either way, the numbers involved are staggering. U.S. 401(k) plans hold approximately $12 trillion in assets, according to the Investment Company Institute. Even a 1% allocation shift would represent $120 billion in new capital entering crypto markets - roughly equal to all bitcoin ETF inflows since their January 2024 launch combined.

The Rule: What the Labor Department Actually Proposed

The proposed rule would mark the most significant shift in 401(k) investment options since employer matching became standard. (Pixabay)

Labor Secretary Lori Chavez-DeRemer framed the proposal as a modernization effort. "This proposed rule will show how plans can consider products that better reflect the investment landscape as it exists today," she said in a Department of Labor statement on Monday.

The mechanics are straightforward. Under current rules, 401(k) plan fiduciaries - the people who decide what investment options workers see in their retirement accounts - have been effectively discouraged from including crypto. Previous Labor Department guidance urged "extreme care" before adding digital assets. That guidance was rescinded in May 2025. Trump's August executive order went further, directing the department to treat digital assets on par with other investment options.

Monday's proposed rule is the regulatory machinery catching up to that order. If adopted, it would allow plan providers to include bitcoin, ether, and potentially other crypto assets alongside private equity and real estate in 401(k) investment menus. The rule does not mandate crypto inclusion - it removes the regulatory barriers that prevented it.

The distinction matters. No plan administrator is being forced to add a bitcoin fund to their lineup. But the fiduciary risk of doing so - the legal exposure that kept most administrators away - would be substantially reduced. Plan providers like Fidelity, Vanguard, and Schwab, which collectively manage trillions in retirement assets, would face far less liability for offering crypto-linked options.

ForUsAll, the 401(k) provider that launched a crypto option in 2022 and immediately drew a Labor Department investigation, would go from regulatory pariah to early mover. Companies like Bitwise and 21Shares, which have been building institutional crypto products, would have a massive new addressable market.

The proposal now enters a public comment period. Implementation, if approved, likely comes in late 2026 or early 2027. But the market is already pricing the possibility, and the implications are enormous.

- Total assets: ~$12 trillion (Investment Company Institute, Q4 2025)

- Active participants: ~150 million Americans

- Average balance (age 55-64): $232,710

- Current crypto allocation across all plans: effectively 0%

- Potential 1% allocation shift: $120 billion into crypto markets

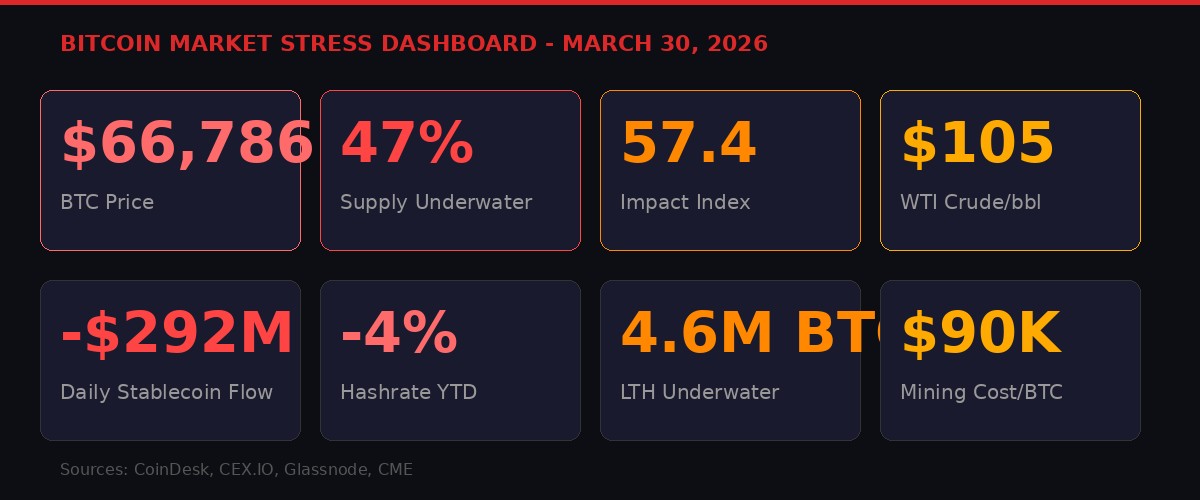

The Underwater Problem: 47% of Bitcoin Supply Is in the Red

The Bitcoin Impact Index hit 57.4 last week - deep in the "high impact" zone that preceded double-digit crashes in 2018 and 2022. (BLACKWIRE)

The rule arrives at a moment of extraordinary stress across the crypto market. According to data published by CEX.IO on Monday, 47% of all circulating bitcoin is currently held at a loss. The Bitcoin Impact Index, which measures financial stress across user cohorts based on onchain behavior, ETF activity, and liquidity flows, surged 13 points last week to 57.4 - its steepest weekly climb since January.

That reading places the market squarely in what analysts call the "high impact" zone. Historically, readings at this level have preceded double-digit price drops. Similar readings appeared in mid-2018, before bitcoin fell from $6,000 to $3,200. They appeared again in mid-2022, before the collapse from $30,000 to $15,000.

Long-term holders - wallets that have held bitcoin for more than six months, the supposed "diamond hands" of the market - are now selling at a loss. Over 4.6 million BTC from these wallets, roughly 30% of their total holdings, are underwater. Their realized losses last week were the worst since 2023. This is not short-term speculators panic-selling. This is conviction evaporating.

The capital flow picture is equally grim. Daily stablecoin net flows, which had averaged inflows of $250 million earlier in March, flipped to outflows of $292 million. ETFs shifted from accumulation to distribution. Miners, squeezed by production costs nearly $23,000 above spot price, moved from holding to selling.

"This kind of divergence between price action and on-chain conviction has historically been a warning sign. Similar moves occurred in mid-2018 and mid-2022 before price drops of over 25%." - CEX.IO Research

One piece of data offers faint reassurance: holders are not yet rushing to deposit BTC on exchanges en masse. That behavior - the mass migration to exchange wallets ahead of selling - typically marks full capitulation. It hasn't happened. The market is stressed, bleeding, losing conviction, but it hasn't panicked. Not yet.

For the 401(k) proposal, the timing creates a paradox. Critics will point to a market where half the supply is underwater and argue this is exactly the wrong moment to expose retirement savers to crypto. Advocates will counter that buying when half the supply is at a loss is precisely what long-term value investing looks like. Both sides have data on their side. Neither is wrong.

Oil at $105, Powell at Harvard, and the Macro Squeeze

WTI crude closed above $100 per barrel - the first close above that level since 2022 - adding a new layer of pressure to risk assets. (Pixabay)

The crypto market's problems are not isolated. They exist within a macro environment that is actively hostile to risk assets. WTI crude oil closed Monday at just shy of $105 per barrel, up 5.3% on the day. While oil has traded above $100 intraday since the Iran conflict began in early March, Monday marked the first closing price above $100 since 2022.

Oil above $100 is not just a number. It's an inflation accelerant. It raises input costs across every sector of the economy. It threatens consumer spending. And it puts the Federal Reserve in a position where holding rates steady starts to look like a policy error.

Fed Chairman Jerome Powell, speaking at Harvard University on Monday, tried to thread the needle. He said the central bank is "looking past short-term oil price shocks" and that inflation expectations remain "well anchored." The bond market liked what it heard - the 10-year Treasury yield fell nine basis points to 4.35%, and rate hike odds collapsed from 25% to 5% on CME FedWatch.

But Powell's reassurance came with a tell. "We will eventually maybe face the question of what to do here," he said. "We're not really facing it yet because we don't know what the economic effects will be." That is not the language of a central banker who is confident the problem will resolve itself. It is the language of someone buying time.

Despite Powell's soothing words, stocks couldn't hold their early gains. The Nasdaq closed down 0.75%. The S&P 500 fell 0.4%. Bitcoin, which had bounced earlier in the session, retreated to $66,500, flat over 24 hours. The pattern is becoming familiar: a hopeful morning, a grinding afternoon selloff, and a close that leaves bulls with nothing.

The macro setup for crypto is as follows: oil is rising because of a war that shows no signs of ending. The Fed is on hold but nervous. Bond yields are elevated. Stablecoin flows are negative. And the government wants to open the floodgates of retirement capital into this environment. The tension between those facts is the entire story of Q2 2026.

The Great Mining Exodus: Hashrate Falls, AI Rises

Mining bitcoin currently costs $23,000 more per coin than the spot price - an unsustainable gap driving the largest infrastructure pivot in crypto history. (BLACKWIRE)

For the first time in six years, bitcoin's hashrate - the total computational power securing the network - declined during the first quarter. The metric is down approximately 4% year-to-date, hovering around 1 zettahash per second (ZH/s), according to Glassnode data.

To appreciate how unusual this is, consider the trend it broke. Over the previous five years, hashrate surged from roughly 100 exahashes per second to 1 zettahash - a tenfold increase. Every single first quarter saw growth. Full-year growth consistently exceeded 10%. In 2022, the hashrate nearly doubled.

The Q1 2026 decline is not a blip. It is the direct consequence of catastrophic mining economics. With production costs averaging $90,000 per bitcoin and the spot price at $66,786, miners are losing roughly $23,000 on every coin they produce. No business model survives those margins for long.

The response has been a mass migration to artificial intelligence infrastructure. Publicly listed mining companies - which account for over 40% of global hashrate - are redirecting capital from mining rigs to GPU clusters optimized for AI workloads. The returns are higher, more predictable, and don't depend on a volatile commodity price.

This transition is being funded two ways: through debt issuance and through selling bitcoin reserves. Both channels reduce reinvestment into mining capacity. The result is a network that is becoming more sensitive to price - if bitcoin falls further, more miners exit, hashrate drops again, and the security of the network theoretically weakens.

There is a counterargument. The concentration of hashrate among large U.S. public companies has been a growing concern for decentralization advocates. If Marathon, Riot, and CleanSpark pivot to AI, smaller and more geographically distributed miners fill the gap. The network becomes less powerful in aggregate but potentially more resilient to coordinated disruption. Whether that trade-off is worth it depends on your threat model.

For the 401(k) conversation, the mining exodus raises a practical question: if the companies that secure the bitcoin network are abandoning bitcoin mining for AI profits, what does that say about the long-term viability of the asset class that retirement plans are now being invited to embrace?

Lido's $20 Million Buyback and the DeFi Governance Reckoning

The largest liquid staking protocol in DeFi controls 23% of all staked ETH but trades at a $258 million market cap after a 95% collapse. (BLACKWIRE)

While the 401(k) debate plays out in Washington, the DeFi sector is confronting its own existential crisis. Lido DAO, the largest liquid staking protocol on Ethereum, has proposed spending up to 10,000 stETH - roughly $20 million - to buy back its own governance token after a 95% crash from its 2021 peak.

LDO hit an all-time low of $0.27 on March 7 and currently trades near $0.30 with a market capitalization of approximately $258 million. The numbers create an absurd contrast: Lido controls roughly 23% of all staked ether on Ethereum, generates consistent protocol fees, and holds billions in total value locked. Its governance token is worth less than a mid-tier NFT project at the 2021 peak.

The buyback itself exposes a deeper problem. Lido's governance team wanted to execute the purchase onchain - the DeFi-native approach. But onchain LDO liquidity sits at about $90,000 of depth at plus-or-minus 2%. A single 1,000 stETH batch would blow through available liquidity multiple times over. The protocol that pioneered decentralized staking has to route through Binance, OKX, and Bybit to buy its own token.

"This is not a routine fluctuation. It represents one of the most significant dislocations between LDO's market price and its underlying protocol fundamentals in the token's history." - Lido Ecosystem Operations proposal

The execution plan is cautious: 1,000 stETH batches, each requiring a separate governance motion with a three-day objection period. Slippage is capped at 3%. The Growth Committee controls timing to avoid front-running - though with the proposal publicly visible on the Lido governance forum, the market already knows the DAO is stepping in as a buyer.

LDO's collapse is not an outlier. It represents a category-wide repricing of what DeFi governance tokens are worth. These tokens control fee switches, treasury allocations, and protocol parameters, but most distribute nothing to holders. They are equity-like instruments with none of the cash flow rights. The market has spent 18 months systematically devaluing them, and Lido's buyback is an admission that the market might be right - or at least that organic demand won't save the price.

Meanwhile, Aave rolled out its v4 upgrade on Ethereum on Monday, pushing into real-world credit markets after two years of development. The upgrade separates different types of lending markets while sharing liquidity pools, enabling everything from traditional crypto lending to institutional borrowing against real-world assets. Aave founder Stani Kulechov framed it as DeFi's next evolution: "A lot of these opportunities will come from value outside of DeFi."

The juxtaposition is stark. Aave is building infrastructure for institutional adoption while Lido is doing buybacks to stop its token from going to zero. Both protocols are essential to Ethereum's ecosystem. Both are struggling to translate utility into token value. The 401(k) proposal would bring new capital into this space, but it won't solve the fundamental question of whether governance tokens deserve any value at all.

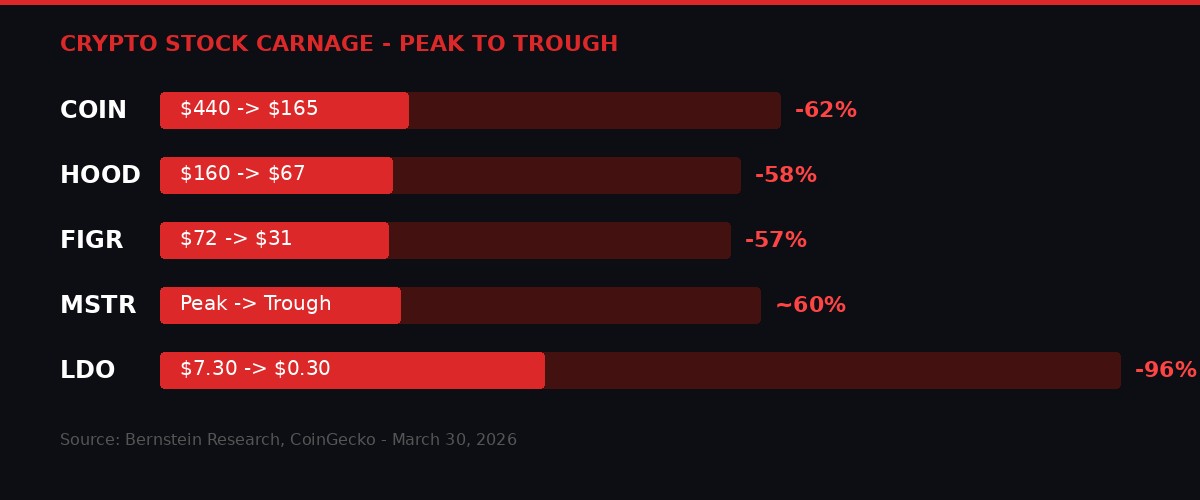

Crypto Stocks at 60% Discounts: Bernstein's "Big Business at Big Discount" Call

Crypto equities have shed roughly 60% from their October 2025 peaks - Bernstein calls it a buying opportunity. (BLACKWIRE)

Wall Street is starting to position. Bernstein, the research broker, published a note Monday calling the 60% crash in crypto-linked equities a "rare chance to buy the dip at a big discount." Analysts led by Gautam Chhugani maintained outperform ratings on Coinbase (COIN), Robinhood (HOOD), and Figure (FIGR) while lowering price targets across the board.

The revised targets tell the story of how much has changed. Coinbase's target dropped from $440 to $330 - a 25% cut - against a current trading price of $165.50. That still implies roughly 100% upside, but the fact that a bull case requires the stock to double shows how deep the damage runs. Robinhood's target fell from $160 to $130 against a $67 price. Figure went from $72 to $67 against $31.

Bitcoin itself has fallen roughly 40-50% from its record high near $126,000 set in October 2025. The broader digital asset market has shed approximately $2 trillion in total value. The selloff has been driven by a familiar cocktail: macro headwinds from the Iran conflict and oil shock, regulatory uncertainty despite the pro-crypto executive orders, and the unwinding of leverage that built up during the 2024-2025 bull run.

Bernstein's thesis rests on a floor forming into Q1 earnings. The broker expects near-term weakness to persist through first-quarter results but views current levels as an entry point into companies with exposure to stablecoins, tokenization, prediction markets, and derivatives - sectors the broker believes will grow regardless of bitcoin's price trajectory.

The firm reiterated its $150,000 year-end bitcoin price target last week, arguing that bitcoin has likely found its bottom. At $66,786, that target implies more than 120% upside in nine months. It's a bold call. But Bernstein has been among the more accurate Wall Street voices on crypto over the past two years, and their willingness to maintain the target through a 50% drawdown at least signals genuine conviction rather than target-chasing.

The 401(k) rule, if adopted, would be a significant catalyst for the companies Bernstein is recommending. Coinbase and Robinhood would be the primary platforms through which retirement accounts access crypto. Fidelity, which already offers a bitcoin 401(k) option through its digital assets arm, would scale that product dramatically. The market is pricing zero probability of the 401(k) rule into crypto equities right now. If that changes, the re-rating would be violent.

Strategy Pauses, BitMine Loads: The Corporate Treasury Split

While Strategy ended its 13-week bitcoin buying streak, BitMine made its largest ether purchase of 2026 - the corporate treasury divergence is widening. (Pixabay)

The corporate crypto treasury landscape split wide open this week. Strategy (MSTR), the Michael Saylor-led company that became synonymous with corporate bitcoin accumulation, broke a 13-week buying streak. No bitcoin purchased last week. No announcement. Just silence from the most vocal corporate bitcoin advocate in the market.

Meanwhile, BitMine Immersion Technologies (BMNR), chaired by Fundstrat's Tom Lee, made its largest weekly ether purchase of 2026: 71,179 ETH worth approximately $143 million. The company has accelerated buying for four consecutive weeks, pushing total holdings past 4.73 million ETH - roughly 3.92% of ether's total supply. Total crypto and cash holdings now stand at $10.7 billion.

The divergence is significant because it reveals a philosophical split in how corporate treasuries are approaching the crypto downturn. Strategy has been the anchor buyer for bitcoin through every dip since 2020. Its absence from the market, even for one week, sends a signal. Saylor hasn't commented on the pause, and it may prove temporary - but in a market this fragile, the largest buyer stepping away is noticed.

BitMine's accelerating ETH purchases represent a different thesis entirely. Where Strategy treats bitcoin as digital gold - a store of value to be accumulated indefinitely - BitMine is betting on Ethereum's transition from speculative asset to yield-bearing infrastructure. Staking rewards, DeFi fee generation, and the Aave v4 expansion into real-world assets all support the idea that ETH produces something beyond price appreciation.

Tom Lee's willingness to increase buying pace as the market deteriorates is either informed contrarianism or institutional stubbornness. He has called the current environment "the final phase of a downturn," citing rising oil prices and geopolitical tension as temporary headwinds. If he's right, BitMine is accumulating at generational lows. If he's wrong, a single company holding 3.92% of ETH supply creates concentration risk that could amplify any future selloff.

For 401(k) investors, the corporate treasury story matters because it demonstrates what institutional conviction looks like in practice. These are not retail traders buying dips with spending money. These are publicly traded companies deploying hundreds of millions in shareholder capital based on multi-year thesis. The question is whether that conviction is evidence of value or evidence of capture.

Elizabeth Warren's Warning and the Political Fault Line

The political battle over retirement funds and crypto is just beginning - the comment period will be one of the most contested in Labor Department history. (Pixabay)

The 401(k) proposal did not arrive without opposition. Senator Elizabeth Warren, crypto's most persistent congressional critic, issued a statement within hours. "As cracks emerge in the private credit market, private equity returns fall to 16-year lows, and crypto keeps tumbling, President Trump has decided now is the time to stick all of these risky assets into Americans' 401(k)s," Warren said.

Her warning carries weight beyond the usual partisan sparring. Private credit markets have indeed shown stress in 2026, with default rates climbing and redemption gates activating at several major funds. Private equity returns are weak. Crypto is in a sustained downturn. Bundling all three asset classes into a single rule change that opens them to retirement accounts gives critics a legitimate complaint about risk stacking.

The deeper political conflict is about who benefits. The crypto industry has spent heavily on lobbying and campaign contributions to both parties, though disproportionately to Republicans in the current cycle. Opening 401(k) plans to crypto doesn't just create a new investor base - it creates a new constituency. Once 50 million Americans hold bitcoin in their retirement accounts, the political cost of regulating crypto harshly becomes enormous. It is constituency capture through financial exposure.

Democrats separately pushed back on another front Monday. Dozens of House and Senate Democrats sent a letter to the CFTC and the Office of Government Ethics asking them to remind federal employees that insider trading on prediction markets is illegal. The letter was prompted by what members described as "a rash" of suspicious activity on platforms like Kalshi and Polymarket, where federal employees may be trading on information they have access to through their government roles.

The two stories are connected. The 401(k) rule expands retail access to crypto. The prediction market letter highlights the risks of expanding access without adequate guardrails. One opens the door. The other points out that the hallway is full of trip wires.

The comment period for the 401(k) proposal will likely be one of the most contested in Labor Department history. The crypto industry will flood the docket with supportive comments. Consumer protection groups will do the same with objections. The outcome will depend less on the merits of the arguments than on the political will of an administration that has already shown it views crypto adoption as both a policy goal and a political strategy.

The $120 Billion Question: What Happens If the Rule Passes

Even a 1% allocation shift from 401(k) plans would inject $120 billion into crypto - equal to all bitcoin ETF inflows since their 2024 launch. (BLACKWIRE)

The math is simple and the implications are not. U.S. 401(k) plans hold approximately $12 trillion. Total retirement assets including IRAs, defined benefit plans, and other vehicles exceed $40 trillion. The 401(k) rule is the first crack in the wall, and if it succeeds, IRA rules will follow.

At a 1% allocation, $120 billion flows into crypto. To put that number in context: bitcoin's total market capitalization is roughly $1.3 trillion. Bitcoin spot ETFs in the United States hold approximately $60 billion. A 1% 401(k) allocation would double the institutional footprint in bitcoin overnight.

At 2%, you're looking at $240 billion - more than the entire market capitalization of ether. At 5%, the number reaches $600 billion, roughly a quarter of all crypto market value. These are not fantasy numbers. Fidelity's internal research on crypto allocations has historically suggested 1-3% portfolio weights for long-term investors. If that guidance becomes the default recommendation for 401(k) plans, the flow numbers land squarely in this range.

The demand wouldn't arrive all at once. Plan administrators need to select products, negotiate fees, update enrollment documents, and educate participants. The rollout would take 12-18 months after the rule is finalized. But the anticipation effect - the market pricing in future flows - would begin immediately.

There's a parallel to what happened with bitcoin spot ETFs in late 2023 and early 2024. Bitcoin rallied from $25,000 to $73,000 largely on the expectation that ETF approval would unlock institutional demand. The actual ETF flows, when they came, were significant but not transformative. The anticipation was the trade. The same dynamic could play out with 401(k) adoption - a rally driven by the expectation of retirement capital, followed by a more modest impact when the money actually arrives.

The risk is that the rule passes, retirement savers allocate to crypto, and then the market does what it has done in every previous cycle: crashes 80%. The 2022 bear market wiped out $2 trillion in crypto value. If 401(k) holders had been exposed at the peak, the political and economic fallout would have been immense. Warren's warning about "sticking risky assets into Americans' 401(k)s" is not just rhetoric. It is a description of a plausible scenario that has already happened twice in crypto's short history.

The counterargument is that 401(k) participants in traditional equity markets experienced a 34% drawdown in March 2020, a 20% drawdown in 2022, and a 57% drawdown in 2008-2009. Risk is not unique to crypto. The question is whether retirement investors understand the magnitude of crypto-specific risk and whether plan administrators will build appropriate guardrails - allocation caps, automatic rebalancing, cooling-off periods - to contain it.

The Convergence: Where All the Threads Meet

The convergence of retirement capital, market stress, and infrastructure shifts will define crypto's next chapter. (Pixabay)

Step back from the individual stories and the picture comes into focus. The 401(k) rule is the demand catalyst. Bitcoin's underwater supply is the price signal. Oil at $105 is the macro headwind. The mining exodus to AI is the infrastructure shift. Lido's buyback and Aave's v4 are the DeFi bifurcation between protocols building for the future and protocols fighting for survival. Strategy's pause and BitMine's acceleration are the institutional divergence. Warren's opposition is the political resistance.

All of these threads are converging in Q2 2026. The outcome depends on which force proves stronger: the structural demand from retirement capital and institutional adoption, or the cyclical pressure from oil shocks, rate uncertainty, and the simple fact that half the market is already losing money.

History offers imperfect guidance. Every previous crypto cycle featured a demand catalyst that seemed transformative at the time. ICOs in 2017. DeFi Summer in 2020. NFTs in 2021. Spot ETFs in 2024. Each brought new capital, new participants, and new narratives. Each was followed by a crash that eliminated the marginal buyers and reset the market back to its fundamental base.

The 401(k) catalyst is different in one important respect: the capital is sticky. Unlike retail traders who can sell in seconds, 401(k) contributions are automated, recurring, and psychologically anchored to retirement timelines measured in decades. Dollar-cost averaging into bitcoin through a 401(k) is structurally different from buying a meme coin on Robinhood. It is slower, steadier, and less prone to panic selling.

That structural difference could break the cycle. Or it could simply mean that the next crash traps capital instead of flushing it. Time will tell. What is certain is that the largest pool of passive savings in the world just moved one step closer to crypto, and the market it's about to enter is bleeding from every indicator that matters.

Bitcoin closed Monday at $66,786. The 401(k) proposal is in public comment. Oil is above $100. Half the supply is underwater. The hashrate is falling. DeFi governance tokens are dying. And someone in Washington just decided that your retirement account should have access to all of it.

Welcome to Q2 2026.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram