Fink's $150B Bet, Saylor's $42B Reload, and the Law That Rewrites Stablecoins

Bitcoin whipsawed $3,700 in a single session and still held $70K at close. While retail traders were getting liquidated on Trump's Truth Social posts, the institutions were quietly going all-in. Larry Fink dropped a 6,000-word shareholder letter calling tokenization the biggest infrastructure upgrade since the internet. Michael Saylor reloaded $42 billion in buying capacity. And a closed-door Senate meeting just revealed the shape of U.S. stablecoin law - and the crypto industry doesn't love what it saw.

Wall Street is no longer flirting with crypto - it's buying the infrastructure. Photo: Pexels

March 23, 2026 will get remembered as a strange day in crypto. The surface story was chaos - $415 million in leveraged positions wiped out in four hours as Trump posted about pausing Iran strikes and Tehran promptly denied the whole thing (CoinDesk). BTC swung from $67,500 to $71,200 and back to $70,000 inside a single New York session.

But that's the retail story. The institutional story happening in parallel was something else entirely. Three separate developments - each newsworthy on its own - landed within the same 24 hours and together they sketch a blueprint for what crypto actually becomes when the serious money moves in.

BlackRock's CEO invoked the internet. Strategy restocked its war chest. And a new draft of the Digital Asset Market Clarity Act made its Washington debut to a room full of unimpressed lobbyists.

This is what institutional capture looks like at full speed.

Larry Fink Goes All-In: The $150 Billion Tokenization Thesis

Larry Fink's annual letter to shareholders compared tokenization to the internet in 1996. Photo: Pexels

BlackRock CEO Larry Fink has been gradually shifting his language on digital assets for years. The 2024 Bitcoin ETF approval helped. The 2025 GENIUS Act stablecoin law helped more. But his 2026 annual shareholder letter - published in full Monday - is a different category of statement altogether (BlackRock).

Fink didn't just endorse tokenization. He positioned it as the structural fix to inequality, inefficient capital markets, and a financial system that - in his own words - is "working, just not for enough people." That framing matters. It's no longer a product pitch from an asset manager who wants to charge fees on a Bitcoin ETF. It's a thesis about what the entire architecture of ownership should look like in twenty years.

"Half the world's population carries a digital wallet on their phone. Imagine if that same digital wallet could also let you invest in a broad mix of companies for the long term - as easily as sending a payment." - Larry Fink, BlackRock Annual Letter 2026

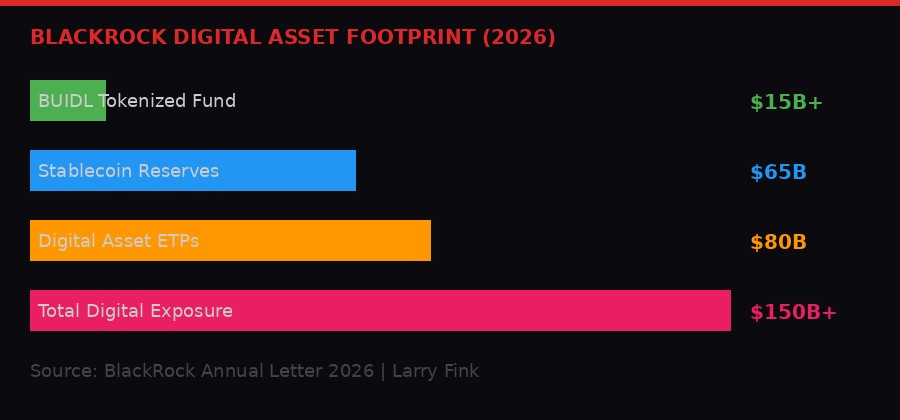

The mechanics Fink described aren't futuristic. They're already operational - just at small scale. BlackRock's BUIDL fund, the USD Institutional Digital Liquidity Fund, is already the world's largest tokenized money market fund. The firm manages $65 billion in stablecoin reserves and nearly $80 billion in digital asset exchange-traded products. Combined, that's roughly $150 billion in assets tied to the digital economy.

BlackRock's digital asset exposure across tokenized funds, stablecoin reserves, and ETPs now totals more than $150 billion. Source: BlackRock Annual Letter 2026.

The comparison Fink used - tokenization is to 2026 what the internet was to 1996 - is doing a lot of work. In 1996, the internet had commercial infrastructure, a growing user base, and obvious utility. But most of the money hadn't moved yet. Businesses still sent physical mail. Securities still settled in days. The transformation took another decade to fully materialize.

Fink's argument is that tokenization is at that exact inflection point. The rails exist. BUIDL proves they work. What's missing is regulatory clarity and distribution infrastructure. If regulators deliver the former, BlackRock will help build the latter.

He called for "clear buyer protections, counterparty-risk standards and digital identity checks" - the language of a man who runs the world's largest asset manager and wants rules he can build products around, not rules that block him.

The letter also touched on Social Security reform, suggesting that long-term market-linked returns could help stabilize the program. That's a secondary story, but it signals how broadly Fink is thinking about financial infrastructure. Digital assets aren't a vertical for BlackRock anymore. They're a foundation.

Strategy's $42 Billion Reload: Saylor Doubles the War Chest

Strategy now holds 762,099 BTC and has restocked buying capacity to $42 billion via new ATM programs. Photo: Pexels

The same Monday that Fink published his letter, Michael Saylor's Strategy (MSTR) quietly filed an 8-K that restocked the company's entire capital-raising arsenal - and then some (SEC Filing).

The new at-the-market program totals $42 billion: $21 billion in Class A common stock (MSTR) and $21 billion in the Variable Rate Series A Perpetual Stretch Preferred Stock (STRC). On top of that, a new $2.1 billion ATM for the STRK preferred series, replacing a prior program.

STRATEGY CAPITAL PROGRAM - MARCH 23, 2026

- New ATM - MSTR common stock: $21B

- New ATM - STRC preferred: $21B

- New ATM - STRK preferred: $2.1B

- Existing MSTR capacity remaining: $6.24B

- Existing STRC capacity remaining: $1.98B

- Existing STRK capacity remaining: $20.33B

- Total potential buying power: ~$52B

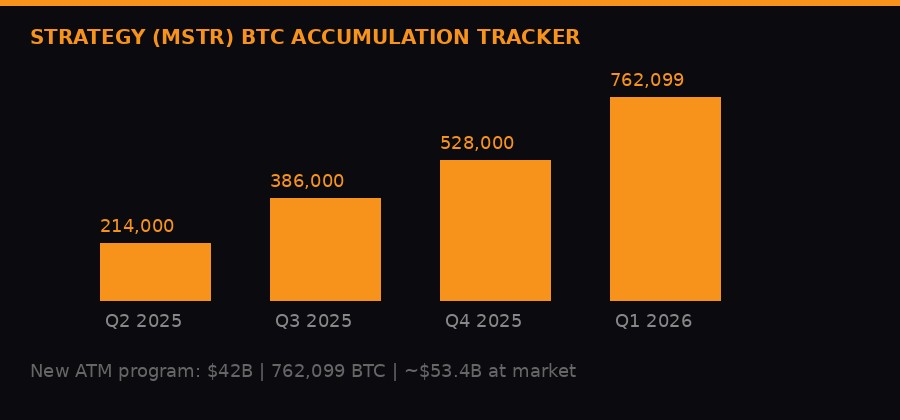

- Current BTC holdings: 762,099 coins (~$53.4B at $70K)

The company added three new sales agents to its syndicate - Moelis & Company, A.G.P./Alliance Global Partners, and StoneX Financial - bringing the total to 19 firms authorized to sell MSTR shares into the market over time. That distribution network is how Saylor converts the stock market's appetite for Bitcoin exposure into actual BTC sitting on a corporate balance sheet.

Strategy has accumulated 762,099 BTC since beginning its accumulation strategy. The new $42B ATM program resets buying capacity for the next phase. Source: MSTR 8-K Filing, CoinDesk.

The timing is deliberate. Last week Strategy purchased another 1,031 bitcoin for $76.6 million - what Saylor called a "small" buy at his scale. MSTR shares were modestly higher Monday as BTC traded near $71,000.

The ATM structure deserves a technical explanation because it's central to why this machine keeps running. Strategy doesn't issue bonds and go buy BTC. It sells shares gradually into the open market through its 19 broker-dealer partners, collecting proceeds that it then deploys into Bitcoin. The preferred shares (STRC, STRK) work similarly but carry fixed or variable dividends, appealing to yield-oriented institutional buyers who want BTC exposure with income characteristics.

The net result is that Strategy acts as a permanent, publicly-listed buyer of Bitcoin. As long as its stock trades at a premium to its BTC net asset value - which it has, persistently - it can issue new equity at attractive terms and buy more BTC, which appreciates the NAV, which sustains the premium. The model is self-reinforcing until it isn't.

At 762,099 BTC, Strategy holds approximately 3.6% of Bitcoin's total 21 million coin supply. The next corporate buyer of scale is H100 Group, which announced Monday it was pursuing acquisitions that would bring it to 3,500 BTC, targeting the title of Europe's largest Bitcoin treasury (CoinDesk). H100's 3,500 vs. Saylor's 762,099 tells you everything about the concentration at the top.

Tom Lee's Bitmine added $138 million in ETH purchases last week - three consecutive weeks of buying through mounting unrealized losses - as its treasury play on Ethereum continues to absorb market supply. Strategy-style treasury plays have officially extended beyond Bitcoin.

The Clarity Act Stablecoin Fight: Banks Win Round One

A closed-door review of the Digital Asset Market Clarity Act gave the crypto industry its first look at revised stablecoin yield language - and insiders say it's too narrow. Photo: Pexels

While Bitcoin was bouncing off Iran headlines and institutions were filing paperwork, a different battle was playing out in a conference room on Capitol Hill. The crypto industry got its first look Monday at revised language in the Digital Asset Market Clarity Act - specifically the section dealing with whether stablecoins can pay yield (CoinDesk).

The opening impression from industry insiders: the language is overly narrow and mechanically unclear.

Here's the background. The GENIUS Act, which became U.S. law in 2025, covered stablecoin issuance basics. The Clarity Act is supposed to be the larger follow-up - comprehensive market structure legislation that would eliminate regulatory ambiguity across the entire digital asset industry. For months, the key sticking point has been whether stablecoin holders can earn yield on their holdings.

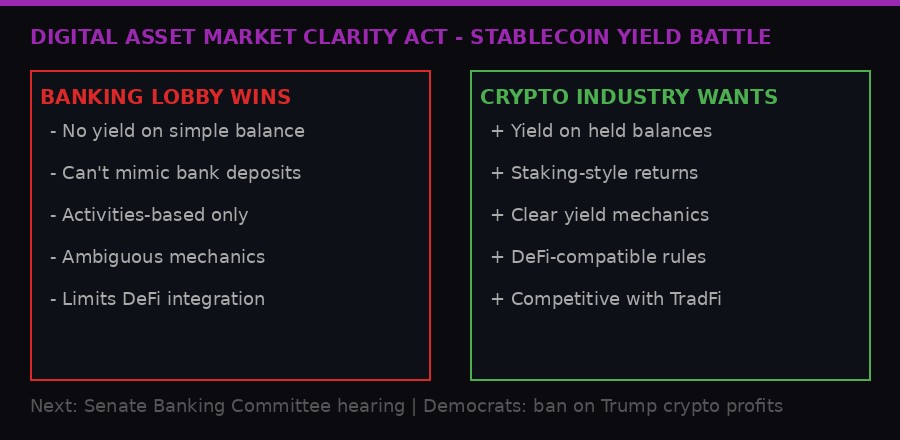

The revised Clarity Act language bars yield on balances but allows activities-based rewards - a compromise neither banks nor crypto fully endorses. Source: CoinDesk reporting.

The banking lobby's position is simple: if stablecoins pay yield, they compete directly with bank deposits, and banks will lose customers. That would constrain lending capacity and potentially destabilize the traditional deposit model that underpins the entire banking system. Their ask was blunt - no yield on balances, period.

The compromise brokered by Senators Angela Alsobrooks and Thom Tillis tries to thread the needle. Per the revised language, stablecoin issuers cannot pay rewards simply for holding a balance. They cannot structure any program that makes the stablecoin functionally equivalent to a bank deposit. But they can pay rewards tied to specific user activities.

"The mechanics of determining activities-based stablecoin rewards is left uncertain." - Person familiar with the current draft, via CoinDesk

That ambiguity is the problem. "Activities-based" is a term that sounds concrete but isn't. Does it mean trading activity? Lending activity? Protocol participation? Providing liquidity? The current text, per sources present at the closed-door review, doesn't specify - which means the crypto industry faces exactly the kind of regulatory gray area the Clarity Act was supposed to eliminate.

The stablecoin yield fight is not the only unresolved issue. The Clarity Act still needs to address DeFi oversight - a priority for Senate Democrats who want anti-money-laundering protections built in - and a provision blocking senior government officials from personally profiting from the crypto industry. That last clause is widely understood to be aimed at Donald Trump, whose family launched multiple crypto ventures before and after his return to the White House.

The bill's trajectory: the closed-door review Monday represents an attempt to clear a path to a Senate Banking Committee hearing, which would be the last major procedural hurdle before floor consideration. A similar version passed the House last year. The Senate Agriculture Committee cleared a markup earlier. The Banking Committee is the final gate.

The Bitcoin Rollercoaster: How One Trump Post Wiped $415 Million

Bitcoin's Iran-driven session Monday was textbook whipsaw - $415 million in leveraged positions hit in under four hours as conflicting headlines landed minutes apart. Photo: Pexels

The $415 million liquidation event deserves its own section because of what it reveals about market structure - not just what happened, but why the damage was so severe for what amounted to a modest net price move (CoinDesk).

BTC started the day around $67,500 after a weekend selloff. The catalyst for that selloff was Trump threatening on Saturday to "obliterate" Iran's power plants unless the Strait of Hormuz was reopened within 48 hours. Markets went risk-off. BTC fell, oil rallied, gold moved.

Then at around 11:23 AM UTC Monday, Trump posted on Truth Social that the U.S. and Iran had held "very good and productive conversations regarding a complete and total resolution of our hostilities." A five-day pause on strikes.

Bitcoin moved $3,700 in roughly one hour on conflicting Iran headlines. The chart of the day for March 23, 2026. Source: CoinDesk, CoinGlass.

BTC ripped from $67,500 to above $71,200 in roughly 60 minutes. Shorts got squeezed. WTI crude dropped 11% to below $88. Brent fell 8% to around $100. The S&P 500 and Nasdaq were up 1.2%. Everything read risk-on.

Then Iran's semi-official Fars news agency reported that no communication had taken place. "There is no direct or indirect communication with Trump," a source told Fars. Bitcoin gave back $1,200 in minutes. Longs who had chased the move got caught. The net settle was about $70,000, up 2.3% on the day.

The liquidation math from CoinGlass is instructive: $280 million in shorts liquidated, $135 million in longs. The 2-to-1 ratio confirms markets were positioned bearishly into the weekend - expecting escalation, not de-escalation - when Trump's post hit. The mass short squeeze was violent. Then the Iran denial clawed back some of those gains and caught the late longs.

The Hyperliquid angle adds another layer. The XYZ:BRENTOIL contract saw $64.4 million wiped, with $61.69 million from longs and just $717,000 from shorts. Traders had been betting the oil price would spike on actual military strikes. They were directionally correct about the situation - strikes were coming - but wrong about the specific Trump social media post that moved markets first.

MARCH 23 LIQUIDATION BREAKDOWN (4-HOUR WINDOW)

- Total liquidations: $415 million

- Short liquidations: $280 million (67%)

- Long liquidations: $135 million (33%)

- Bitcoin: $140M | Ethereum: $120M | Brent (Hyperliquid): $64.4M

- Tokenized gold: $20.9M | Tokenized silver: $19.8M

- BTC net move: +2.3% ($67,500 to ~$70,000)

Wintermute's OTC trader Jasper de Maere framed the forward view cleanly: if the five-day pause holds and Hormuz shipping normalizes, rate-cut expectations could return and BTC could retest the $74,000-$76,000 range. If talks collapse and oil spikes again, mid-$60s. The next five days are binary.

Backpack's BP Token: The FTX Survivors Write a Different Playbook

Backpack Exchange, founded by ex-FTX and Alameda employees, launched its BP token Monday with no founder or investor allocation at inception. Photo: Pexels

While the macro noise dominated headlines, Backpack Exchange launched its native BP token Monday - and the tokenomics are worth reading as a document about how the post-FTX generation of crypto founders is trying to design around the sins of their predecessors (CoinDesk).

Backpack was founded by former FTX and Alameda Research employees. The company carries that history everywhere it goes. After FTX collapsed in November 2022, Backpack quietly acquired the defunct exchange's European licensed entity and relaunched it as Backpack EU, giving itself a regulatory-grade entity to operate from. That acquisition bought credibility and compliance infrastructure simultaneously.

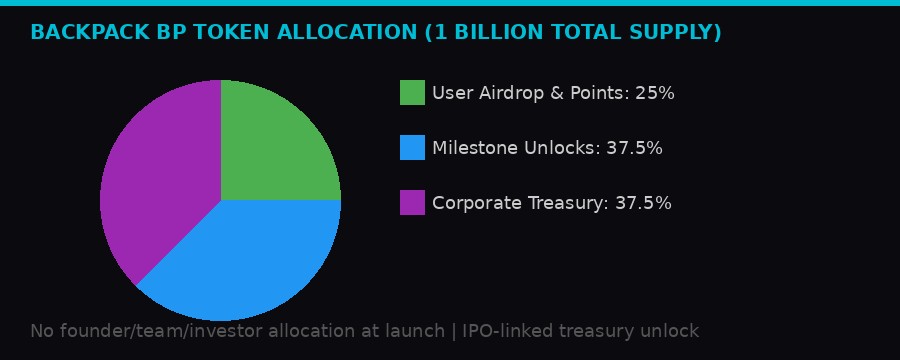

BP token's 1 billion supply: 25% user airdrop at launch, 37.5% milestone unlocks, 37.5% corporate treasury locked until IPO. No insider allocation. Source: Backpack Exchange announcement.

The BP token structure is explicitly designed to avoid the insider dump narrative. Of the 1 billion total supply, 25% (250 million tokens) distributes at launch - primarily to existing users via Backpack's points program, with a smaller slice for Mad Lads NFT holders. No tokens allocated to founders, team members, or early investors at inception.

The remaining 75% splits into two buckets. The first 37.5% unlocks progressively based on operational milestones - market expansion, product launches, regulatory achievements. The second 37.5% stays locked in a corporate treasury until after a potential IPO.

That IPO linkage is novel. Backpack says long-term stakers may eventually convert BP tokens into company equity. The token isn't just a trading or governance instrument. It's potentially a fractional ownership claim on the underlying business.

That framing - exchange token as proto-equity - positions BP directly alongside regulated securities. It's a design choice that either gets challenged by securities regulators as an unregistered offering or becomes a template for how exchange tokens work in a post-Clarity Act world.

Brazil's Crypto Tax Retreat and the Global Regulatory Patchwork

Brazil's finance minister delayed a crypto foreign exchange tax plan, citing election-year political risk. The proposal would have applied rates up to 3.5% on stablecoin transactions. Photo: Pexels

As U.S. legislators worked on the Clarity Act, Brazil's finance minister delayed a separate and contentious crypto tax proposal Monday, citing concerns about conflict with Congress during an election year (CoinDesk).

The Brazilian proposal would classify certain crypto transactions as foreign exchange operations - which in Brazil carries FX tax rates of up to 3.5%. Industry groups argued the classification was both legally incorrect and economically harmful, particularly for stablecoin usage in a country where dollar-denominated stablecoins have become mainstream for cross-border commerce and inflation hedging.

Brazil is the largest crypto market in Latin America and consistently ranks in the top ten globally by volume. Stablecoins, particularly USDT and USDC, are actively used for everyday economic activity in ways that have no direct equivalent in developed markets. Applying a 3.5% FX tax to transactions treated as currency substitutes would hit ordinary users, not just traders.

The delay doesn't kill the proposal. It shelves it past election season. The underlying issue - Brazil's government wants tax revenue from crypto activity - hasn't gone away. But the political calculus has shifted. The finance minister calculated the risk of alienating a vocal, organized crypto constituency outweighs the near-term revenue benefit.

The Brazil situation illustrates the fracture lines in global crypto regulation. The U.S. is moving toward a comprehensive framework that tries to normalize digital assets inside existing financial law. The European Union's MiCA is already live. But in emerging markets, governments are still deciding whether crypto is a foreign currency, a commodity, a security, or a new category entirely - and each answer has massive tax and regulatory implications.

What Comes Next: The Five-Day Clock and the Institutional Ratchet

Bitcoin's near-term price path runs through the Iran situation. The institutional buildout continues regardless of outcome. Photo: Pexels

The five-day pause Trump announced expires Saturday. Between now and then, every development in Iran-U.S. relations is a direct input into crypto prices. That's the uncomfortable reality of a market that has become correlated with geopolitical risk in ways that didn't exist three years ago.

If talks progress and oil normalizes, the macro ceiling for crypto lifts. BTC has multiple times stalled at $74,000-$76,000 - a range that represents both technical resistance and the inflation/rate-sensitivity ceiling the market has been unable to break through while energy prices remain elevated. Oil at $88 WTI, down from $110+ at the conflict's peak, is moving in the right direction. Hormuz staying open is the variable.

The options market is still hedged bearish. Put options on Deribit traded at an 8-10 volatility point premium to calls through June-end expiry as of Monday close, per Amberdata data cited by CoinDesk. Traders are treating the bounce with skepticism. That positioning - if the pause holds and good-faith talks emerge - is a coiled short squeeze waiting to happen.

On the institutional side, there's no pause button. Fink's letter, Saylor's 8-K filing, and the Clarity Act's progress through Senate committees are all slow-moving but directional forces. They operate on quarterly and annual timescales, not on five-day ceasefire windows.

BlackRock now has $150 billion in digital asset exposure. That number was zero in 2020. The direction of travel is not in question - only the speed. The BUIDL tokenized fund has demonstrated that institutional-grade on-chain money market products work at scale. The ETF business has demonstrated that mainstream investors will buy regulated Bitcoin exposure. The Clarity Act, once passed, unlocks the next tier: DeFi products, tokenized securities, stablecoin yield products, all inside a U.S. legal framework.

Strategy's $42 billion ATM reload ensures there is a permanent institutional buyer in the market regardless of retail sentiment. At 762,099 BTC, Saylor has converted approximately $53 billion in corporate capital into Bitcoin. The next 1,000 BTC will come from the new ATM program. So will the 1,000 after that.

The stablecoin Clarity Act fight will resolve - badly or well for the crypto side, but it will resolve. The banking lobby won the first draft. But the crypto industry has competent lobbyists, a compliant president, and a Senate majority that voted for GENIUS last year. The final text will look different from Monday's closed-door preview.

Bitcoin at $70,000 is a strange place to be. It's well off its all-time highs. It's been range-bound for weeks. It moves $3,700 on a single presidential social media post and gives half of it back when a foreign government denies the post happened. That's not the behavior of an asset class that has figured out what it is.

But Fink's letter, Saylor's 8-K, and the Senate markup tell a parallel story. The infrastructure is being built. The capital is being allocated. The laws are being written. What crypto is becoming - at the institutional layer - looks nothing like what it was five years ago. The retail whipsaw is the visible surface. The structural transformation is what's happening underneath.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram