The $70 Billion Pivot: Bitcoin Miners Are Selling BTC to Build AI Data Centers

The average public miner spent $79,995 to produce one bitcoin last quarter. Bitcoin is trading at $66,368. That math produces one outcome: the industry is cannibalizing itself, selling the asset it exists to produce in order to fund a complete transformation into something else entirely - AI data centers with $70 billion in contracts already on the table.

The bitcoin mining industry has crossed a structural threshold. Not the kind you recover from by waiting for price to recover. The kind where the incentive structure inverts, capital allocators make permanent decisions, and an entire sector rewrites its identity to stay solvent.

This is that moment. And it's accelerating faster than most participants anticipated.

The Numbers That Broke the Industry

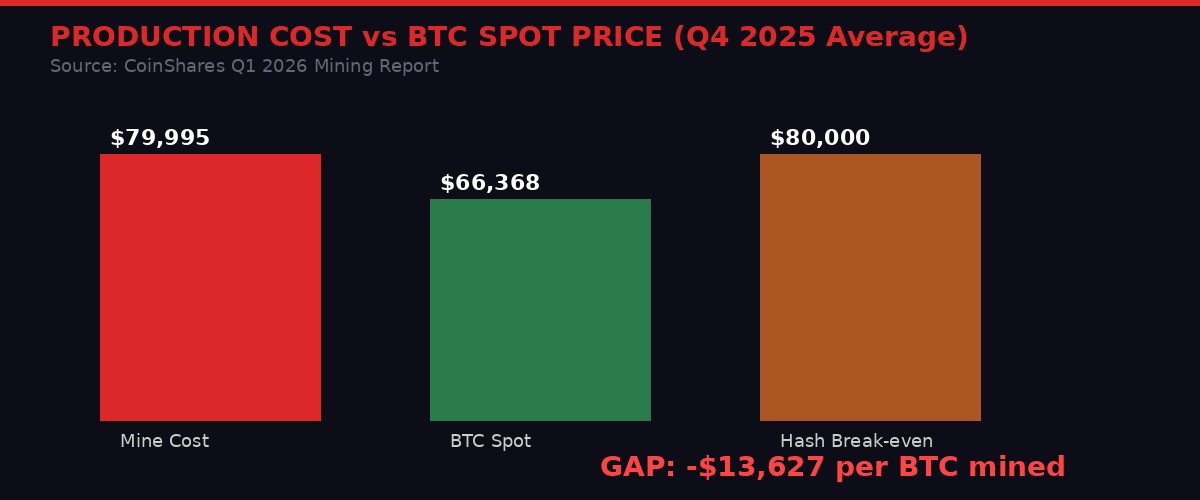

The CoinShares Q1 2026 mining report, published this week, landed with the subtlety of a collapsed hash-ribbon. The weighted average cash cost to produce one bitcoin among publicly listed miners reached approximately $79,995 in Q4 2025. That figure incorporates electricity, hardware depreciation, hosting costs, and operational overhead across the sector's largest public operations.

Bitcoin was trading at $68,000 to $70,000 when that report was compiled. It's at $66,368 as of Friday's close. The effective per-coin loss has widened to nearly $13,627 - a number that, if sustained, makes continued mining not just economically painful but structurally irrational.

CoinDesk reported last week that miners were losing approximately $19,000 per BTC produced at lower hash price estimates. The range varies by miner - those with access to sub-$0.05 per kilowatt-hour electricity and next-generation hardware are closer to breakeven. Most are not. (Source: CoinDesk, March 22, 2026)

Hash price - the metric tracking miner revenue per petahash per day - hit an all-time post-halving low of approximately $28 to $30 per petahash per day in early March. For context: that's the revenue signal that determines whether running a miner is profitable at any given electricity rate. At those levels, you need power below $0.05/kWh to stay above water. Global average industrial power rates hover between $0.06 and $0.09/kWh.

The hashrate tells its own story. The Bitcoin network peaked at approximately 1,160 exahashes per second in early October 2025. It has since declined to roughly 920 EH/s, with three consecutive negative difficulty adjustments - the first such streak since July 2022. Machines are going offline. The economics are doing what economics always do: they force decisions.

$70 Billion in AI Contracts: The Pivot in Numbers

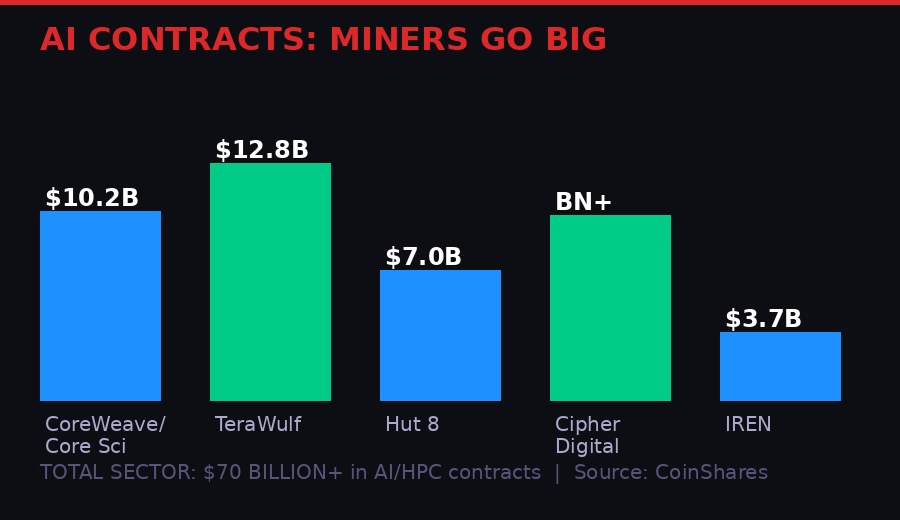

The response to unworkable economics has been staggering in scale. According to the CoinShares report, over $70 billion in cumulative AI and high-performance computing contracts have now been announced across the public mining sector. These are not letters of intent. These are multi-year deals with known counterparties, fixed rates, and construction timelines.

The breakdown by company illustrates how structural this shift has become:

| Company | AI/HPC Partner | Contract Value | Term |

|---|---|---|---|

| Core Scientific | CoreWeave | $10.2 billion | 12 years |

| TeraWulf | HPC customers | $12.8 billion | Multi-year |

| Hut 8 | AI infrastructure lease | $7 billion | 15 years |

| Cipher Digital | Google-backed Fluidstack | Multi-billion | Multi-year |

| IREN | GPU capacity (200 MW) | Scaling | Ongoing |

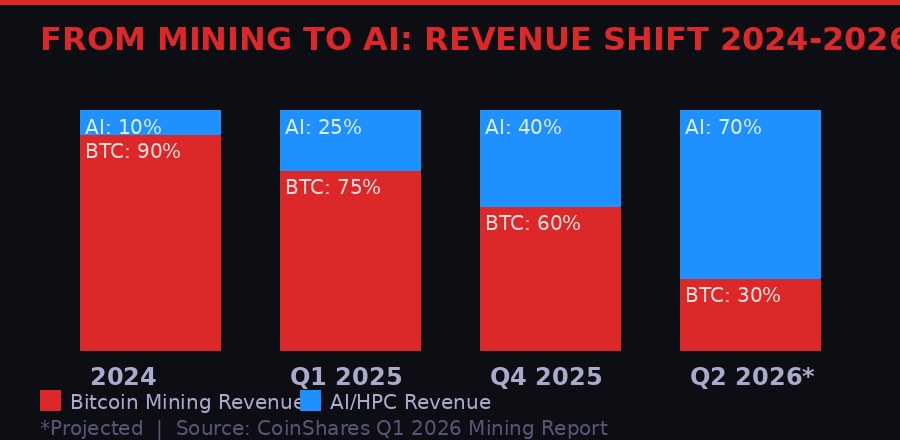

Core Scientific's AI colocation revenue already accounts for 39% of its total revenue. TeraWulf is at 27%. IREN is at 9% and deploying up to 200 megawatts of liquid-cooled GPU capacity. These are not pilot programs. These are operational revenue streams growing quarter over quarter.

The sector projection by year-end 2026 is stark: listed miners could derive as much as 70% of their revenue from AI, up from roughly 30% today. The companies are not "also doing AI." They are becoming AI infrastructure operators that happen to still mine bitcoin on the side.

"The cost differential between bitcoin mining infrastructure at roughly $700,000 to $1 million per megawatt and AI infrastructure at $8 million to $15 million per megawatt is wide, but AI offers structurally higher and more stable returns." - CoinShares Q1 2026 Mining Report

That math is brutal in its clarity. AI infrastructure capex runs 8 to 15 times the cost per megawatt compared to mining buildouts - but delivers margins above 85% with multi-year revenue visibility. Versus a mining operation currently losing $13,627 per coin produced with zero revenue certainty beyond the spot price. The capital allocation decision makes itself.

Selling the Asset You Mine to Fund the Pivot

The pivot is being financed two ways - and both show up directly in the on-chain and regulatory data.

First: debt at infrastructure scale. The mining sector's aggregate leverage has changed category. IREN now carries $3.7 billion in convertible notes across five series. TeraWulf has $5.7 billion in total debt across convertible and senior secured notes at its compute subsidiary. Cipher Digital issued $1.7 billion in senior secured notes in November - its quarterly interest expense jumped from $3.2 million for the first nine months of the year to $33.4 million in Q4 alone. These are not mining company debt loads. These are the balance sheets of companies building out data center infrastructure. (Source: CoinShares Q1 2026 Mining Report, company 10-Ks)

Second - and this is where it gets uncomfortable for Bitcoin holders: they are selling bitcoin. A lot of it.

Publicly listed miners have collectively reduced their BTC treasuries by over 15,000 BTC from peak levels. The sales register reads like a who's-who of the industry:

- Core Scientific: Sold roughly 1,900 BTC worth $175 million in January. Planning to liquidate substantially all remaining holdings in Q1 2026.

- Riot Platforms: Sold 1,818 BTC worth $162 million in December 2025.

- Bitdeer: Reduced its BTC treasury to zero in February 2026.

- Marathon Digital: The largest public holder at 53,822 BTC quietly expanded its policy in its March 10-K to authorize sales from its entire balance sheet reserve, partly driven by its $350 million bitcoin-backed credit facility where loan-to-value climbed to 87% as prices fell toward $68,000.

The miners selling BTC to fund AI buildouts are the same companies whose mining operations secure the Bitcoin network. When mining is unprofitable and AI is lucrative, rational capital reallocates away from mining. If enough miners make that call simultaneously, the network's security budget - the total hashrate backing transaction finality - shrinks. Three consecutive negative difficulty adjustments suggest this process has already started.

The hashrate decline from 1,160 to 920 EH/s represents a 20.7% reduction in network security since October. Not a crisis yet - the network's difficulty adjustment is designed to absorb exactly this kind of shift. But the trajectory is visible in the data and the incentive structure creating it shows no signs of reversing at current prices.

The Hashrate Reckoning

CoinShares forecasts the network hashrate will reach 1.8 zetahashes by end of 2026 and 2 zetahashes by end of March 2027. Those figures are one month later than previously predicted, acknowledging that the timeline has slipped.

The catch is the assumption embedded in those forecasts: they require bitcoin recovering to $100,000 by year-end. If prices stay below $80,000, CoinShares explicitly expects hash price to continue falling and hashrate to decline further as more miners exit.

A sustained move below $70,000 could trigger larger capitulation. Paradoxically, that would benefit surviving miners through lower difficulty adjustments - the remaining hash power gets a larger share of the fixed block reward. But the short-term damage to miner balance sheets and the network's PR narrative around security would be significant.

Next-generation hardware offers a partial lifeline. Bitmain's S23 series and Bitdeer's proprietary SEALMINER A3 - both operating below 10 joules per terahash - are expected at scale through H1 2026. These machines would roughly halve the energy cost per bitcoin compared to current mid-generation fleets. But deploying them requires capital that most miners are currently routing toward AI instead. The hardware exists. The capital allocation decision is going elsewhere.

The Market Has Already Priced the Bifurcation

The equity market has done what equity markets do - it priced the shift before the sector fully acknowledged it.

According to the CoinShares data, miners with secured HPC contracts now trade at 12.3 times next-twelve-month sales. Pure-play miners trade at 5.9 times. The market is paying more than double for AI exposure in the same sector. That premium does two things simultaneously: it rewards companies that have signed AI contracts, and it creates a powerful financial incentive to sign more of them.

The valuation signal reinforces the transformation. Every quarter that passes without AI contract announcements is a quarter where a mining company watches its peer group trade at twice its multiple. The market has essentially told the sector: stop being miners, start being data centers.

Geographic distribution is also shifting. The United States, China, and Russia now control roughly 68% of global hashrate, with the U.S. gaining about 2 percentage points of market share in Q4 alone. Emerging markets are entering the mix - Paraguay and Ethiopia have joined the global top 10 mining countries, driven by HIVE's 300-megawatt operation in Paraguay and Bitdeer's 40-megawatt Ethiopia facility. These low-cost jurisdictions may end up inheriting a larger share of the pure-play mining business as U.S. operators pivot to AI. (Source: CoinShares Q1 2026 Mining Report)

ETF Outflows and the Macro Headwinds Compressing Bitcoin

The miner crisis doesn't exist in isolation. The bitcoin price that's crushing mining economics is itself a product of deteriorating macro conditions that compounded through March 2026.

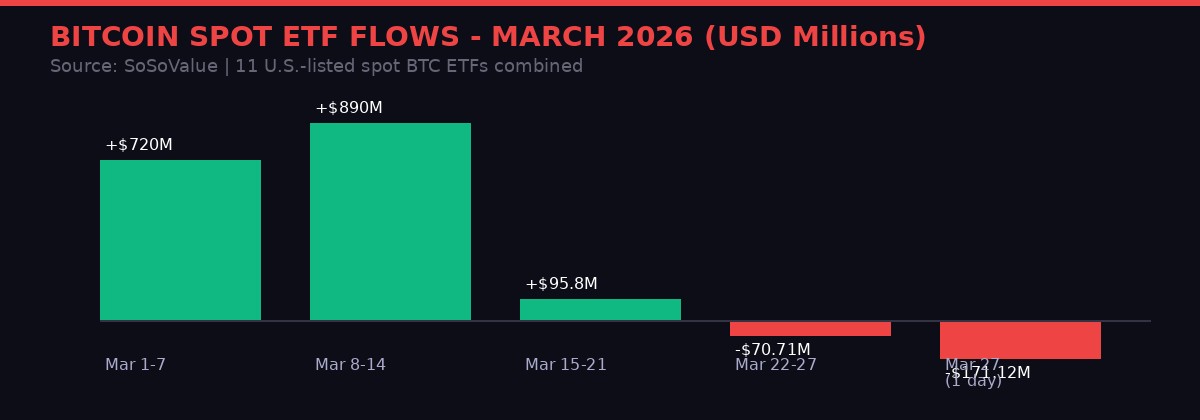

On Thursday, investors withdrew a combined $171.12 million from the 11 U.S.-listed spot bitcoin ETFs - the largest single-day outflow in over three weeks, per SoSoValue data. BlackRock's IBIT saw $41.92 million in outflows. Fidelity's FBTC, GBTC, BITB and ARKB each recorded $20-30 million withdrawals. This follows a period of robust inflows - the funds attracted more than $2 billion between late February and mid-March. Since then, the momentum has reversed hard. Net outflows of $70.71 million so far this week. (Source: SoSoValue, March 27, 2026)

The macro picture explains the institutional hesitation. The 10-year U.S. Treasury yield is approaching 4.5% - its highest level since July 2025. The MOVE index, which tracks U.S. bond market volatility, spiked 18% in 24 hours. Oil remains above $100 per barrel, with WTI and Brent both rising 3% as Ukraine's disruption of Russian oil flows complicates Trump administration plans to ease energy supply pressure. The DXY dollar index is moving toward 100, creating structural headwinds for risk assets. (Source: CoinDesk, March 27, 2026; Coinglass)

Nearly $300 million in long bitcoin futures positions were liquidated in a single 24-hour window on Friday - the fifth time in 10 days that longs have taken that level of punishment. The positioning tells the story: traders were repeatedly betting that the Iran war would translate into a flight-to-crypto narrative. That trade has not materialized. Every bounce got sold.

Glassnode's Accumulation Trend Score data confirms who's doing the selling. Retail wallets under 1 BTC carry an accumulation score of 0.11. Wallets holding 1 to 10 BTC are at 0.05 - near-maximum distribution. Whales holding 1,000 to 10,000 BTC sit neutral at 0.5 - neither accumulating nor distributing at scale. The largest cohort, 10,000+ BTC holders, show mild distribution but nothing resembling the aggressive selling seen when bitcoin was above $90,000. The picture: retail is capitulating, whales are watching. (Source: Glassnode, March 27, 2026)

The Macro Pressure Dashboard

The convergence of macro signals hitting bitcoin simultaneously is not coincidence. It's the arithmetic of a risk-off environment compressing every asset class that requires optimism to hold.

Iran's war now entering its fifth week without resolution has done something specific to the market. Early war-stage trading produced a brief flight-to-Bitcoin narrative - the "digital gold in geopolitical chaos" thesis. That thesis failed. Bitcoin has lost roughly 25% from its January highs while gold has held and in some periods strengthened. The war narrative that was supposed to be a bullish catalyst became a source of persistent risk-off pressure as oil spiked, treasury yields climbed, and equity markets entered correction territory.

The Nasdaq 100 is trading at 23,760 - 10% below the January 2026 high. Bitcoin options worth over $15 billion expired Friday with the $75,000 "strike magnet" no longer providing upside support. Bitcoin and ether puts are trading at 6 to 8 volatility points of premium over calls across all expirations. The market is paying meaningful money to protect against further downside.

Morgan Stanley's entry into the bitcoin ETF race - pricing its proposed spot bitcoin fund at 14 basis points, the lowest fee on the market if approved - suggests institutional infrastructure build continues. The medium-term demand picture is not broken. But short-term, every macro indicator is pointing the wrong direction. (Source: CoinDesk, March 27, 2026)

What Happens Next: Two Scenarios

The bitcoin mining industry's transformation now hinges on a single variable. Not hashrate, not difficulty, not hardware efficiency. The price of bitcoin.

Scenario A: Price recovers to $100,000 by year-end. Mining margins flip positive. Hash price rises toward levels that make mid-generation hardware viable again. The AI pivot slows - not reverses, but slows. Companies with secured AI contracts keep running them because the revenue is good. But they also restart aggressive bitcoin mining with upgraded hardware. The sector ends up diversified rather than transformed. CoinShares' hashrate forecast of 1.8 zetahashes by end-2026 becomes achievable.

Scenario B: Bitcoin stays at $70,000 or below. The economics of mining remain structurally negative. AI pivot accelerates. More miners zero out their BTC treasuries to fund infrastructure buildouts or service debt. Hashrate continues declining through mid-year. The capitulation benefits the survivors through lower difficulty but creates a narrative problem - the world's largest public blockchain is processing transactions with 25-30% less security than six months ago. Pure-play miners in Ethiopia and Paraguay pick up the hashrate that U.S. operators abandon. The U.S. mining industry's dominant position erodes as capital reallocates to AI.

The market is pricing Scenario B with higher probability. The $66,368 spot price, the persistent negative funding rates, the ETF outflows, the whale neutrality - none of these are the fingerprints of a market positioning for a $100,000 recovery.

The bitcoin mining industry entered this cycle as a group of companies whose core function was securing a blockchain and accumulating the asset that blockchain produced. It is exiting - if current trajectories hold - as a group of AI infrastructure operators that still happen to run some ASICs on the side.

That is not a failure. It may be the rational survival move that keeps these companies solvent through a brutal cycle. But it represents a structural shift in who secures the Bitcoin network, and what motivates them to do it. The long-term implications - for network security, for block subsidy economics after the next halving, for the Bitcoin-as-digital-gold narrative - are not priced into any model. Not yet.

The $70 billion pivot is real. The math driving it is real. Where it ends depends on a number: $70,000, or $100,000. Everything else is a consequence of that.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram