Bitcoin futures liquidations hit $299M in 24 hours after Trump's Saturday Iran ultimatum. Photo: Pexels

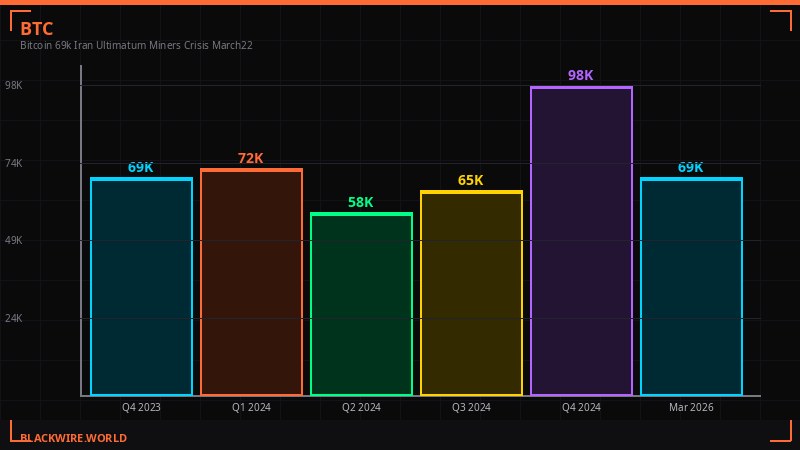

Last week looked like a recovery. Eight consecutive green days, a weekly high of $75,912, and a Fed meeting that delivered the dovish pivot traders had been hoping for. By Saturday night, all of it was gone.

President Trump's 48-hour ultimatum to Iran - demanding the reopening of the Strait of Hormuz or facing strikes on power infrastructure - landed on markets that had spent the entire week getting long. The positioning was extreme. When the headline hit, there was no cushion.

$299 million in liquidations across 84,239 traders. 85% of that coming from long positions. Bitcoin down 2.2% to $69,192. The largest single liquidation was a $10 million BTC-USDT swap on OKX. That is not a market dip. That is a market telling you it was not ready for what just happened.

Liquidation breakdown by asset, March 22, 2026. Source: CoinGlass

The Ultimatum That Broke the Rally

The Iran-Strait of Hormuz standoff is now directly shaping crypto market structure. Photo: Pexels

The sequence of events matters here, because it explains both how badly the market was positioned and how quickly sentiment reversed. On Friday, Trump said he was thinking about "winding down" the military operation against Iran. Markets took that as signal. Eight days of green candles had already priced in a ceasefire narrative, and the "winding down" comment felt like confirmation.

Twenty-four hours later, the script flipped completely. Trump posted that he would "hit and obliterate" Iran's power plants - starting with the largest - if the Strait of Hormuz was not reopened to commercial shipping. That is not winding down. That is threatening to target civilian infrastructure for the first time in the conflict. [Source: CoinDesk, March 22, 2026]

The 48-hour clock started ticking Saturday evening. That means the deadline arrives Monday evening U.S. time - directly into the next trading week's open. Iran has given no indication it will comply. The market is now staring at the real possibility of direct strikes on Iranian power plants, which would be a qualitative escalation from anything seen so far in the conflict.

For crypto markets specifically, the positioning going into the weekend could not have been worse. Traders had piled into long positions after eight straight days of gains and a Fed meeting that leaned dovish. The put/call ratio was already at record highs - a sign that sophisticated players were hedging - but spot buyers and futures traders had been chasing upside all week. When the headline broke, the liquidation cascade was mechanical and fast.

The altcoin damage was broad and proportional. Ether dropped 1.8% to $2,114. XRP lost 2.5% to $1.41. BNB slid 1.4% to $633. Solana fell 2.1% to $88.55. Dogecoin took 2.7% out. The only major assets that managed to stay positive on the week were Ether at +0.8% and Solana at +0.7%. Everything else closed the seven-day window in the red. [Source: CoinDesk Market Data, March 22, 2026]

Major crypto assets performance snapshot, March 22, 2026. Source: CoinDesk / CoinGlass

Miners Are Bleeding: The $19,000 Gap That Cannot Last

Bitcoin mining economics have reached a critical breakdown point. Miners absorbing $19K loss per coin mined. Photo: Pexels

The Iran conflict is not just a headline risk for traders. It is an existential threat to bitcoin's mining sector, and the numbers have reached a level that cannot be sustained for much longer.

Checkonchain's difficulty regression model - which estimates average production costs using network difficulty and energy inputs - pegged the cost of producing one bitcoin at $88,000 as of March 13. Bitcoin was trading at $69,192 on Sunday. That is a gap of nearly $19,000 per coin. The average miner is operating at a 21% loss on every single block they mine. [Source: CoinDesk / Checkonchain, March 22, 2026]

This is not new stress. The cost squeeze started building in October when bitcoin crashed from $126,000 down through $70,000. But the Iran war accelerated every component of the problem. Oil above $100 feeds directly into electricity costs for mining operations, particularly the estimated 8-10% of global hashrate operating in energy markets sensitive to Middle Eastern supply dynamics. The Strait of Hormuz handles roughly 20% of the world's oil and gas flows. As long as it stays closed to most commercial traffic, energy costs stay elevated, and mining margins stay negative.

The network is already showing structural stress. Difficulty dropped 7.76% on Saturday to 133.79 trillion - the second-largest negative adjustment of 2026 after February's 11.16% plunge during Winter Storm Fern. Difficulty is now nearly 10% below where it started the year and far below November 2025's all-time high of approximately 155 trillion. [Source: CoinDesk, March 22, 2026]

Bitcoin miner production cost vs spot price breakdown. Source: Checkonchain / Luxor Hashrate Index

Hashrate has retreated to roughly 920 EH/s, well below the record 1 zetahash level reached in 2025. Average block times during the last epoch stretched to 12 minutes and 36 seconds - 26% slower than the 10-minute target. Hashprice, the metric tracking expected miner revenue per unit of computing power, is hovering around $33.30 per petahash per second per day according to Luxor's Hashrate Index. That is near breakeven for most hardware and not far from the all-time low of $28 hit on February 23.

"When miners can't cover costs, they sell bitcoin to fund operations. That selling adds supply pressure to a market already dealing with 43% of total supply sitting at a loss, whales distributing into rallies, and leveraged positioning dominating price action." - CoinDesk analysis, March 22, 2026

Mining economics are not just a mining story. They are a market structure story. Forced selling from unprofitable miners creates a baseline of supply pressure that operates independently of sentiment or macro factors. When 43% of circulating supply is already underwater, adding forced miner selling into the mix is a structural headwind that does not go away when the headlines calm down.

Publicly traded miners have been adapting by diversifying into AI and high-performance computing, which offer more predictable revenue streams. Marathon Digital, Cipher Mining, and others have been building out data center capacity alongside their mining operations. But that pivot takes time and capital, and the immediate economics are still brutal. The next difficulty adjustment is projected for early April and is expected to decline further according to CoinWarz data. If bitcoin stays below $88,000 - and there is no sign of a return to that level in the near term - the miner exodus continues.

Options Markets Are Screaming: VanEck Documents Extreme Fear

Bitcoin options markets are pricing extreme fear - put premiums at all-time highs relative to spot volume. Photo: Pexels

The liquidation data tells you what happened in the past 24 hours. The options data tells you what sophisticated investors have been expecting for weeks. And right now, they are as defensive as they have been since the June 2021 China mining crackdown.

VanEck's mid-March 2026 Bitcoin ChainCheck documents the full scope of the defensive positioning. The put/call open interest ratio averaged 0.77 over the period and peaked at 0.84 - the highest level since June 2021. Bitcoin's 30-day average price fell 19% from the prior period. Realized volatility dropped from approximately 80 to just above 50. Futures funding rates eased to 2.7% from 4.1%. [Source: VanEck Bitcoin ChainCheck, March 21, 2026]

Bitcoin options sentiment data from VanEck's mid-March ChainCheck report. Source: VanEck

Traders spent approximately $685 million on put options over the past 30 days. Call premiums fell 12% to approximately $562 million. Relative to spot volume, put premiums reached roughly 4 basis points - an all-time high in VanEck's data.

"Relative to spot volume, put premiums reached an all-time high of roughly 4 basis points, roughly 3x the levels seen in mid-2022 following the Terra/Luna stablecoin collapse and the Ethereum staking liquidity crisis." - VanEck Bitcoin ChainCheck, March 2026

To put that in perspective: investors are currently paying more for downside insurance relative to spot volume than they were during the collapse of the entire Terra/Luna ecosystem, which wiped out approximately $60 billion in market value in seventy-two hours. That is the baseline of fear embedded in the current options market.

VanEck's historical analysis offers a contrarian read on what this level of fear implies for forward returns. Looking at the past six years, similar put/call skew readings were followed by average bitcoin gains of 13% over 90 days and 133% over 360 days. The logic is straightforward: extreme hedging means the bad news is priced, and there is limited incremental selling from investors who have already bought insurance. But that historical pattern was established in a market without an active geopolitical war disrupting energy supply. Whether it holds in the current environment is an open question.

The onchain data adds context to the bearish options positioning. VanEck notes that onchain activity has remained weak while miner selling - despite the brutal economics - is actually contained relative to historical stress periods. That muted miner selling might seem counterintuitive given the $19,000 per coin loss, but it reflects the strategic reality: miners who sell aggressively into a weak market accelerate their own pain. Many are choosing to hold, borrow against inventory, or pivot to AI compute rather than dump spot.

Gold's Bear Market - The Other Safe Haven Failing at the Worst Time

Gold is approaching a technical bear market despite escalating Middle East tensions - a significant breakdown of its traditional role. Photo: Pexels

The story that does not get enough attention this weekend is what is happening to gold. The yellow metal - traditionally the go-to safe haven in geopolitical crises - is approaching a technical bear market, down nearly 20% from its January all-time high. That number is remarkable given the context: an active Middle East war, a Strait of Hormuz closure disrupting global energy supply, and a U.S. president threatening to strike civilian infrastructure.

Gold should be exploding in this environment. Instead, it is in freefall. What happened?

The mechanism is clear even if the magnitude is surprising. Markets have repriced the interest rate outlook dramatically since the conflict began. Rate cuts are now largely pushed out of 2026 entirely, with policy expected to remain restrictive through December 2026. The primary driver is the same war that should theoretically be boosting gold: rising oil prices are adding upward pressure on inflation, which reinforces the higher-for-longer rate environment. Higher real rates are the single biggest structural headwind for gold, which produces no yield. The conflict has created a self-defeating dynamic for gold's traditional safe-haven thesis. [Source: CoinDesk Markets, March 22, 2026]

On an M2 money supply-adjusted basis, gold is trading near levels seen at major historical peaks in 1974 and 2011, when it was $200 and $1,800 per ounce respectively. On this liquidity-adjusted basis, gold appears to be consolidating at elevated levels rather than breaking down structurally. But try telling that to a spot trader watching a 20% drawdown from the high.

Bitcoin has actually shown relative resilience in the M2-adjusted framework. Relative to M2, bitcoin remains in a consolidation phase similar to 2024, still retesting its 2021 highs on a liquidity-adjusted basis. Historically, each cycle has seen bitcoin move above prior peaks when adjusted for money supply. With bitcoin still approximately 40% below its October high, this framework suggests a typical consolidation range before potential further upside. But that is a twelve-month thesis playing out against a seventy-two-hour geopolitical timeline that is about to reach a hard deadline Monday evening.

"Gold is nearing a technical bear market despite geopolitical tensions, as higher interest rate expectations and inflation pressures from rising oil prices reduce its appeal." - CoinDesk / James Van Straten, March 22, 2026

The gold-bitcoin correlation has also shifted in a noteworthy way. Gold traded in lockstep with bitcoin tick-for-tick after breaking down from $5,000 on Wednesday, showing positive correlation after weeks of divergence. This suggests the two assets are now responding to the same macro variables - real rates and liquidity - rather than operating as independent safe havens with different investor bases. When they correlate to the downside like this, there is no diversification benefit between them, which is a problem for any portfolio trying to hedge market risk through precious metals and crypto simultaneously.

Ethereum's Existential Quarter: Quantum, Fragmentation, and the Trust Layer Bet

Ethereum faces three simultaneous structural challenges in early 2026: L2 fragmentation, quantum threats, and leadership uncertainty. Photo: Pexels

While bitcoin's weekend crisis dominated the headline flow, Ethereum has been quietly accumulating its own set of problems - and these ones are structural rather than geopolitical. The Ethereum ecosystem is navigating three simultaneous challenges that go to the heart of what the network is supposed to be: the L2 fragmentation debate, an accelerating quantum computing threat, and leadership turbulence at the Ethereum Foundation.

The L2 debate exploded into the open when Vitalik Buterin delivered a pointed critique of the rollup ecosystem earlier in 2026: "You are not scaling Ethereum." The comment cut through a largely celebratory conversation around layer-2 networks. Rollups have processed more transactions, fees have come down, and activity has spread across dozens of networks. But Buterin's argument was sharper than general skepticism about progress. [Source: CoinDesk, March 22, 2026 / Vitalik Buterin, February 2026]

Ethereum's three simultaneous structural challenges in 2026. Source: BLACKWIRE analysis

Many current L2 designs rely on centralized components and operate in siloed environments that do not fully inherit the security guarantees of Ethereum's base chain. In Buterin's framing, scaling that sacrifices decentralization is not Ethereum scaling - it is something else wearing Ethereum's brand. The fragmentation across L2 networks, inconsistent security assumptions, and centralized components are beginning to look less like temporary trade-offs and more like structural risks to Ethereum's core value proposition as a shared, neutral settlement layer.

The quantum threat adds a second layer of urgency. The Ethereum Foundation has elevated quantum computing from a distant academic concern to near-term planning priority, folding efforts like LeanVM and post-quantum signature schemes into active development roadmaps. The implication is significant: the network is no longer just building for the next market cycle but defending against threats that could fundamentally break its cryptographic assumptions. Buterin has also outlined a roadmap to protect the blockchain from long-term quantum risks, establishing dedicated research efforts focused specifically on post-quantum security. [Source: CoinDesk Tech, February 2026]

The leadership dimension arrived without warning. The departure of Tomasz Stańczak as co-executive director of the Ethereum Foundation marked a significant internal disruption. Stańczak had only stepped into the role approximately a year earlier, following the long-standing tenure of Aya Miyaguchi. In an ecosystem that favors continuity and slow consensus, the rapid turnover signaled a deeper recalibration, particularly when it comes at a moment when the foundation is facing technical, strategic, and philosophical reevaluations simultaneously.

Against all this structural turbulence, the Ethereum Foundation has staked a bold claim on its long-term direction: the network should become the "trust layer" for artificial intelligence. Buterin outlined how Ethereum could play a foundational role in the AI ecosystem - not through payments or DeFi, but as a coordination layer for decentralized AI systems enabling verifiable outputs, trust-minimized data sharing, and machine-to-machine economic activity. The foundation's decentralized AI research unit, launched in September 2025, has accelerated into something more deliberate in 2026. [Source: CoinDesk Tech, March 2026]

ETH's market performance reflects the uncertainty. Down 1.8% to $2,114 on Sunday, only marginally positive on the week at +0.8%, and still far from the highs of 2025. The asset is caught between short-term market pressure and long-term narrative construction that has not yet translated into price action. For ETH bulls, the thesis is clear but the timeline is unclear. For bears, the simultaneous pressures on the network are a more immediate concern than any AI vision.

SEC Drops Crypto Taxonomy - Clarity Arrives With Asterisks

The SEC and CFTC published joint interpretive guidance on crypto asset categories this week - the most specific regulatory framework in U.S. history for digital assets. Photo: Pexels

The first concrete regulatory clarity on crypto's security status in years dropped this week, and it is both more definitive and more conditional than the industry was hoping for. The SEC, joined by the CFTC, published interpretive guidance laying out how it approaches the question of what in crypto it will deem a security. The guidance is one of the most specific efforts to define this for the industry in the history of U.S. crypto regulation. [Source: SEC Interpretive Guidance 33-11412 / CoinDesk, March 22, 2026]

SEC/CFTC crypto asset taxonomy from joint interpretive guidance, released March 2026. Source: SEC

The framework establishes several categories. Digital securities are cryptocurrencies that meet the definition of a security under any other context - specifically, those that meet the prongs of the Howey Test. These remain under SEC oversight. Everything else is more nuanced.

Payment stablecoins are generally not securities. Digital tools are generally not securities. Digital collectibles - NFTs, digital art - are generally not securities unless issuers take specific actions like fractionalizing them. Digital commodities, which likely includes bitcoin and possibly ether, are not securities unless they are marketed in ways that meet securities regulations.

"We establish a straightforward taxonomy of crypto assets - most of which are not securities - and clarify how the Supreme Court's Howey test applies when a crypto asset is part of an investment contract." - SEC Chair Paul Atkins and Commissioners Hester Peirce and Mark Uyeda, CoinDesk op-ed, March 19, 2026

The CFTC signed on to the guidance and will administer it under the Commodities Exchange Act. Congressman Troy Downing called it "very positive" while noting that Congress still needs to pass market structure legislation to make it permanent, as the guidance could be undone by a future administration. Law firm partner Chris LaVigne characterized the guidance as "predictably" concluding that most crypto assets are not securities, while noting the SEC retained enforcement discretion: "a crypto asset that is not a security can nonetheless be sold as part of an investment contract if it is marketed with promises of profit derived from the issuer's essential managerial efforts." [Source: CoinDesk, March 22, 2026 - Nikhilesh De]

The legislative timeline is looking tighter than hoped. Senator Cynthia Lummis anticipated a markup in the final weeks of April. Senator Tim Scott said lawmakers are close to agreements on outstanding issues. Senator Kirsten Gillibrand expressed optimism about an upcoming markup. But Jason Gottlieb from Morrison Cohen put the central problem bluntly: "People need to understand that jurisdiction is still uncertain. The SEC is clearly saying 'we don't have jurisdiction if the token does not meet these criteria' - but just because the SEC does not have jurisdiction does not mean the CFTC does." Without a market structure bill, CFTC jurisdiction over non-security cryptocurrencies remains legally uncertain even after this guidance.

The Monday Deadline: What Markets Are Pricing and Why Both Outcomes Are Painful

Markets face a binary binary outcome as Trump's 48-hour Iran ultimatum expires Monday evening. Photo: Pexels

The 48-hour deadline creates a specific market structure problem that is worth mapping clearly before the week opens. There are essentially three scenarios, and none of them have clean bullish resolution in the short term.

Iran complies and reopens the Strait to commercial shipping. Oil collapses from $100+, which reduces mining costs and inflation pressure. Fed rate hike bets ease. Bitcoin likely rallies sharply from the $69K level. This scenario removes the single biggest macro headwind. Probability: low, given Iran's stated position and internal political dynamics.

Iran does not comply and the U.S. strikes civilian energy infrastructure. This is a qualitative escalation with unpredictable second-order effects. Iranian retaliation could range from proxy attacks to direct military engagement. Oil spikes further. Risk assets including crypto sell off hard. Bitcoin likely tests $65K support. Regional conflict risk premium expands globally.

Trump lets the deadline pass without striking, essentially backing down. Markets initially might read this as de-escalation. But it also signals that the ultimatum was a bluff, which reduces deterrence credibility and actually extends the conflict timeline. Medium-term bearish for resolution, despite short-term risk-on reaction. The most likely scenario given diplomatic history.

The options market data from VanEck suggests sophisticated players are hedging for Scenario 2 while positioned for the historical base case that extreme fear precedes rallies. The $685 million in put premium spending over 30 days is not dumb money - it is institutional investors managing tail risk. They are not necessarily predicting bitcoin crashes. They are ensuring that if it does crash, they survive it.

What is clear from the structural data is that the current $69,192 price level is deeply uncomfortable for multiple parties simultaneously. Miners are losing $19,000 per coin. 43% of supply holders are underwater. Miner difficulty is near 2026 lows. Hashprice is near all-time lows. Long liquidations just wiped out eight days of accumulated positioning in twenty-four hours. This is a market under significant stress from multiple directions at once, not just a geopolitical headline risk.

The macro overlay makes it worse. Gold is in a technical bear market despite all the conditions that should be driving it higher. Real rates are rising because oil-driven inflation is pushing out Fed cuts. Risk assets broadly have no clear catalyst for relief until either the Iran situation resolves or the Fed surprises to the dovish side - and after holding rates dovishly last Wednesday, Powell has limited room to move further without inflation data backing.

"Bitcoin's latest fear unlocked as rate hike bets rise and bond markets crumble." - CoinDesk, March 20, 2026

The Ethereum L2 debate, the quantum computing preparations, and the SEC taxonomy announcement are all legitimate long-term positive developments for the crypto space. None of them matter to the Monday morning open. What matters Monday morning is whether Trump gives the order to strike power plants in Iran, whether oil stays above $100, and whether the leveraged longs that got wiped out this weekend attempt to rebuild positions or sit on the sidelines waiting for resolution.

Right now, the most likely scenario is gridlock - a market that cannot fall much further because mining economics force buy pressure through difficulty adjustments, but cannot rally because the macro and geopolitical headwinds remain fully intact. $65,000 to $75,000 is the range until something breaks in either direction. The Monday evening Iran deadline is the most immediate test of which direction that break comes from.

Watch the Strait of Hormuz news wires. Watch oil. Watch whether the difficulty adjustment in early April materializes. And watch whether the VanEck historical pattern - extreme put premium buying as a contrarian buy signal - holds up in a market that is fighting a war it did not have to deal with in any of those prior historical episodes.

Every data point right now is flashing red. The historical pattern says this is where you buy. The macro says this is where you wait. The Monday deadline will tell you which framework was right.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram