Bitcoin's Fear Trade: Record Put Premiums, Rate Hike Ghosts, and Strategy's 761,068 BTC Counterbet

Bitcoin traders are paying more to insure against losses than at any point in recorded history. Rate hike probability for April jumped from 0% to 12% in a single week. Gold and silver are collapsing. And Strategy just logged its second-biggest quarterly BTC haul ever - 89,618 BTC - at these very prices. The divergence is the story.

Bitcoin markets are pricing a level of fear not seen since China's 2021 mining ban. (Pexels)

The Put Premium Signal: Wall of Worry or Real Fear?

Bitcoin options markets are screaming louder than any point in recent history. (Pexels)

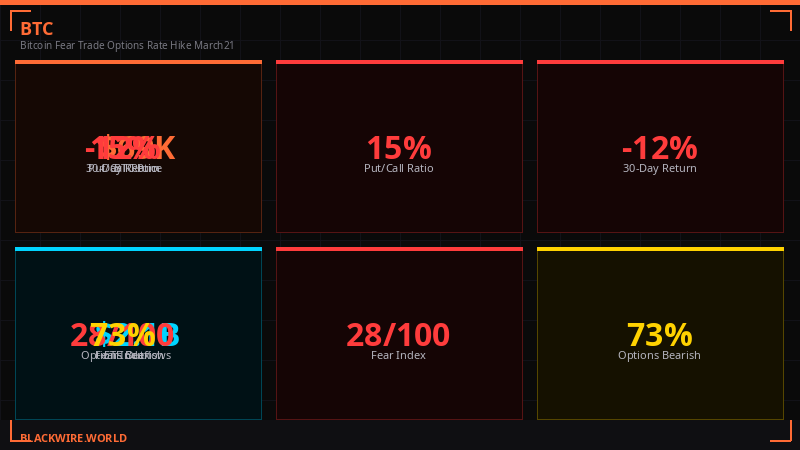

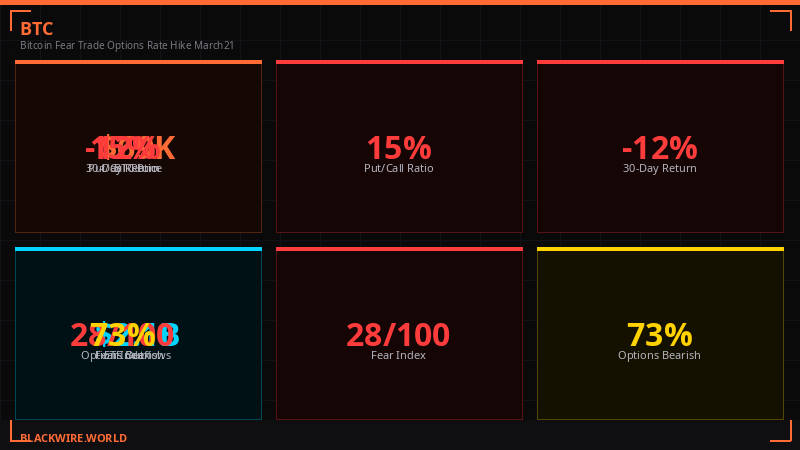

The VanEck mid-March 2026 Bitcoin ChainCheck landed Friday with one stark conclusion: investors are as defensive as they have ever been. The put/call open interest ratio averaged 0.77 and peaked at 0.84 - the highest since June 2021, when Beijing's crackdown on miners sent the entire crypto industry into a multi-month tailspin. (Source: VanEck Bitcoin ChainCheck, March 2026)

In raw dollar terms: traders spent approximately $685 million on put options over the past 30 days. Call premiums fell 12% to roughly $562 million over the same period. That $123 million gap in favor of puts - expressed as a ratio of spot volume - hit 4 basis points. An all-time high in VanEck's data. (Source: VanEck)

"Relative to spot volume, put premiums reached an all-time high of roughly 4 basis points, roughly 3x the levels seen in mid-2022 following the Terra/Luna stablecoin collapse and the Ethereum staking liquidity crisis." - VanEck Bitcoin ChainCheck, March 2026

For context: the Terra/Luna wipeout in May 2022 erased roughly $40 billion in value in 72 hours. The Ethereum merge-staking crisis that followed locked billions in illiquid positions. Those were two of the most catastrophic 90-day windows in crypto history. The current put premium reading is 3x those levels.

Put premiums hit $685M vs call premiums of $562M. The gap vs spot volume is an all-time record. (BLACKWIRE/VanEck data)

Realized volatility has actually cooled - dropping from around 80 to just above 50 since the Iran war began. Futures funding rates eased to 2.7% from 4.1%, meaning levered longs are scaling back. On-chain activity remains weak. Miner selling is contained. The picture is not one of panic selling - it's one of structured, disciplined hedging by sophisticated players paying whatever it costs to own downside insurance.

VanEck's historical analysis cuts both ways. The firm found that when similar options skew readings appeared over the past six years, they were followed by average bitcoin price gains of 13% over 90 days and 133% over 360 days. Fear at this level, historically, marks turning points - not fresh breakdowns. But history doesn't always rhyme, and the macro context in March 2026 is uniquely hostile.

Rate Hike Probability Went from Zero to Twelve in Seven Days

The Fed narrative flipped faster than any point in the current cycle. (Pexels)

Two months ago, the consensus was that the Federal Reserve would cut rates in April 2026. Six weeks ago, that expectation shifted to "no cut, but no hike either." This week, the CME FedWatch tool began showing a non-trivial 12% probability of an actual rate hike at the April FOMC meeting - up from 0% just seven days earlier. (Source: CME FedWatch, March 20, 2026)

What broke the narrative? A sequence of overlapping shocks, each individually survivable, together constituting a macro regime change. February's CPI reading showed headline inflation at 2.4% and core at 2.5% - both above the Fed's 2% target. Then the Iran war started. WTI crude exploded roughly 50% in three weeks. Energy costs feed directly into headline inflation, and the February readings predate all of that. The April CPI print is going to be ugly.

The macro shock sequence from Iran war to bond selloff to rate hike odds. (BLACKWIRE)

The bond market is already pricing the new reality. The 10-year U.S. Treasury note hit 4.38% on Friday, up from under 4% at the start of March. That's 38 basis points in three weeks - a violent move for a benchmark that tends to shift in single-digit basis point increments under normal conditions. (Source: CoinDesk, March 20, 2026)

The selloff isn't domestic. In the U.K., 10-year gilt yields crossed 5% - up roughly 15% in a month and at the highest level since 2008, the year of the global financial crisis. Markets are repricing the entire global risk-free rate, and that re-pricing is nowhere near finished. (Source: CoinDesk)

"Bitcoin has once again acted as the canary in the macro coal mine. At current levels, bitcoin is already pricing a recession, while many traditional assets are not." - Andre Dragosch, European Head of Research, Bitwise

The S&P 500 fell below its 200-day simple moving average on Thursday for the first time since May 2025. That's technically significant - not because a single indicator is definitive, but because it represents the weight of accumulated selling pressure breaking through a widely-watched floor. The index is now down more than 5% since late February and logged four consecutive weekly losses. The Nasdaq is down similarly, including a 1.2% decline on Friday alone.

Gold ran violently higher in the days after the war started, hitting $5,500 per ounce at peak. But as oil remained elevated and rate hike speculation grew, even the classic safe-haven broke. Gold is now at $4,569, down roughly 17% from its peak in three weeks. Silver crashed from $95 to $69.50. The traditional flight-to-safety playbook isn't working, and that's forcing capital to make hard choices about where to park during a stagflationary shock.

Strategy's 761,068 BTC: The Most Expensive Conviction in Financial History

Strategy's accumulation continues even as bitcoin sits 40% below its all-time high. (Pexels)

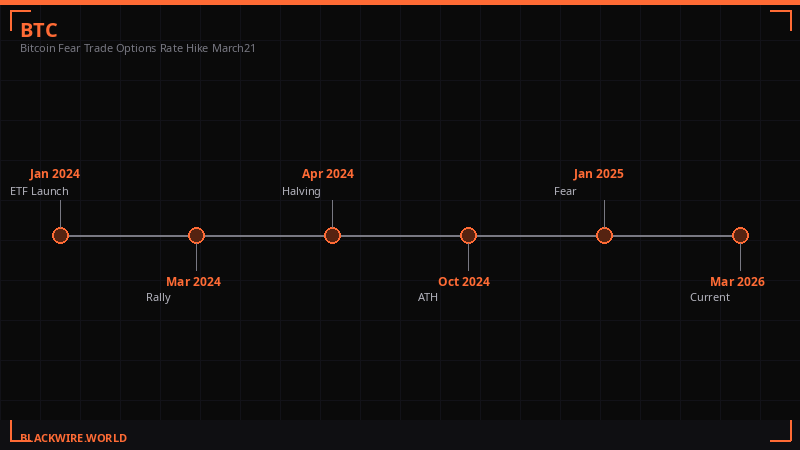

While options markets flash peak fear and bond markets crumble, one institution is doing the opposite of hedging. Strategy - the Michael Saylor-led software-company-turned-bitcoin-treasury - has bought 89,618 BTC in Q1 2026, pushing its total holdings to 761,068 BTC. With two Mondays remaining in the quarter, that number is likely to grow. (Source: CoinDesk/strategy.com, March 21, 2026)

The only quarter with a larger accumulation was Q4 2024, when Strategy added 194,180 BTC as bitcoin's price surged 40% from $70,000 to $100,000 following Trump's election victory. That quarter, including a single Monday in November when the company bought 55,500 BTC in one announcement, was the apex of the bull run. Q1 2026 is shaping up as the second-largest buying quarter - while the price is doing the opposite of that 2024 rally.

Q1 2026 is Strategy's second-biggest buying quarter ever, despite BTC sitting 40% off all-time highs. (BLACKWIRE/strategy.com data)

Bitcoin's price has fallen over 40% from its October 2025 all-time high of $126,000. Strategy's own common stock (MSTR) is down 15% from the start of Q1. The company's recent purchases have been partly funded by sales of its perpetual preferred offering called Stretch (STRC), which accounted for up to 15,000 BTC worth of buying over the past two weeks.

But STRC hit a wall this week. The preferred instrument failed to reach its $100 par value, making further utilization of that funding mechanism temporarily unavailable. Strategy's accumulation is capital-availability-driven, not just price-conviction driven. When the funding vehicle breaks down, the buying pace is constrained - regardless of what Saylor says on X about infinite accumulation. (Source: CoinDesk, March 21, 2026)

The math on Strategy's position is brutal at current prices. At $70,426 per BTC, the 761,068 BTC position is worth approximately $53.6 billion. The company holds somewhere in the range of $8-10 billion in debt financing tied to this position. The average cost basis on the full stack is estimated around $65,000-$68,000 per BTC based on disclosed purchase history. At $70K spot, they're in the black - but barely, and with massive leverage.

The bear case is straightforward: if bitcoin drops to $55,000, the entire enterprise is underwater on a mark-to-market basis. The bull case is equally simple: Strategy is buying bitcoin that institutional allocators will eventually need to own, at prices 40% below peak, funded by instruments that cost them less than the long-term expected appreciation. Whose logic wins is what the next six months will decide.

Morgan Stanley Files MSBT: Wall Street's Next Bitcoin ETF Move

Morgan Stanley joins the spot Bitcoin ETF race with ticker MSBT. (Pexels)

Morgan Stanley filed updated paperwork with the SEC on Friday for its planned spot bitcoin ETF, disclosing the ticker MSBT and a $1 million seed capital commitment at launch. The filing revealed a 10,000-share creation unit requirement and confirmed BNY Mellon as cash and administrative handler, with Coinbase as prime broker and bitcoin custodian. (Source: SEC filing, March 20, 2026)

This is not a speculative filing - the bank bought two shares earlier in March for audit purposes, a routine step in the ETF readiness process. The product architecture mirrors the BlackRock IBIT playbook almost exactly, which is intentional. IBIT has attracted over $56 billion in investor inflows since launching in January 2024 and remains the dominant vehicle for institutional bitcoin exposure in the U.S. (Source: CoinDesk)

If MSBT gets SEC approval, it will be the 12th spot bitcoin ETF trading in the U.S. market. The question is whether it launches into a market hungry for more institutional product or into a market already saturated, with a declining bitcoin price scaring off the very wealth management clients Morgan Stanley serves.

Morgan Stanley also filed for a Solana ETF earlier this year but has not submitted any amendments to that application. The solana product appears to be in a holding pattern, while the bitcoin product is moving actively toward launch. Given that Solana is down significantly from 2025 highs and facing renewed validator competition from new Layer-1 networks, the timing of that pause is rational.

The MSBT filing represents the institutional consensus: bitcoin is a permanent asset class. The conviction is so strong that the largest bank by wealth management AUM is going through the full regulatory apparatus to offer exposure - even as BTC sits 40% below peak and rate hike fears mount. That's not a trade. That's a structural allocation bet on 5-10 year timeframes.

Coinbase Goes "Everything Exchange": Stock Perps for Non-U.S. Traders

Coinbase's Everything Exchange strategy now includes perpetual futures on Magnificent 7 stocks. (Pexels)

Coinbase dropped a product on Friday that blurs the line between crypto exchange and stock exchange: perpetual futures contracts on U.S. large-cap equities for non-U.S. retail and institutional traders. The contracts cover the Magnificent 7 - Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta, and Tesla - plus SPY and QQQ ETF perpetuals in select jurisdictions. (Source: Coinbase blog, March 20, 2026)

The mechanics: contracts have no expiry date (perpetual), settle in USDC, and offer up to 10x leverage on individual stocks and up to 20x on ETF products. Trading runs 24 hours a day, 7 days a week - something no traditional stock exchange offers. The risk engine is the same one Coinbase uses for its crypto derivatives, with cross-margining across perpetual futures and spot positions.

Why does this matter right now? Because the demand for 24/7 equity exposure has been exploding. Decentralized platforms - primarily Hyperliquid - have been absorbing this demand rapidly. Hyperliquid launched S&P 500 perpetual futures just days earlier, and the platform saw oil-linked contracts surge 5% in a single session after U.S.-Israeli strikes on Iran. Coinbase is explicitly chasing that market, bringing it into a regulated, custodied environment. (Source: CoinDesk)

The implication is structural: the boundaries between crypto exchanges and stock exchanges are dissolving. When you can trade NVIDIA perps 24/7 on the same platform where you trade BTC, the institutional case for maintaining separate equity and crypto desks starts to break down. Trading desks that run both can run them from a single custody and collateral stack. That's a genuine efficiency gain, and it's what Coinbase is selling under the "Everything Exchange" branding.

The irony of launching stock perps during a week when the S&P 500 broke below its 200-day moving average is not lost on anyone paying attention. Coinbase's new product line is being introduced precisely when equity markets are under the most stress since mid-2025. Whether that creates a flood of short positions on the new platform, or deters cautious institutional adoption, will be visible in volume data over the coming weeks.

SBF's Prison Pardon Play: Backing Trump's Iran Strikes from Behind Bars

Sam Bankman-Fried is playing the one card he has left: public alignment with the president. (Pexels)

Sam Bankman-Fried - convicted of fraud, currently serving a 25-year sentence stemming from the collapse of FTX in November 2022 - is trying to get out of prison by becoming Donald Trump's most public crypto endorser. Through prison-approved communications on X, posted via proxy, Bankman-Fried this week backed Trump's strikes against Iran, framing the military operation as necessary to neutralize nuclear risk. (Source: CoinDesk, March 21, 2026)

This isn't a sudden conversion. In earlier posts, SBF pointed to lower U.S. gas prices under Trump compared to the Biden era. He credited Trump with "saving" the SEC by replacing former Chair Gary Gensler with Paul Atkins, arguing the change reduced inter-agency conflict and eased regulatory pressure on crypto firms. Each statement is calculated. Each one builds the narrative that SBF is aligned with the president's agenda.

The playbook has worked before. Ross Ulbricht, who ran the Silk Road dark market and was sentenced to life without parole in 2015, was freed by Trump shortly after his second inauguration in January 2025. The Ulbricht pardon was widely seen as a gift to the libertarian crypto community that backed Trump. If the president is willing to pardon a convicted darknet market operator, the argument goes, a high-profile crypto fraud conviction might not be off the table.

The odds remain long. FTX's collapse wiped out approximately $8 billion in customer funds and triggered a market-wide contagion that took down Celsius, BlockFi, and Genesis. The political fallout from pardoning SBF - given the scale of retail investor losses - would be significant. Bankman-Fried's lawyers filed a motion for a new trial in February 2026, which the government opposed. The public messaging is a parallel track: shape the narrative while the legal process grinds along.

One concrete development moving in parallel: the FTX Recovery Trust announced it will distribute approximately $2.2 billion to creditors as part of the ongoing Chapter 11 process. Recovery rates are approaching full repayment for many claim classes - an outcome that seemed impossible when the exchange imploded in 2022. Whether that recovery record influences any future clemency consideration is speculative, but Bankman-Fried's team will certainly frame it that way.

The Macro Setup Heading Into April: What Breaks Next

The April FOMC decision is the next hard catalyst for markets under pressure. (Pexels)

The week of March 17-21 delivered a concentrated burst of macro noise. Six major economies - the U.K., France, Germany, Italy, the Netherlands, and Japan - issued a joint statement condemning Iran's attacks and pledging to take steps to stabilize energy markets and ensure safe passage through the Strait of Hormuz. That triggered a brief oil pullback: WTI fell nearly 2% to $93.80. Bitcoin popped to $70,800. Then the weekend arrived, and none of the underlying dynamics changed. (Source: CoinDesk, March 20, 2026)

The macro calendar heading into April is dangerous. The Fed's next FOMC meeting is in April. That 12% rate hike probability may sound small, but it was 0% a week ago. If March CPI comes in above 3% - which energy prices make plausible - that probability moves materially higher. Markets that have not priced a rate hike in over two years will have to reprice everything: bond yields, equity multiples, crypto risk premiums.

U.S. Treasury Secretary Scott Bessent floated the idea Thursday of removing sanctions from Iranian oil tankers and releasing crude from the Strategic Petroleum Reserve. If those moves materialize, oil breaks lower and the rate hike narrative deflates. If they don't, the April CPI print lands hot, and the Fed's options narrow sharply. (Source: CoinDesk, March 20, 2026)

Bitcoin's position in this environment is strange but not incoherent. It's down 40% from its 2025 peak - absorbing the macro headwinds faster and more completely than equities. Bitwise's Andre Dragosch argued Friday that at current levels, bitcoin is already pricing a recession. If he's right, bitcoin may be the first asset to finish repricing, which means it could also be the first to bottom. The options market's extreme fear reading - historically a contrarian signal - points in the same direction. But "historically" carries an asterisk when the macro regime is as unusual as this one.

The game theory is: if you think the Iran conflict de-escalates, oil pulls back, CPI surprises to the downside, and the Fed holds, then bitcoin at $70K is cheap. If you think the conflict expands, oil stays above $90, CPI runs above 3%, and the Fed hikes in April, then the put buyers are correct to pay record premiums. Both scenarios are plausible. The 12% hike probability means the market is not pricing either as certain - just as genuinely two-sided. That's the first time since 2022 that "two-sided" meant a hike was back on the table at all.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram