The Easter Trap: Bitcoin Enters Its Most Dangerous Weekend as ETFs Go Dark, Whales Dump, and War Grinds On

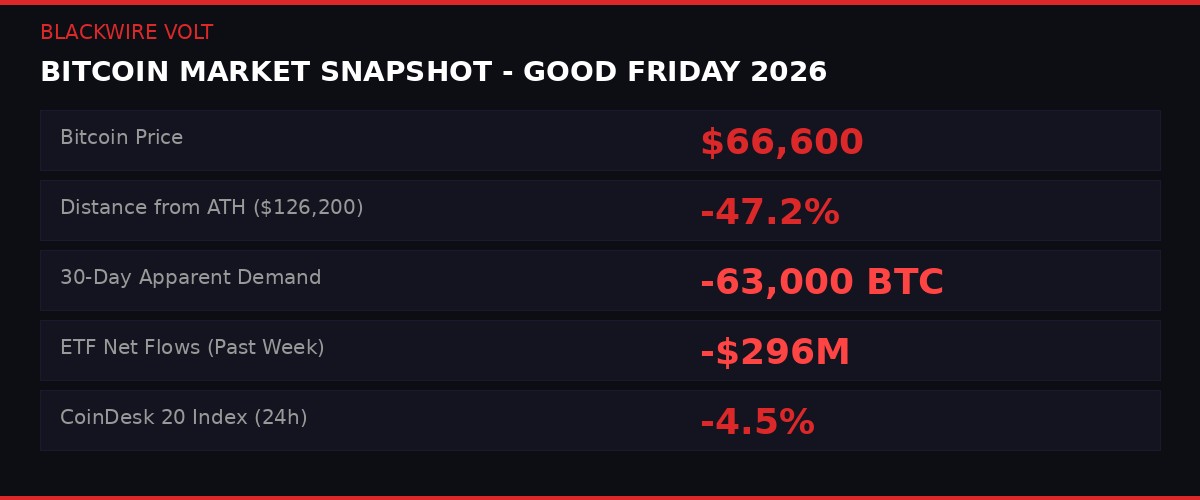

Bitcoin is sitting at $66,600 on Good Friday morning. In the next 72 hours, every institutional buyer that has propped up this market will be offline. CME futures - closed. ETF creation and redemption - paused. The machines that arbitrage spot and futures? Quiet. What remains is a spot market drowning in sell pressure, a negative gamma zone that turns every small dip into an avalanche, and a geopolitical backdrop that could send oil past $115 with a single missile strike. This is not a holiday. This is a trap.

The Liquidity Void: What Happens When the Machines Go to Church

Good Friday is not just a day off. It is the annual shutdown of every institutional mechanism that has come to underpin bitcoin's price in 2026. The Chicago Mercantile Exchange (CME), where bitcoin futures now account for a dominant share of institutional positioning, closes entirely for the holiday. It does not reopen until Sunday evening. Every spot bitcoin ETF listed in the United States - from BlackRock's iShares Bitcoin Trust (IBIT) to Fidelity's Wise Origin Bitcoin Fund (FBTC) and the dozen other products that collectively manage over $60 billion in assets - halts creation and redemption activity. CoinDesk

This matters more than it used to. As CoinDesk reported in February, bitcoin's price discovery has been steadily migrating from unregulated spot exchanges to CME futures and the ETF wrapper. The arbitrage between spot and futures, executed by sophisticated market makers, keeps prices aligned across venues. When CME goes dark, that arbitrage breaks. When ETFs cannot create or redeem shares, the passive bid from pension funds and wealth managers disappears. CoinDesk

What remains is the raw spot market. And right now, that spot market is bleeding.

CryptoQuant data shows 30-day apparent demand at approximately -63,000 BTC. That number deserves a moment of attention. It means that despite ETF purchases climbing to roughly 50,000 BTC over the past 30 days - the highest level since October 2025 - and despite Strategy (formerly MicroStrategy) accumulating about 44,000 BTC over the same period, the selling from other market participants has overwhelmed those inflows by a substantial margin. CryptoQuant via CoinDesk

The net demand number is negative. And the institutional buyers that partially offset the selling are about to go dark for three days.

Singapore-based market maker Enflux captured the situation in a client note: the price floor is "partly underwritten by rate-cut expectations," expectations that are themselves under attack from inflation data. The ISM prices-paid index jumped to 78.3 in March, its highest reading since June 2022. Enflux reported $296 million in net ETF outflows during the week of March 24, with only muted inflows in early April. Enflux via CoinDesk

Strip away the institutional bid. Strip away the arbitrage. Strip away the rate-cut narrative. What you have left is a market held together by hope and habit, entering a weekend where neither will be enough if anything goes wrong.

The Whale Exodus: 188,000 BTC and Counting

The most alarming datapoint in bitcoin's current market structure is not the price. It is the behavior of the largest holders.

According to CryptoQuant's latest report, wallets holding between 1,000 and 10,000 BTC - the whale tier, the entities whose accumulation historically marks the floor of bear markets and whose distribution historically marks the top - have flipped to net distribution. Their one-year balance change has dropped to approximately negative 188,000 BTC, a dramatic reversal from a positive 200,000 BTC near the 2024 cycle peak. CryptoQuant via CoinDesk

To put that in dollar terms: at current prices, 188,000 BTC is roughly $12.5 billion worth of bitcoin that the market's largest individual holders have been selling over the past year. This is not retail panic. This is not leveraged traders getting liquidated. This is the smart money, the long-term accumulators, the wallets that have survived multiple cycles, deciding that the current environment warrants reducing exposure.

Mid-sized holders have also sharply slowed accumulation. The Coinbase Premium - the difference between bitcoin's price on Coinbase Pro (the primary U.S. institutional venue) and global exchanges - has remained persistently negative, signaling weak domestic spot demand from American traders and institutions. CryptoQuant

This is the paradox of the current market. ETF purchases are at multi-month highs. Strategy keeps buying. But the broader holder base is dumping into that bid. The institutions are absorbing some of the selling. But not all of it. And the gap between institutional buying and aggregate selling is widening.

The CryptoQuant report noted that any relief rally would face resistance between roughly $71,500 and $81,200 - levels that have capped every prior rebound during this bear market structure. For bulls, the math is brutal: you need to climb 7% to hit the first resistance wall, and 22% to break out of bear territory entirely. For bears, you just need to wait for the institutions to take a long weekend.

The Negative Gamma Time Bomb

Below the surface of spot prices, the derivatives market has built something ugly.

In recent weeks, traders on Deribit - the dominant crypto options exchange - have been loading up on put options providing downside protection. These defensive positions are concentrated at strike levels from $68,000 all the way down to the mid-$50,000s. Given the Iran war, quantum computing threats, and a six-month bear market, the demand for insurance makes intuitive sense. But insurance creates its own risk. Glassnode via CoinDesk

When traders buy puts, the dealers (market makers) who sell those puts take on "negative gamma" exposure. This is a technical concept with very practical consequences. Negative gamma means that as bitcoin's price falls, the dealers' losses on their short put positions increase. To hedge those mounting losses, they must sell bitcoin. Their selling pushes the price down further. Which increases their losses on the puts. Which forces more selling. Which pushes the price down further.

This is not theoretical. It is mechanical. The feedback loop is baked into the math of options hedging.

Glassnode's analysis shows that dealer gamma exposure is predominantly negative from $68,000 all the way down to $50,000. Bitcoin has already broken below $68,000 as of this writing, putting it squarely inside the danger zone. Glassnode

"Negative gamma is now building just below current price levels, from $68K all the way down to the high 50s. A move into this zone could trigger accelerated selling as hedging flows reinforce downside momentum, turning what would otherwise be a gradual move into a sharper repricing, with a potential revisit of the $60K level."

- Glassnode Weekly Report, April 2, 2026

The $60,000 level is significant. It was the bottom of the February 5 selloff, the sharpest single-day decline of this cycle. If the negative gamma feedback loop fully engages, it could carry bitcoin below that level in a matter of hours - not days.

And here is the timing problem: the March 27 options expiry already drained liquidity from the derivatives market. The Easter weekend will drain what is left. When the selling feedback loop needs buyers to absorb the pressure, there may simply be nobody there. The market makers who normally provide two-sided liquidity will be hedging, not absorbing. The institutional arbitrageurs will be offline. The ETF create/redeem process will be frozen.

The timing could not be worse. If any geopolitical headline drops over the weekend - an escalation in the Strait of Hormuz, a breakdown in ceasefire talks, a new oil supply disruption - the price reaction will happen in a market with no institutional stabilizers, inside a derivatives structure designed to amplify downward moves.

The War That Will Not Let Go

The Iran war, now in its 34th day, has rewritten the macro environment for every risk asset on the planet. Before the conflict escalated, the setup for crypto was improving. Global growth was strengthening. Central banks were leaning toward rate cuts. Stablecoin supply had crossed $315 billion. Institutional adoption was accelerating. Grayscale

Then the missiles started flying, and everything changed.

Grayscale, the largest digital asset manager, published a report on April 2 that captured the current state of play with unusual directness: "The war in Iran overshadowed virtually all other market developments in March." Oil prices have surged, fueling inflation concerns that have pushed interest rate expectations higher. The Fed, which was expected to begin cutting rates in Q2, is now on hold. The rate-cut narrative that underpinned much of bitcoin's institutional bid has evaporated. Grayscale Research Report

President Trump's "renewed aggressive posturing toward Iran" pushed bitcoin down roughly 2% just yesterday, according to CoinDesk. But the broader damage goes beyond single-day moves. Since the outbreak of the conflict, bitcoin has been broadly rangebound in the mid-$60,000s to low-$70,000s, with sharp headline-driven swings tied to oil prices and shifting risk sentiment. Each escalation drives a leg down. Each hint of cooperation drives a partial recovery. But the highs keep getting lower. CoinDesk

The dual chokepoint crisis at the Strait of Hormuz and Bab el-Mandeb has kept oil elevated above $100 per barrel for weeks. Iran's 34-day internet blackout - the longest wartime shutdown in modern history, as BLACKWIRE reported earlier this week - signals a regime that is digging in, not negotiating. Wednesday brought a brief reprieve when Iran signaled cooperation on a key shipping route, sending oil down $6 per barrel intraday and giving bitcoin a bounce. But the relief was temporary. The structural risk remains.

For crypto investors, the war creates a paradox. Bitcoin was supposed to be a hedge against geopolitical chaos. Instead, it trades like a risk asset - correlated with equities, inversely correlated with oil, and punished by every headline that suggests inflation will stay elevated. Grayscale noted that bitcoin has actually held up "better than some traditional markets" and has been "roughly flat since the start of the war," outperforming equities at times. But "flat" is not what anyone bought bitcoin for. Grayscale

The asset manager expects investors to remain on the sidelines until there is "greater clarity" on the conflict. If the war eases and energy prices retreat, a rapid repricing toward a more supportive environment is possible. If it grinds on, "persistently high oil prices may continue to pressure growth and delay a broader recovery." Grayscale

There is no clarity coming this weekend. Only a holiday and a hot war.

The Bear Market Clock: Time Pain vs. Price Pain

Bitcoin's price has fallen approximately 47% from its October all-time high of $126,200. That drawdown is painful but not unprecedented. In fact, it may be historic for a different reason: its relative mildness.

Fidelity Digital Assets analyst Zack Wainwright observed this week that bitcoin's crashes are getting smaller with each cycle. After the 2013 peak of $1,163, bitcoin fell 87% to $152. After the 2017 peak of $20,000, it fell 84% to $3,122. This cycle, the maximum drawdown has been roughly 50%. "Each cycle has been less dramatic to the upside than the previous and downside risk has also been less dramatic," Wainwright wrote in an April 1 post. Fidelity Digital Assets via CoinDesk

AdLunam co-founder Jason Fernandes explained the structural shift: "As liquidity deepens and institutional participation increases, volatility naturally compresses on both the upside and the downside." The capital required to drive a 90% collapse is simply too great in a market with ETF wrappers, pension exposure, and corporate treasuries. CoinDesk

Not everyone agrees. Bloomberg Intelligence's Mike McGlone continues to insist that bitcoin could see a "normal reversion" toward $10,000, arguing that "the crypto bubble is over." He envisions a scenario where a broader decline across equities, commodities, and risk assets drags bitcoin into a much deeper hole. Bloomberg Intelligence via CoinDesk

But even the optimistic read comes with a warning. The bear market may not go much deeper in price terms, but it could go much longer in time.

Glassnode's Realized Cap HODL Waves - a metric that groups bitcoin supply by holding period and weights by realized price - shows a familiar pattern forming. Historically, bear market bottoms coincide with long-term holders (those holding six months or more) controlling at least 85% of supply. Currently, long-term holders account for about 80%. The trend is moving in the right direction, but several months of consolidation likely remain. Glassnode via CoinDesk

This is what traders call "time pain" - the slow, rangebound grind that exhausts both bulls and bears through sheer boredom and frustration. Price pain forces capitulation quickly. Time pain does it slowly. Both are effective. Time pain may be worse because it drains conviction without providing the cathartic flush that typically marks a bottom.

The implication for the Easter weekend is straightforward. Even if bitcoin survives the next 72 hours without a dramatic crash, the path ahead offers months of grinding, directionless trading. The bear market is maturing. That does not mean it is ending.

The Regulatory Earthquake Nobody Is Pricing In

While markets fixate on oil prices and options greeks, a seismic shift in crypto regulation happened late Thursday that has not yet been fully absorbed.

President Trump fired Attorney General Pam Bondi and elevated Todd Blanche - his former personal criminal defense attorney and the sitting Deputy Attorney General - to the position of interim Attorney General. Blanche is not a neutral figure in crypto. He is the author of the DOJ memo that disbanded the National Cryptocurrency Enforcement Team (NCET), the unit created in 2022 to pursue crypto-specific criminal cases. He signed a four-page order directing prosecutors not to pursue regulatory violation cases in the crypto industry. CoinDesk

According to ProPublica, Blanche held between $159,000 and $485,000 in crypto assets - including Bitcoin, Solana, Cardano, Ethereum, Polygon, Polkadot, and Quant - when he signed that memo. He also held Coinbase stock. His ethics disclosure shows he transferred the holdings to his children and a grandchild, but ProPublica reported the transfers happened after the memo was signed, violating ethics rules and his own pledge to divest before working on crypto-related matters. ProPublica via CoinDesk

Now this person runs the entire Department of Justice.

The implications are layered. On one hand, the man who effectively decriminalized crypto regulatory violations is now the nation's top law enforcement officer. For exchanges, DeFi protocols, and token projects that feared SEC or DOJ action, this is the most favorable enforcement environment imaginable. On the other hand, this comes days after Drift Protocol lost $285 million to an exploit that blockchain analytics firm Elliptic linked to North Korean state-sponsored hackers. Elliptic

The tension is obvious. The same government that is pulling back from crypto enforcement is watching a hostile nation-state steal hundreds of millions of dollars from American crypto protocols and users. The NCET was built precisely for this type of investigation. It no longer exists.

Simultaneously, the CFTC - now led by Chairman Mike Selig - filed an extraordinary lawsuit against three states: Illinois, Arizona, and Connecticut. The states had sent cease-and-desist letters to prediction market providers, arguing the companies were offering unregulated sports gambling. The CFTC countered that prediction markets are federally regulated swaps under the Commodity Exchange Act, giving the federal agency "exclusive jurisdiction." CFTC via CoinDesk

Illinois Governor J.B. Pritzker's office fired back with unusual venom: "The Trump Administration is carrying water for companies driving well-documented and lucrative insider trading schemes." The battle line is drawn. The federal government is deregulating crypto at the same pace that state governments are trying to clamp down. CoinDesk

For the market, the regulatory chaos adds another layer of uncertainty. Is the DOJ going to prosecute the next Drift-style hack aggressively? Or has the enforcement apparatus been intentionally hollowed out by someone who was literally invested in the industry he was supposed to regulate? The answer to that question matters for billions of dollars in capital allocation. The market is not pricing it in yet.

The X Factor: Musk's Kill Switch and the Scam Economy

In a development that could reshape crypto's marketing infrastructure, Elon Musk's X (formerly Twitter) announced it will auto-lock any account that mentions cryptocurrency for the first time in its history. The feature, revealed by X Head of Product Nikita Bier on April 2, targets the epidemic of hijacked accounts being used to promote scam tokens and phishing operations. CoinDesk

Bier called it a "scam kill switch" and said it "should kill 99% of the incentive" behind the current wave of phishing that tricks users into surrendering credentials through fake copyright violation emails, then uses their accounts to push fraudulent crypto projects. The change was prompted by a detailed firsthand account from an X user who lost control of their account after falling for a pixel-perfect fake login page that harvested two-factor authentication codes.

The implications for crypto marketing are significant. X has been the primary social distribution channel for crypto projects since the earliest days of Bitcoin Twitter. Token launches, airdrop announcements, community building, influencer marketing - all of it runs through X. A system that auto-locks any first-time crypto mention would catch not just scammers but also legitimate projects, new users discussing crypto for the first time, and any account that has previously focused on non-crypto topics.

Bier's language suggested the system will involve an additional verification step rather than a permanent lock, but the friction alone could measurably reduce the volume of crypto-related content on the platform. For an industry that relies heavily on social virality and network effects, that is not nothing.

The scam economy that X is targeting is enormous. The most infamous precedent was the 2020 Twitter hack that compromised accounts belonging to Apple, Barack Obama, and Musk himself, netting over $100,000 in bitcoin from a fake giveaway. That breach, carried out through social engineering against Twitter employees, resulted in a 5-year prison sentence. Current scam operations are more sophisticated, more distributed, and harder to trace. They run on hijacked accounts, fake airdrops, and pump-and-dump token launches that generate millions before disappearing. CoinDesk

Bier also called out Google for failing to stop phishing emails at the email level, pointing out that much of the account hijacking starts with phishing messages that Google's filters should catch but do not. The blame is distributed across platforms, but X is the one taking action.

The Stablecoin Lifeline: $315 Billion and Growing

Amid the bearish indicators, one structural metric keeps flashing green: stablecoin supply.

The total stablecoin market has expanded from approximately $20 billion in 2020 to more than $315 billion today, according to DeFiLlama data. The sector added roughly $100 billion in 2025 alone, reflecting a surge in demand for dollar-pegged digital assets across trading, payments, and onchain finance. Even through the current bear market, stablecoin supply has continued to grow - a notable divergence from 2022, when the collapse of TerraUSD triggered a contraction. DeFiLlama via Grayscale

SoFi announced on April 2 that it is launching SoFi Big Business Banking, a platform that lets companies manage U.S. dollars and crypto - including stablecoins - within its regulated bank. The service aims to replace the current patchwork of banks, stablecoin issuers, and custodians by enabling 24/7 deposits, conversion into SoFiUSD (the bank's own stablecoin), and instant movement of funds. CoinDesk

Meanwhile, Coinbase received conditional approval from the Office of the Comptroller of the Currency (OCC) for a trust charter, moving it closer to operating as a federally regulated crypto custodian. The x402 protocol - Coinbase's AI payments system that enables machines to pay each other using stablecoins - joined the Linux Foundation with support from Google, Stripe, AWS, Visa, and Cloudflare. CoinDesk

The crypto market structure bill, which would provide comprehensive regulatory clarity for digital assets, has been pushed back but is still in active development. Industry representatives are reviewing revised stablecoin yield compromise language this week. CoinDesk

Europe added its own milestone. France's new blockchain-native stock exchange announced it is taking an aerospace firm public directly onchain - the first blockchain IPO in European history. The move positions Lise and ST Group as an early test case for going public on blockchain rails within EU regulations. CoinDesk

These are real structural developments. Stablecoins growing to $315 billion is not speculative froth. SoFi integrating crypto into FDIC-insured banking is not a meme. Coinbase getting a federal charter is not a press release. The infrastructure is being built even as the price bleeds.

Grayscale's report captured the duality: "The long-term drivers of the asset class, including growing adoption of stablecoins and tokenized assets, remain intact." Periods of heightened uncertainty "have historically presented attractive opportunities for long-term investors positioning for the next phase of growth."

The question is whether any of that matters over a holiday weekend where the institutional buyers are offline, the whales are selling, and the options market is rigged to amplify every downtick.

The Cycle That Refuses to Break

There is a case for optimism buried under the rubble, and it is worth examining honestly.

Bitcoin's drawdown compression is real. From 87% in 2014 to 84% in 2018 to roughly 50% now - the pattern suggests an asset that is genuinely maturing. Fidelity's research showed that in a 10-year comparison across major asset classes, bitcoin delivered roughly 20,000% returns while leading on risk-adjusted measures despite its volatility. It has been the top-performing asset in 11 out of the past 15 years. Fidelity Digital Assets

Jason Fernandes of AdLunam articulated the bull case for allocation: "If a small 1% to 3% allocation can materially improve returns and Sharpe ratios without significantly increasing drawdowns, then bitcoin starts to function less like a standalone bet and more like an efficiency enhancer within a diversified portfolio." His punchline: "The risk isn't about owning bitcoin anymore. It's the opportunity cost of having no exposure at all." CoinDesk

That framing is powerful for the medium term. It is irrelevant for this weekend.

The structural case for bitcoin has never been stronger. ETFs, federal charters, corporate treasuries, stablecoin rails, sovereign experiments in tokenization. The adoption curve is unmistakable. But markets do not trade on five-year roadmaps. They trade on liquidity, positioning, and fear. Right now, all three point the same direction.

WHAT TO WATCH THIS WEEKEND

- Bitcoin spot price relative to $65,000 support CRITICAL LEVEL

- Any Iran/Hormuz/Houthi headline escalation HIGH RISK

- Deribit put option activity and gamma shifts NEGATIVE GAMMA ZONE

- Stablecoin flows to exchanges (selling signal) MONITOR

- CME futures gap at Sunday night reopen GAP RISK

- April 9 core PCE inflation data (forward risk) KEY CATALYST

The best-case scenario for bulls is that nothing happens. A quiet Easter, no headlines, no escalation, no new hacks. Bitcoin drifts sideways, CME reopens Sunday night without a major gap, and the market limps into next week where the real test - April 9 core PCE inflation data - awaits.

The worst-case scenario is that something does happen. An escalation in Iran. A new exploit. A whale wallet dumping into a thin market. The negative gamma feedback loop engages, prices cascade below $65,000, no institutional buyer is available to absorb, and by the time CME reopens on Sunday night, bitcoin is trading at $58,000 with a gap that needs to be filled in both directions.

Between those scenarios sits every possible shade of volatility, in a market that has been systematically stripped of the tools and participants that would normally dampen it.

Bitcoin has survived worse. It always does. But it has rarely entered a holiday weekend with this specific combination of structural vulnerability: whale distribution, institutional shutdown, negative gamma exposure, hot war backdrop, inflation resurgence, regulatory chaos, and a six-month bear trend that shows no signs of reversal.

Happy Easter. Watch the charts.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram