From Hodl to Hedge: Bitcoin's Corporate Treasury Orthodoxy Is Fracturing

MARA Holdings sold 15,133 BTC for $1.1 billion to retire debt at a discount. GameStop pledged its entire bitcoin stack to Coinbase and started writing covered calls. David Sacks, the architect of Washington's pro-crypto pivot, quietly exited his czar role. And Maxine Waters put a letter on the Kansas City Fed's desk demanding answers about Kraken's historic master account access. All of it happened in the same 72-hour window. The bitcoin corporate treasury playbook - the one Saylor wrote, the one every CFO panel endorsed - is being rewritten in real time.

Market data as of March 27, 2026, 04:30 CET. BTC near $68,800. Gold down 15% MTD. Oil above $100.

Key Numbers - March 26-27, 2026

The Macro Backdrop: War, Oil, and Bond Yields Are Tearing Up the Playbook

Markets globally have been whipsawed since the Iran war escalated in late February 2026.

Before you can understand what is happening inside corporate bitcoin treasuries this week, you need to understand the macro backdrop. Because everything - the MARA sell, the GameStop pivot, the Fed master account politics - is downstream of what oil, bonds, and geopolitics have done to capital markets since the Iran conflict exploded.

The U.S. 10-year Treasury yield was sitting below 4% just weeks ago, keeping corporate debt manageable and crypto assets buoyant. By Thursday March 26, it had surged to 4.43% intraday before pulling back slightly, per CoinDesk. That is a brutal 43-plus basis point move in a matter of weeks. Not just bad for crypto prices - catastrophic for any company sitting on leveraged positions or convertible debt structures that were priced for a different world.

Oil above $100 per barrel since the outbreak of Middle East hostilities is the inflation multiplier that changes every Fed calculation. Expectations for Federal Reserve rate cuts have not just evaporated - there are active bets now that the Fed will hike. Similar dynamics are playing out across Western Europe. The era of cheap money that enabled the original "stack bitcoin with leverage" model is, for now, over.

Bitcoin itself has shown surprising resilience. It initially fell hard from its October 2025 all-time high near $108,000 - briefly touching the low-$60,000 range in the immediate panic phase. But it has since stabilized in the $69,000-$70,000 range even as equities continue to bleed. The Nasdaq is now down roughly 10% from its late January highs. Bitcoin, for its part, is down far less on the same timeframe.

Trump extended his pause on U.S. attacks against Iran's energy infrastructure to 10 days on Thursday, citing ongoing diplomatic talks. He posted on Truth Social: "As per Iranian Government request - I am pausing the period of Energy Plant destruction by 10 Days. The talks are ongoing and going very well." That news briefly sent bitcoin up 1% from session lows. Markets are now structurally hostage to a geopolitical timer that resets every ten days.

This is the environment in which corporate bitcoin treasuries are making decisions. And the decisions they are making this week reveal a lot about the limits of the original playbook.

JPMorgan's Wednesday report noted gold's market breadth has fallen below bitcoin's - a historic divergence. Source: JPMorgan, CoinDesk.

MARA Holdings: The Biggest Corporate Bitcoin Seller of 2026 (So Far)

MARA Holdings operates one of the world's largest bitcoin mining and treasury operations.

Marathon Digital Holdings - now operating as MARA Holdings - built its identity around two things: mining bitcoin and never selling it. The company has spent years accumulating coins, issuing convertible debt at 0% interest to fund purchases, and positioning itself as the institutional "always buy, never sell" mirror to MicroStrategy's "always lever, never stop" strategy.

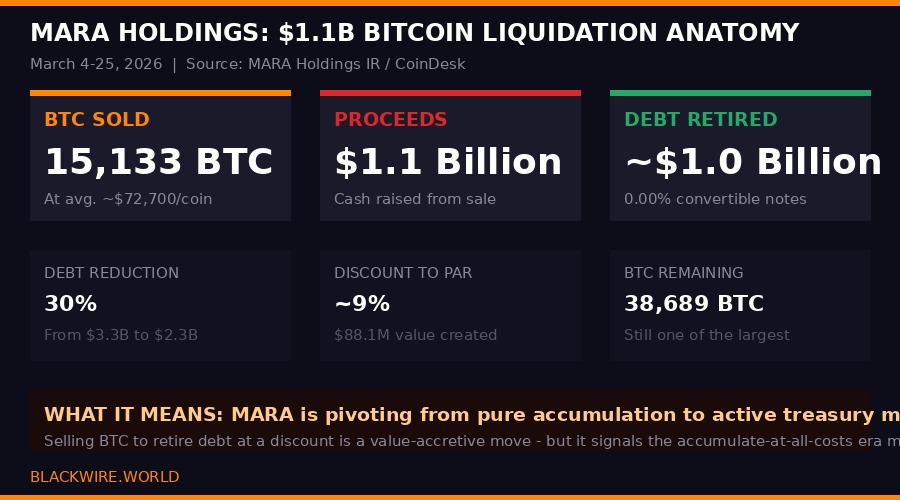

That identity is now complicated by a single transaction. Between March 4 and March 25, MARA sold 15,133 BTC for approximately $1.1 billion, per the company's press release. The proceeds funded a buyback of roughly $1.0 billion of its 0.00% convertible senior notes due 2030 and 2031 - at a discount to face value.

The math is elegant. MARA bought back $367.5 million of its 2030 notes for $322.9 million, and $633.4 million of its 2031 notes for $589.9 million. The combined discount to par of approximately 9% generates roughly $88.1 million in pure accounting value - cash left on the table by note holders who wanted out early. The company's total convertible debt drops from around $3.3 billion to $2.3 billion, a 30% reduction.

"Our decision to sell a portion of our bitcoin holdings reflects a strategic capital allocation move designed to strengthen our balance sheet and position the company for long-term growth." - Fred Thiel, CEO of MARA Holdings (CoinDesk, March 26, 2026)

MARA stock jumped 10% in premarket trading on the announcement. The market apparently loves the deleveraging story more than it mourns the reduced BTC stack. MARA now holds 38,689 BTC - still one of the largest corporate bitcoin positions on earth - but down from a peak above 50,000 coins. The sale averaged roughly $72,700 per coin, meaning MARA got out at prices that look like relative value compared to where BTC is trading today.

Anatomy of MARA's bitcoin sell operation: March 4-25, 2026. 15,133 BTC sold at avg. ~$72,700. Source: MARA IR.

The strategic logic is sound. When your debt carries a 0% coupon and trades at a 9% discount, selling bitcoin near $72,000 to retire it is a compelling IRR trade. It reduces dilution risk - those convertible notes could eventually become MARA shares, flooding the cap table. And it shrinks the debt load at a moment when higher bond yields are making leveraged structures more expensive to roll.

But here is what the trade signals beyond its immediate mechanics: MARA is now running an active treasury, not a passive accumulation vault. The "never sell" era is over for the second largest publicly traded bitcoin miner. The company still has substantial exposure and is still structurally long BTC. But it has now demonstrated a willingness to liquidate positions when the capital structure math demands it. That is a meaningful shift in corporate behavior - and it will affect how other companies in the space are evaluated.

Thiel's statement also hints at MARA's next chapter. "Expansion into AI and energy infrastructure" appeared in the company's framing of the deal. This is consistent with a broader trend of bitcoin miners seeking alternative revenue streams as post-halving mining economics tighten and AI data center demand for power creates opportunities to monetize their energy infrastructure differently. The bitcoin treasury is being reshaped to fund a different business model.

Corporate bitcoin holdings landscape as of March 27, 2026. Strategy dominates at 528,185 BTC. Source: Company filings.

GameStop: The Meme Stock Becomes a Derivatives Desk

GameStop's fiscal year 2026 annual SEC filing revealed a sophisticated OTC options strategy around its bitcoin position.

GameStop's bitcoin story just got significantly stranger. When the company transferred nearly its entire 4,710 BTC stack to Coinbase Prime in January 2026, the move triggered widespread speculation: was the meme stock retailer dumping its crypto holdings under pressure? Was management losing faith in its own bitcoin bet?

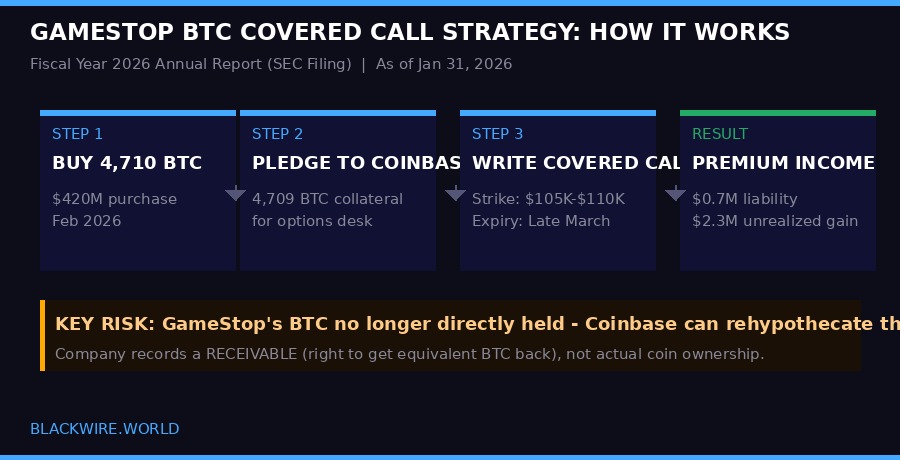

The company's fiscal year 2026 annual report, filed with the SEC on Tuesday and reviewed by CoinDesk, reveals the actual answer. GameStop pledged 4,709 of its 4,710 BTC to Coinbase as collateral for an over-the-counter covered call strategy. The company has been writing short-dated call options on its bitcoin, with strike prices between $105,000 and $110,000 and expiry dates through late March 2026.

The mechanics: by writing covered calls, GameStop collects option premiums from buyers who want upside exposure to bitcoin above those strike levels. If BTC never reaches $105,000 before expiry, the options expire worthless and GameStop keeps the premium as income. If BTC surges above the strikes, GameStop's gains are capped but it still profits from the premium plus the appreciation up to the strike level.

At current BTC prices around $68,800, those $105,000-$110,000 strikes are comfortably out of the money. The near-term options already expired unexercised per the annual report - meaning GameStop collected premium, the calls expired worthless, and the company is now sitting on collateral still held at Coinbase Credit. The SEC filing reports a $0.7 million liability linked to the options and a $2.3 million unrealized gain from the strategy so far.

How GameStop's covered call strategy works. Key risk: BTC is pledged as collateral - not directly held. Source: SEC Filing, CoinDesk.

But the accounting change is more significant than the options income. Because Coinbase can rehypothecate or redeploy the pledged bitcoin - meaning lend it out or use it as its own collateral - GameStop no longer classifies the assets as directly held coins. Instead, the company records a receivable: the legal right to reclaim equivalent BTC later. The 4,709 BTC appears on GameStop's balance sheet as $368.3 million worth of receivables at fiscal year-end, not as a direct coin holding.

The company also booked a $59.7 million unrealized loss tied to BTC's price decline since purchase. That is the mark-to-market pain of buying near $90,000+ per coin in early 2026 and watching prices pull back. The covered call income partially offsets this - but only partially. GameStop's bitcoin bet is underwater, and the company has responded by trying to generate yield rather than sitting passively on a losing position.

This is a fundamental change in posture. GameStop announced its bitcoin strategy in January 2026 with the language of treasury diversification and long-term conviction. Within two months, the company has pledged its entire position to a third party and started running an options book. Whether this is sophisticated treasury management or retail investors getting played is a question worth sitting with.

David Sacks Steps Down: The Policy Architect Exits Stage Left

Washington's crypto policy architecture is shifting with David Sacks exiting his czar role to take a broader science advisory position.

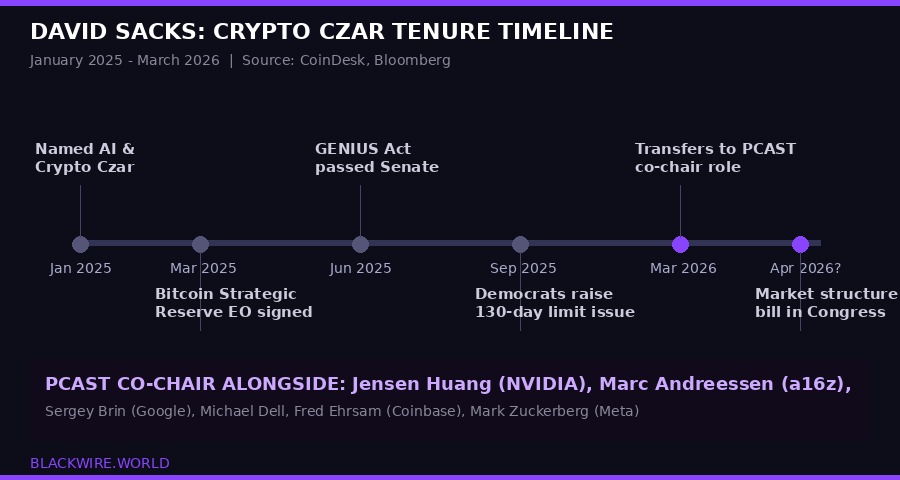

David Sacks - the PayPal Mafia veteran, Palantir backer, and X board member who became the most consequential figure in U.S. crypto policy in a generation - is no longer the White House's AI and crypto czar.

Sacks announced Thursday that he was transitioning to a new role as co-chair of the President's Council of Advisors on Science and Technology (PCAST), per CoinDesk. The czar position he is vacating was, by law, constrained. Sacks told Bloomberg the role was designated as a "special government employee" position, meaning he could only legally serve for 130 working days. Democrats had been raising red flags since September 2025 that he had already exceeded this limit.

His move to PCAST neatly solves the legal problem - the advisory committee role has no such constraint - while elevating him into a broader mandate covering AI, quantum computing, nuclear power, and what he described as "other cutting-edge technologies." Critically: he did not mention crypto once in his Bloomberg interview announcing the transition.

Sacks' policy achievements: Bitcoin Strategic Reserve, GENIUS Act stablecoin legislation, crypto market structure bill. Source: CoinDesk, Bloomberg.

"PCAST is the principal body of external advisors tasked with shaping science, technology, and innovation policy for the President and the White House. Thirteen of the world's most accomplished leaders in science and technology will join us." - David Sacks, via X post, March 26, 2026

What did Sacks actually accomplish during his 14-month run? More than most in Washington would have predicted. The Bitcoin Strategic Reserve executive order - one of the most significant moments in crypto's institutional legitimacy arc - came under his watch. The GENIUS Act, the first major federal stablecoin legislation to pass the Senate, was shepherded through by his team. Work on the crypto market structure bill - the comprehensive framework that could finally give the industry clear operating rules - is his legacy project now being handed to successors.

The PCAST lineup he is joining reads like a who's who of Silicon Valley's most powerful: Jensen Huang of NVIDIA, Marc Andreessen of a16z, Sergey Brin of Google, Michael Dell, Fred Ehrsam of Coinbase, Lisa Su of AMD, and Mark Zuckerberg of Meta, among others. Sacks will co-chair alongside Michael Kratsios, who has served in both Trump administrations. It is a powerful perch - arguably more powerful than the czar role - but it is a broader brief. Crypto gets a smaller piece of his attention going forward.

For the industry, the question is who fills the vacuum. The crypto market structure bill is the most urgent outstanding item. It could still pass this Congress, but it needs someone with Sacks' combination of technical fluency and political access to push it across the finish line. The transition announcement did not name a successor. Washington tends to fill these vacuums slowly.

Kraken vs. Maxine Waters: The Fed Master Account Fight Is Not Over

Kraken's Federal Reserve master account - the first ever granted to a crypto exchange - is drawing scrutiny from Congress.

Earlier this month, Kraken became the first cryptocurrency exchange in history to secure a Federal Reserve master account, specifically a "limited purpose" version granted by the Federal Reserve Bank of Kansas City. The move was historic - it gave Kraken direct access to the same payment rails that traditional banks use, bypassing the custodian banks and correspondent relationships that crypto firms have been forced to rely on.

But Representative Maxine Waters is not letting the announcement pass without scrutiny. Waters, the ranking Democrat on the House Financial Services Committee and a likely future chair if Democrats retake the House (Polymarket currently prices that at 84% probability), sent a letter Thursday to Kansas City Fed President Jeff Schmid demanding answers about the approval, per CoinDesk.

"The announcement raises questions about the approval because neither statute nor the Federal Reserve Board's Account Access Guidelines refer to a 'limited purpose account' type. Accordingly, I write to request that you clarify the terms of Kraken's account access approval and provide additional information regarding the process and considerations informing the approval." - Representative Maxine Waters, letter to Kansas City Fed President Jeff Schmid, March 26, 2026

Waters' core argument is legal and procedural: the term "limited purpose account" does not appear in the relevant statutes or in the Fed's own Account Access Guidelines. She is questioning whether the Kansas City Fed created a new category of account access without proper legal authority or adequate oversight of the approval process. She is also flagging potential consumer-protection concerns, though her letter does not elaborate on the specific risks she sees.

The Kansas City Fed's response to press inquiries was minimal: the bank has "received the letter and will review it." That is standard boilerplate from a regional Fed office that is not going to engage publicly with congressional correspondence before it has formulated an internal response.

The political stakes are significant. Several other crypto firms are still waiting for master account access - the Fed is also working on a separate "skinny" master account framework at the Board level in Washington that could govern these applications more broadly. If Waters can cast doubt on the legal foundation of Kraken's approval, she could complicate access not just for Kraken but for every crypto firm waiting in line. The Fed's general position under its current guidelines, outlined in a 2022 document revised in 2023, is already restrictive about account access for novel charter types.

Kraken's victory also came in the immediate aftermath of another banking access drama: the Custodia Bank saga, in which Wyoming's crypto-focused chartered bank spent years fighting the Federal Reserve for master account access and ultimately lost its court case just as the Kansas City Fed opened the door to Kraken. That timing - a court closes one door while a regional Fed bank opens another - suggests the Biden-era restrictions are being selectively reversed under the current administration, but the legal framework governing those reversals is, apparently, unclear even to members of Congress.

JPMorgan's Warning: Gold Is Cracking, Bitcoin Is Not

Gold is down 15% month to date from its $5,500 all-time high in January. Bitcoin has proven comparatively resilient amid the same macro shock.

While corporate treasuries are reconfiguring their bitcoin positions, JPMorgan published an analysis Wednesday that challenges one of the foundational assumptions of modern portfolio construction: that gold is the superior safe-haven asset.

The bank's research team, led by analyst Nikolaos Panigirtzoglou, noted that gold has fallen roughly 15% month to date from its record near $5,500 per ounce hit in January 2026. The metal was trading around $4,450 as of Thursday. Silver has followed an even steeper path lower from its $120 peak. Both are being hit by rising interest rates, a stronger U.S. dollar, and institutional profit-taking after an extended rally.

The ETF flows data is stark. Gold ETFs bled nearly $11 billion in the first three weeks of March. Silver's accumulated inflows from the prior months have been almost entirely reversed. CME futures positioning data - JPMorgan's proxy for institutional sentiment - shows a sharp unwind of long gold and silver exposure from the crowded positions built up through late 2025.

Bitcoin tells a different story. Spot bitcoin ETFs, which launched in the United States in January 2024 and have become the primary institutional vehicle for bitcoin exposure, have continued to attract net inflows over the same period when gold was hemorrhaging. CME bitcoin futures positioning has remained relatively stable. Momentum signals are recovering from oversold conditions toward neutral - suggesting the worst of the selling may be behind it.

"The deterioration in liquidity conditions in gold has seen its market breadth decline below that of bitcoin currently." - JPMorgan analysts led by Nikolaos Panigirtzoglou, research note March 26, 2026

Gold's market breadth falling below bitcoin's is a historically unprecedented statement from a Wall Street bank. Market breadth measures how broadly prices are supported across a market - narrow breadth means only a few assets or participants are keeping prices up, which is typically a warning sign. The fact that bitcoin now has broader market support than gold - even after a significant correction - suggests genuine structural demand rather than speculative froth.

The broader implication for corporate treasuries: the "diversify into hard assets" narrative that drove the gold rush of 2024-2025 is now reversing at pace. If institutional investors are unwinding gold positions to meet redemptions or rebalance portfolios, bitcoin's relative stability could accelerate the shift of the "inflation hedge" and "hard money" narrative toward crypto. That is the secular bull case for bitcoin as a treasury asset - even as individual companies like MARA and GameStop demonstrate that holding BTC at scale requires active management, not just passive accumulation.

The Bigger Picture: What the Fracture Means for Corporate Bitcoin

Corporate boards that rushed to adopt bitcoin treasury strategies in 2024-2025 are now navigating the first real stress test of those policies.

Step back from the individual stories and a pattern emerges. The corporate bitcoin treasury movement - which exploded in 2024 and 2025 as dozens of companies followed MicroStrategy's lead - is encountering its first major macro stress test. Rising yields, geopolitical shocks, and price volatility are forcing companies to confront questions that the original playbook simply assumed away.

The original thesis was simple: buy bitcoin, hold bitcoin, issue cheap debt to buy more bitcoin, watch the asymmetric upside compound forever. It worked spectacularly from 2020 through late 2025. MicroStrategy's Saylor became the high priest of corporate treasury bitcoin. Every CFO panel at every crypto conference in 2024 had at least one speaker explaining why putting 1-5% of cash into BTC was now a fiduciary obligation.

The stress test is revealing the limits of passive conviction. MARA's decision to sell $1.1 billion of coins was rational and value-accretive - but it was also a forced adaptation to balance sheet pressures that the original bull thesis did not adequately price in. GameStop's covered call strategy is either clever treasury optimization or a sign that management has lost conviction and is trying to generate income from a position it does not fully believe in anymore. The covered calls cap upside - you only write them if you think the asset is unlikely to hit those strike prices.

The Sacks departure removes the key political patron of the pro-crypto Washington agenda. The crypto market structure bill - the legislation that could finally give the industry operational clarity on whether tokens are securities or commodities - still has no final form and no obvious champion with equivalent proximity to power. The GENIUS Act stablecoin bill passed the Senate, but the comprehensive framework remains unfinished business.

Kraken's master account fight illustrates the fragility of the institutional access gains made over the past year. A single letter from a senior congresswoman has put a historically significant milestone under legal cloud. If Democrats retake the House in November - a probability that Polymarket currently prices at 84% - Waters returns to the Financial Services Committee chairmanship. That changes the regulatory conversation significantly.

- March 4-25, 2026MARA sells 15,133 BTC for $1.1 billion, retires convertible debt at 9% discount to par

- March 4, 2026Kansas City Fed announces Kraken gets "limited purpose" master account - industry first

- March 26, 2026 (AM)GameStop annual report reveals 4,709 BTC pledged to Coinbase for OTC covered call strategy

- March 26, 2026 (PM)David Sacks announces transition from crypto czar role to PCAST co-chair

- March 26, 2026 (PM)Maxine Waters sends letter to Kansas City Fed demanding Kraken account approval details

- March 26, 2026 (PM)Trump extends Iran energy infrastructure strike pause to 10 days, BTC stabilizes near $69K

- March 27, 2026JPMorgan report: gold market breadth falls below bitcoin's for first time in recorded history

The story of bitcoin as a corporate treasury asset is not ending - the JPMorgan analysis showing bitcoin's relative resilience versus gold is a genuinely bullish data point for the long thesis. Strategy still holds 528,185 BTC and Saylor shows no signs of deviating from his mandate. Bernstein still has a $150,000 year-end target on bitcoin.

But the era of simple, passive accumulation - buy and hold, add leverage, never question the thesis - is being replaced by something more sophisticated and more fragile. Corporate treasury bitcoin is becoming an active management problem. The companies that navigate it well will be the ones that understand the difference between conviction and strategy.

What to Watch Next

Iran deadline: Trump's 10-day pause expires ~April 5. Oil and bond yields remain the dominant macro variable for risk assets.

MARA Q1 2026 earnings: Will the company frame the BTC sale as one-off or the start of a recurring capital allocation policy?

Kraken / Kansas City Fed response: The Fed's written reply to Waters will define the legal standing of every subsequent crypto master account application.

Sacks successor: Who fills the crypto czar vacuum in the White House? The market structure bill needs an advocate with administration access.

GameStop BTC update: Q1 2026 10-Q filing will show whether covered call strategy was renewed post-March expiry or unwound.

Bitcoin ETF flows: Continued net inflows versus gold ETF outflows is the cleanest signal of institutional rotation hypothesis. Watch weekly data.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram