Bitcoin Hits $71K: War Rally Meets DeFi Wreckage and the Treasury Trap

BTC rebounds 4% as $550 million in short positions get liquidated. Balancer Labs is shutting down after its third exploit. Resolv's USR stablecoin is trading at 27 cents. And U.S. Treasury yields are quietly becoming the most dangerous variable in the entire equation.

There are at least four separate crises unfolding simultaneously in crypto markets right now. Bitcoin is up 4%. DeFi is bleeding out. Treasury markets are approaching a yield level that historically forces political pivots. And one of the oldest AMMs in the space just announced it's shutting down its corporate entity after a $110 million hack it never recovered from.

The market is focusing on the number: $71,000. That's the headline. The details beneath it are a different story.

The War Trade: Bitcoin's Bizarre Resilience

U.S. and Israeli forces struck Iranian energy infrastructure on Tuesday including a natural gas pipeline in Khorramshahr, according to reports circulating in Asian morning hours. Oil is holding near $100 per barrel. Nasdaq 100 futures are in the red. S&P 500 futures are down about 0.1% since midnight.

Bitcoin climbed anyway.

BTC has gained 4% in the past 24 hours to around $71,053, according to CoinDesk market data. It is outperforming gold - the traditional war hedge - since the conflict began in late February. That tells you something about how the market is pricing Bitcoin in 2026: not as a risk asset, but as a hard asset and a geopolitical hedge.

The proximate trigger for Monday's rally was diplomatic theater. President Trump announced a "48-hour ultimatum pause" over the Strait of Hormuz after claiming "good and productive" talks with Iran. Iranian officials immediately called it "fake news" and denied any communication took place. The conflict escalated again Tuesday with fresh strikes. But the short squeeze was already underway.

AI tokens were a separate catalyst. Nvidia CEO Jensen Huang stated in public remarks that artificial general intelligence has "already been achieved," triggering a rotation into AI-adjacent crypto tokens. Bittensor (TAO) jumped 5.8% and FetchAI (FET) added 4.1% in Asian hours, according to CoinDesk data. The AI narrative didn't die in the war - it's just running parallel.

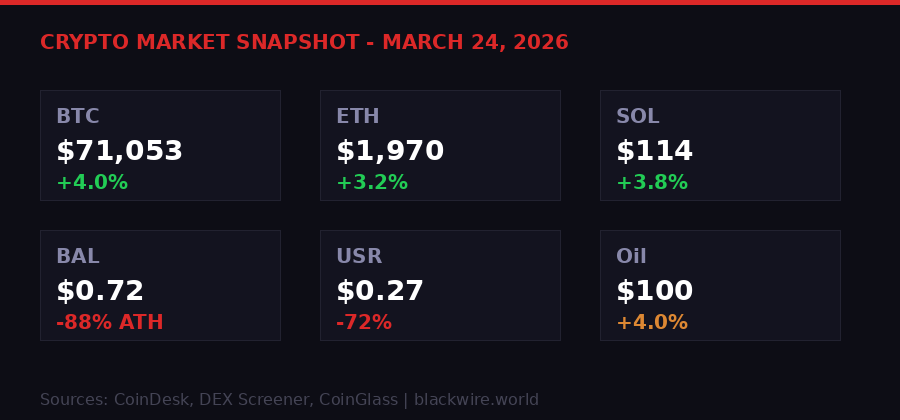

Key Market Data - March 24, 2026

- BTC: $71,053 (+4.0% 24h) - outperforming gold since war began Feb 2026

- ETH: ~$1,970 (+3.2% 24h)

- SOL: ~$114 (+3.8% 24h)

- Oil (WTI): ~$100/barrel - stable near war highs

- Nasdaq 100 futures: -0.1% since midnight UTC

- 10-yr UST yield: 4.37% (+45bps since war start)

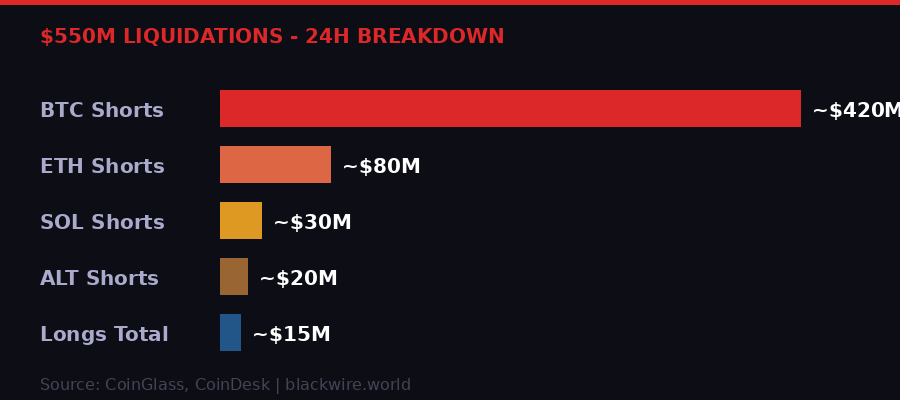

$550 Million Liquidated: What the Derivatives Say

More than $550 million in leveraged crypto futures were liquidated over the past 24 hours, with short positions - bets that prices would fall - taking the majority of the hit, according to CoinDesk and CoinGlass data. That is a significant forced unwind.

But here's the thing traders need to understand: this rally does not have strong legs based on derivatives positioning alone. Open interest in major BTC futures denominated in USD and USDT declined to 228,000 BTC from 229,000 BTC even as price went up 4%. That tells you the move is happening without fresh leveraged longs piling in. Existing shorts got blown out; new longs are not rushing in to replace them at scale.

The same pattern holds across ETH, XRP, and SOL. DOGE, ADA, SUI, AVAX, LINK, and PAXG futures saw open interest fall as much as 10% despite positive price action. Nobody is adding risk at $71K with a war raging and DeFi in pieces.

Perpetual funding rates for majors are between 5% and 10% annualized - positive but not extreme, indicating the market is bullish without being euphoric. On Deribit, BTC and ETH put options still show a net bias for downside protection across all timeframes, but the skew has narrowed from 8-10 volatility points of put premium over calls down to 5-6 points. Risk is receding, but not gone.

The CoinDesk 20 Index (CD20) is up 0.3% on Tuesday while the altcoin-heavy CoinDesk 80 (CD80) has risen more than 1%. Altcoins are outperforming Bitcoin marginally, which historically signals improving sentiment rather than pure flight to BTC safety. HYPE, OP, and CRV are all up around 3% as traders rotate into speculative names in anticipation of a wider breakout.

The memecoin sector is the worst-performing on Tuesday. The CoinDesk Memecoin Index (CDMEME) gained just 0.1% with several index components losing 3-5%. The meme trade is done for this cycle. Real volume is going elsewhere.

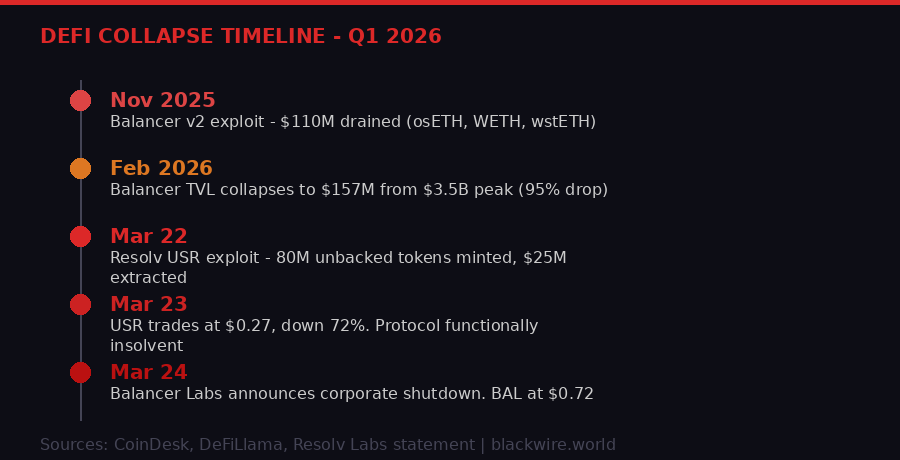

Balancer Labs is Dead: A $110 Million Slow-Motion Collapse

Balancer Labs is shutting down.

The corporate entity that incubated and funded the Balancer decentralized exchange announced Tuesday that it will wind down operations, according to a governance forum post by co-founder Fernando Martinelli. The shutdown is the direct consequence of a November 2025 exploit on Balancer v2 that drained approximately $110 million in digital assets - including osETH, WETH, and wstETH - the third known security breach in the protocol's history.

"BLabs, as a corporate entity, has become a liability rather than an asset to the protocol's future and is just not sustainable as is without any sources of revenue." - Fernando Martinelli, Balancer co-founder, governance forum, March 24, 2026

This is the end of a DeFi founding story. At its 2021 peak, Balancer held nearly $3.5 billion in total value locked, putting it alongside Aave, Uniswap, and Curve as one of the four foundational infrastructure pillars of decentralized trading. It had fees spiking above $6 million annualized. It had institutional backing. It was building the future of finance.

Today, DeFiLlama data shows TVL at $157 million - a 95% collapse from peak. The BAL token is trading at $0.72, down roughly 88% from its all-time high, against a fully diluted valuation of $11 million. The market cap has cratered to $10 million. BAL trades below net asset value.

Martinelli said he "seriously considered" shutting everything down entirely. He didn't - the protocol still generates about $1 million in annualized fees over the past three months, which is enough to sustain a lean operation if you strip out all the deadweight. That is what the restructuring plan proposes to do, aggressively.

The plan: cut BAL emissions to zero, ending what Martinelli calls a "circular bribe economy that costs more than it generates." Wind down the veBAL governance model, which he says was captured by meta-governance protocols like Aura and bribe markets that made voting "unrepresentative of the actual Balancer front line." Redirect 100% of protocol fees to the DAO treasury instead of the current 17.5%. Drop v3 protocol fees to 25% to attract organic liquidity. And run a BAL buyback to give token holders an exit at a fair price.

Martinelli's own relationship with the protocol ends with the wind-down, though he offered advisory capacity. Essential team members would move to a new Balancer OpCo pending a governance vote. The product scope narrows to five areas: reCLAMM pools, liquidity bootstrapping pools, stablecoin/LST pools, weighted pools, and non-EVM chain expansion.

This is not a rescue. This is controlled demolition of the corporate wrapper around a protocol that still breathes but can no longer support the weight of the organization built around it. Whether the protocol survives in leaner form is genuinely uncertain. What's not uncertain is what caused this: three exploits, $110 million in losses, and legal liability that made the company untenable.

The Resolv Disaster: $25 Million Gone, USR at 27 Cents

While Balancer was dying slowly over months, Resolv blew up in minutes.

On Sunday March 22 at 2:21 a.m. UTC, an attacker exploited a flaw in Resolv's USR stablecoin minting contract. The attack was simple in its elegance and catastrophic in its effect: the attacker deposited 100,000 USDC and received 50 million USR tokens in return - roughly 500 times the expected amount - because the minting contract contained no oracle checks, no amount validation, and no maximum mint limits.

Two transactions. 80 million unbacked tokens created. USR crashed to $0.025 on its most liquid Curve Finance pool within 17 minutes of the first mint. The attacker converted the proceeds to ETH through decentralized exchanges and now holds 11,409 ETH worth approximately $23.7 million plus $1.1 million in wrapped USR in a separate wallet, according to CoinDesk and blockchain security analysis.

"This is a growing trend of attacks that are focusing on the blind spot of security teams - sensitive keys and credentials that do not hold the funds directly, but can be used to access the funds. That includes dev credentials, trading API keys, and other deployment keys." - Ido Sofer, founder, Sodot (crypto key management firm), via CoinDesk

Resolv's initial statement described the incident as a "compromised private key" and "targeted infrastructure compromise." Onchain analysts found the real problem was structural: the SERVICE_ROLE account that completes swap requests in the minting contract was controlled by a single externally owned account, not a multisig. It was a single point of failure with administrative power over an active financial system holding hundreds of millions in TVL.

USR was supposed to be a dollar-pegged stablecoin using a delta-neutral hedging strategy backed by ETH and BTC. As of Monday morning it was trading at $0.27, down 72% on the week. The protocol holds $95 million in assets against $173 million in liabilities. It is functionally insolvent. There is no mathematical path to peg restoration at those numbers without external capital injection.

Resolv's TVL had peaked near $684 million in February 2025 and declined through the year to around $95 million before the exploit. The protocol advised users strongly against trading USR while recovery measures are being implemented, warning that user actions during the post-exploit period "may affect the recovery." That is code for: we don't have a plan yet, and panicking will make it worse.

The back-to-back failures of Balancer and Resolv within 24 hours is not coincidence - it is a structural DeFi problem. Market observers are calling this a "really dark" period for the sector. The yield opportunities that made DeFi compelling in 2021-2022 have compressed. The risk of catastrophic loss - through exploit, governance capture, or operational failure - remains constant. The risk/reward has inverted. Capital is leaving and not coming back at scale until the security infrastructure fundamentally improves.

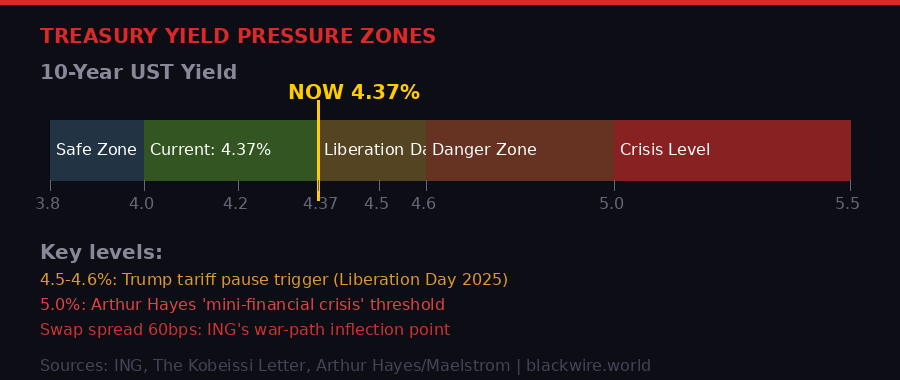

The Treasury Trap: How Bond Markets Could End the War

The most underappreciated story in crypto markets right now has nothing to do with DeFi exploits or short squeezes. It's the 10-year U.S. Treasury yield, sitting at 4.37% and climbing.

Since the Iran war began at the end of February, the benchmark yield has surged roughly 45 basis points. That move is pricing in delayed Federal Reserve rate cuts and higher inflation expectations from elevated oil. But the real mechanism is more dangerous: as yields rise, they increase the cost of funding U.S. government debt, which eventually creates enough economic pressure to force political decisions.

ING's Padhraic Garvey, regional head of research Americas, has identified the key threshold in a note to clients: the 10-year U.S. Treasury swap spread. It currently sits just below 50 basis points.

"Watch the 10-year swap spread. It's just below 50bp now. If that were to shoot to 60bp, it would spell enough trouble to ultimately shape the war path. Why? It's a measure of the de-rating of Treasuries. We need to steer clear of that. It's not just the negative perception, it's the added cost of funding U.S. debt." - Padhraic Garvey, CFA, Regional Head of Research Americas, ING

Rising swap spreads aren't just perception - they increase the implied cost of U.S. government borrowing, which ripples through the financial system and tightens credit conditions across the board. The mechanism is real and measurable.

The more commonly cited threshold comes from The Kobeissi Letter: the 4.5-4.6% range on the 10-year yield. That is exactly where Trump pulled back from his Liberation Day tariffs in April 2025. When the 10-year surged past 4.50%, Trump began floating a tariff pause. When it broke above 4.60%, he officially implemented a 90-day pause on reciprocal tariffs on April 9th, 2025. The bond market forced his hand then. The same mechanism is in play now.

We are currently at 4.37%. We are 13 basis points from the zone that previously caused a geopolitical 180. If the U.S. and Israeli strikes on Iranian energy infrastructure intensify, if oil pushes further above $100, if inflation expectations reprice hard - that threshold is reachable within days.

Beyond 4.5-4.6% sits Arthur Hayes' scenario. The BitMEX co-founder and Maelstrom Fund CIO has previously argued that a 10-year yield above 5% could trigger a "mini-financial crisis" that forces the Fed to step in with liquidity injections. The U.S. economy, in Hayes' analysis, simply cannot sustain 5% on the 10-year given current debt levels and the cost structure of refinancing trillions in maturing Treasuries.

What does this mean for Bitcoin? The initial reaction to a yield spike toward 5% would likely be a sharp selloff - risk assets don't like financial crises. But if the Fed is then forced to inject liquidity, Bitcoin would likely recover quickly and potentially overshoot. The pattern is familiar: the same dynamic played out in March 2020, in the COVID-era QE cycles, and in every major liquidity injection event since 2019. Liquidity injections are rocket fuel for BTC.

Traders are being told by multiple analysts to watch Treasury yields and swap spreads as closely as they watch Bitcoin price action. For once, that advice is accurate.

Bitcoin Mining Concentration: The 2-Block Reorg Nobody Is Talking About

While markets were focused on the war rally and DeFi explosions, something unusual happened at Bitcoin block height 941,881: a 2-block chain reorganization, the clearest on-chain signal yet that hashrate is concentrating into fewer and fewer hands.

Here's what happened, according to CoinDesk's technical analysis: at 15:49:35 UTC on Monday, AntPool found a valid block at height 941,881. Twelve seconds later, at 15:49:47 UTC, Foundry found a different valid block at the same height. The network briefly split, with some nodes following AntPool's chain and others following Foundry's.

ViaBTC extended AntPool's chain at block 941,882. Foundry extended its own. Two competing chains, each two blocks deep, running in parallel. Then Foundry produced blocks 941,883 through 941,886 consecutively, making its chain the heaviest by a significant margin. The network reorganized to Foundry's version. AntPool and ViaBTC's blocks were orphaned - valid work, zero reward.

A 2-block reorg does not threaten Bitcoin's security. The network resolved it exactly as designed. But the event is a structural warning about what happens when hashrate concentrates.

Foundry USA currently controls approximately 30% of Bitcoin's total hashrate - enough that when conditions align, it can mine multiple consecutive blocks and trigger exactly this kind of reorg when it finds a block at nearly the same time as a competitor. The smaller the number of large pools, the more frequently this will happen.

Bitcoin's mining difficulty dropped 7.76% on Saturday, the second-largest negative adjustment of 2026. Total network hashrate has retreated to roughly 920 EH/s from the 1 zetahash record hit in 2025. The reason: with Bitcoin at $70,000, mining is deeply unprofitable. The average production cost is estimated at around $88,000 per BTC. Smaller and mid-size miners are shutting down, and their hashrate is concentrating into the large pools that can absorb the losses temporarily through scale and capital reserves.

Every miner that exits the network makes Foundry's relative share larger. This is a feedback loop that doesn't reverse until Bitcoin price rises significantly above production cost or larger miners themselves start failing. Neither scenario is imminent.

Revolut, Tokenization, and the Institutional Accelerator

Not everything in Tuesday's markets is a disaster. The divergence between institutional crypto infrastructure and retail DeFi has never been more visible.

Revolut, the crypto-friendly European fintech, reported that 2025 profits soared 57% to $2.3 billion, according to CoinDesk. Its customer base grew to 68.3 million users. Total customer balances jumped 66% to $67.5 billion. Transaction volume hit $1.7 trillion. Revolut built this on the back of a business model that integrates crypto trading as a native feature alongside traditional banking - and it is printing money.

Meanwhile, Apex Group - a major fund services provider - announced plans to tokenize the Omnes Mining Note (OMN) on Coinbase's Base blockchain. The structured note is backed by Bitcoin hashrate and targeting institutional investors who want exposure to Bitcoin mining without the operational complexity. This is the Apex telling institutional clients: you can own a piece of the mining industry like owning a bond.

And Strategy (the company formerly known as MicroStrategy) topped up its capital-raising plans, bringing its potential Bitcoin buying power back to $42 billion through expanded share issuance and new Wall Street partnerships, according to CoinDesk. Michael Saylor's playbook continues: treat Bitcoin as balance sheet, use equity markets to fund accumulation, and leverage the difference.

BlackRock CEO Larry Fink's annual shareholder letter, released Monday, argued that "digital wallets and tokenized assets could modernize markets and expand investor access" in the same way the internet transformed mail. Fink is betting billions on tokenized funds. BlackRock is not experimenting. It is building at scale.

The pattern is clear: the players with balance sheets, compliance departments, and legal infrastructure are accelerating into crypto. The players without it - the DeFi protocols running on optimistic trust in smart contract security - are collapsing. This is not a coincidence. This is the market sorting.

What Comes Next: The $75K Line and the War Variable

The headline question in markets right now is whether Bitcoin can get to $75,000. That's the number analysts and derivatives markets are treating as the "full bull" confirmation threshold - the level that would indicate the war-related uncertainty discount has been priced out and the underlying bid is structural.

Getting there requires at least one of three things to happen.

First: the Iran conflict de-escalates in a real and verifiable way, not through diplomatic statements that Iran immediately contradicts. A genuine ceasefire or pause would send oil back below $90 and allow equity markets to recover, reducing the macro headwind that keeps marginal crypto buyers on the sidelines.

Second: Treasury yields stabilize below 4.5%. If the 10-year backs away from the Liberation Day threshold rather than breaking through it, the bond-market pressure on the war calculus eases. This would remove the tail risk of a forced Fed liquidity injection scenario - which would be crypto-positive but only after a violent initial shock.

Third: fresh capital formation. The $550 million short liquidation proved there are motivated sellers of volatility in this market. But declining open interest during the rally means buyers are not yet committing new money at scale. For Bitcoin to push from $71K to $75K in a sustained way, new capital needs to enter - not just forced exits from the short side.

The DeFi collapse is a separate track from Bitcoin's price trajectory but it matters for the broader crypto narrative. Every blown-up stablecoin and every shut-down DeFi lab erodes the "DeFi will replace TradFi" argument that drew capital into the ecosystem. That capital does not necessarily leave crypto - it goes to Bitcoin, to institutional products, to tokenized assets. The ecosystem is concentrating, not contracting.

The mining concentration story is a slow-burn. A 2-block reorg is not an emergency. But if Bitcoin stays below production cost for another quarter, the concentration will deepen. And deeper concentration means less network resilience and more political surface area for arguments about mining cartels. This is a year-horizon risk, not a week-horizon risk.

Short-term, the war controls everything. Trump's relationship with Treasury yields is the clearest predictor of geopolitical posture available in public markets. Watch 4.5% on the 10-year. If it breaks there and holds, expect a significant diplomatic event within days. That diplomatic event will likely be crypto-positive. If the yield blows past 4.5% toward 5%, expect the kind of financial market stress that precedes forced Fed action. That's initially crypto-negative, then massively crypto-positive.

Either way, short sellers at $71,000 are not having a good Tuesday.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on TelegramSources: CoinDesk market data (March 24, 2026); Balancer Labs governance forum post by Fernando Martinelli; Resolv Labs official incident statement; ING research note by Padhraic Garvey CFA; The Kobeissi Letter market analysis; Arthur Hayes/Maelstrom Fund published commentary; CoinDesk blockchain technical analysis; DeFiLlama TVL data; CoinGlass liquidation data; Revolut 2025 annual financial results; BlackRock CEO Larry Fink 2026 shareholder letter.