The Chip Uprising: How China Built an AI Silicon Empire While Washington Watched

IDC data reveals Chinese chipmakers captured 41% of the domestic AI accelerator market in 2025 - delivering 1.65 million GPUs while Nvidia's dominance cratered from near-monopoly to a bare majority. The sanctions playbook didn't just fail. It created a competitor.

The silicon battlefield: China's domestic chipmakers are rewriting the rules of AI hardware competition. Photo: Pexels

Three years ago, the question was whether China could survive without Nvidia. Today, the question is whether Nvidia can survive without China.

New data from research firm IDC, reported by Reuters on April 1, tells a story that Washington's export control architects never imagined writing. Chinese GPU and AI chip makers captured approximately 41% of China's AI accelerator server market in 2025, up from what analysts estimate was roughly 5-10% just three years earlier. They shipped a combined 1.65 million AI GPUs into a market that is now the world's second-largest consumer of artificial intelligence compute.

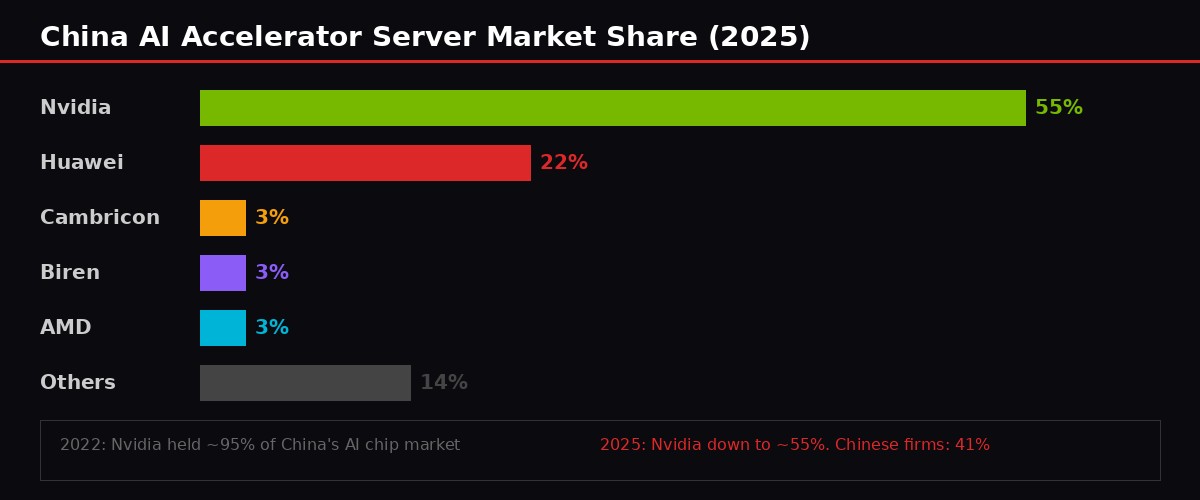

Nvidia still leads. It shipped around 2.2 million cards and held a 55% share in 2025. But that number used to be north of 95%. In the span of three fiscal years, the company lost nearly 40 percentage points of market share in what was once its most profitable international market. Not because it made worse chips - because Washington made policy decisions that turned the Chinese semiconductor ecosystem from a captive buyer into a survival-driven innovator.

The total market tells its own story: approximately 4 million AI accelerator cards shipped into China in 2025. That figure itself has exploded, driven by Beijing's all-hands push to build AI data center capacity. And an increasing share of those cards carry logos that didn't exist on any benchmark five years ago.

The Numbers Behind the Earthquake

Data compiled from IDC, Reuters, and Tom's Hardware reporting. BLACKWIRE infographic.

Let's break the IDC data down because the headline number - 41% - obscures the texture of what's actually happening inside China's AI silicon ecosystem.

Nvidia remains the single largest vendor by unit volume. Its approximately 2.2 million card shipments dwarf any individual Chinese competitor. But the aggregate matters more than any single player. Huawei's HiSilicon division - the maker of the Ascend series of AI accelerators - is now firmly the second-largest AI chip supplier in China. Though IDC didn't break out individual Chinese company shares, industry analysts at Tom's Hardware and Digitimes estimate Huawei accounted for the largest slice of that 41%, followed by a cluster of startups-turned-scaleups.

AMD sits just outside the top tier. Cambricon Technologies and Biren Technology round out the top five, each delivering approximately 116,000 AI accelerator cards in 2025, according to Tom's Hardware's analysis of the IDC data. That's not a vanity number. That's real silicon going into real data centers training and running real models.

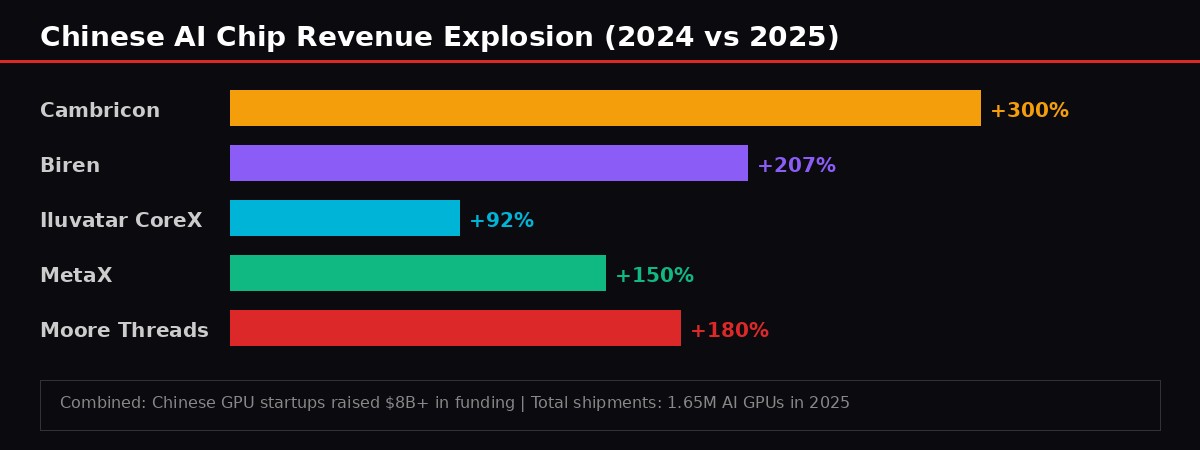

The revenue picture is even more striking. Biren Technology, which only went public in January 2026, posted full-year 2025 revenue of 1.03 billion yuan (approximately $149 million), representing a 207.2% year-over-year surge. Its crosstown rival Iluvatar CoreX posted identical top-line revenue of 1.03 billion yuan, a 91.6% increase. Cambricon Technologies - the oldest and most established of China's domestic AI chip pure-plays - saw revenue growth exceeding 300% in 2025, though from a small base, according to South China Morning Post reporting.

These aren't profitable companies yet. Biren posted losses of 16.5 billion yuan. Iluvatar CoreX lost 1 billion yuan. But the trajectory matters more than the current P&L. These firms are in land-grab mode, and Beijing is bankrolling the land.

Huawei: The Anchor of the Domestic Stack

Huawei's Ascend chips are becoming the default AI accelerator for Chinese data centers. Photo: Pexels

If there's a single company that embodies the chip uprising, it's Huawei. The Ascend 910C - the company's current flagship AI accelerator - delivers approximately 60% of the inference performance of Nvidia's H100, according to The Asia Business Daily, citing benchmark analysis. In pure compute terms, you need roughly 1.5 to 2 Huawei chips to match a single Nvidia GPU. On paper, that sounds like a loss.

In practice, it's a revolution.

Because the Ascend 910C works. It trains models. It runs inference. It plugs into China's domestic software ecosystem with a compatibility layer that has been iterated on relentlessly since 2023. And critically, it does all of this without a single component that requires a U.S. export license.

Reuters reported on March 27 that Huawei's newest AI chip - the Ascend 920, unveiled at the company's Developer Conference - has already attracted purchase orders from ByteDance and Alibaba. The 920 reportedly offers modest improvements in raw compute over the 910C but is specifically designed to excel at inference workloads, the process of running trained AI models to handle real-time queries and tasks. This is a strategically shrewd move. Training is the glamorous headline, but inference is where the volume lives. Every ChatGPT-style query, every AI-powered search result, every recommendation engine tick requires inference. Huawei is positioning itself for the workload that actually generates revenue.

The software story reinforces the hardware gains. Zhipu AI's GLM-5 model - a 744 billion parameter frontier system - was trained entirely on Huawei Ascend 910B chips. Zero Nvidia involvement. It scored 92.7% on AIME 2026, a competitive mathematics benchmark, and while it trails GPT-5.2 and Claude on certain academic benchmarks, the gap is measured in single-digit percentage points, not orders of magnitude. DeepSeek, perhaps the most talked-about Chinese AI lab of 2025-2026, has adopted a hybrid strategy: Nvidia chips for training, Huawei chips for inference deployment. Reports indicate DeepSeek V4 - the upcoming trillion-parameter multimodal model - is being specifically optimized for Ascend hardware.

There were failures along the way. An OSINT analysis circulating on Reddit documented that DeepSeek's R2 model "failed on Ascend 910B training," forcing a reversion to Nvidia H20 chips. The Ascend stack is not yet a drop-in replacement for the CUDA ecosystem that has defined AI compute for a decade. But Huawei is closing the gap with each generation, and the fact that China's most capable AI labs are building Ascend-native workflows speaks louder than any individual benchmark.

The Startup Surge: Biren, Cambricon, and the New Silicon Pack

China's AI chip ecosystem has expanded from one credible player (Huawei) to a full stack of competitors. BLACKWIRE infographic.

Huawei gets the headlines, but the deeper story is the ecosystem forming around it. A cluster of Chinese chipmakers - most founded between 2018 and 2020, many by engineers who trained at Nvidia, AMD, or Qualcomm's China operations - have collectively transformed from venture-funded prototypes into shipping silicon vendors.

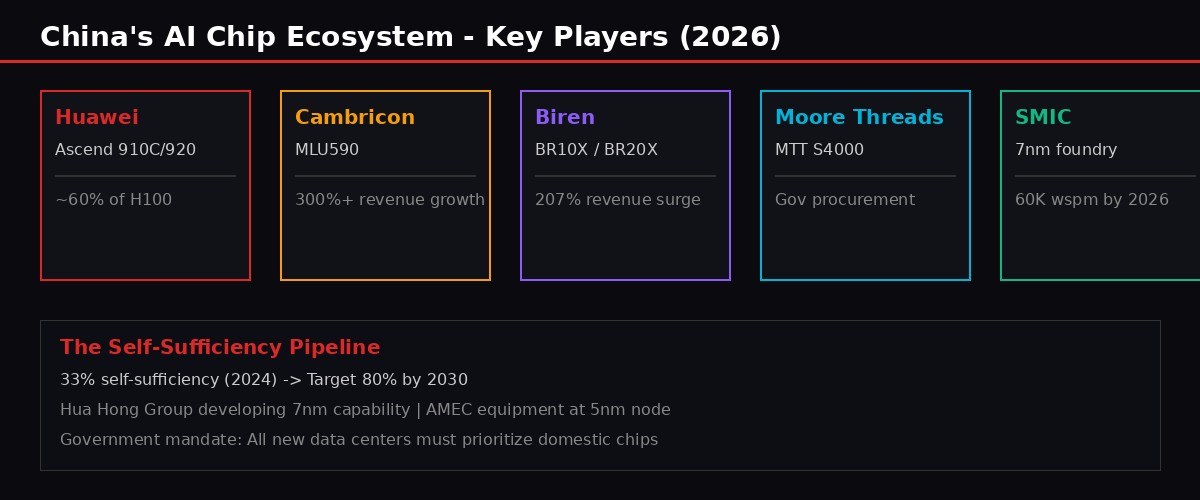

Biren Technology is the most dramatic turnaround. Founded in 2019, it nearly collapsed in 2022 when the U.S. Commerce Department's entity list designation threatened to cut off access to TSMC's advanced nodes for manufacturing. The company pivoted to domestic foundries and redesigned its architecture around available process technology. Its BR10X general-purpose GPU became the main revenue contributor in 2025, and the next-generation BR20X - built on a more advanced architecture - is slated for launch in 2026. Biren's stock has surged since its January 2026 IPO despite the massive losses, a signal that investors see the government procurement pipeline as a guaranteed floor.

Cambricon Technologies is the elder statesman of the group. Founded in 2016 by two brothers from the Chinese Academy of Sciences, it was the first Chinese company to ship a commercial neural network processor. Its MLU590 series is deployed across Baidu, Tencent, and government-funded computing centers. Revenue growth north of 300% in 2025 reflects the government's procurement mandate hitting full stride.

Moore Threads, founded by a former Nvidia China executive, has taken a different angle - targeting both AI and graphics workloads with its MTT S4000 series. The company has won contracts for government digital infrastructure projects where having a domestic supplier is not a preference but a requirement.

MetaX Integrated Circuits and Enflame round out the field, with both companies reporting stellar 2025 results driven by the same procurement tailwinds. Collectively, Chinese AI chip startups raised over $8 billion in funding through 2025, according to analysis by tech-insider.org.

Revenue growth across China's domestic AI chip sector in 2025. All figures represent year-over-year increases. BLACKWIRE infographic.

The pattern is consistent across all of these firms: triple-digit revenue growth, persistent losses, massive government backing, and a clear path to scale that doesn't depend on any single foreign technology supplier. This is not an accident. It's industrial policy working exactly as designed.

The Sanctions Paradox: How Export Controls Created the Thing They Were Meant to Prevent

Data center buildout in China has accelerated precisely because of supply chain uncertainty. Photo: Pexels

The U.S. chip export control regime began in earnest in October 2022, when the Commerce Department's Bureau of Industry and Security (BIS) issued sweeping restrictions on advanced semiconductor exports to China. The logic was straightforward: deny China access to cutting-edge AI hardware, and you deny it the compute necessary to train frontier AI models that could be applied to military or surveillance purposes.

The policy has gone through multiple iterations since then. Each round tightened restrictions, then loosened them, then tightened again in a whiplash cycle that confused the industry as much as it constrained it. The most telling policy shift came in January 2026, when the Commerce Department changed the licensing framework for Nvidia's H200 chip - its second-most-powerful AI accelerator - from "presumption of denial" to "case-by-case licensing." The East Asia Forum described this as evidence that export controls have "cooled down" under practical pressure.

Then came the reversal of the reversal. In March 2026, Nvidia halted production of H200 chips intended for the Chinese market entirely, shifting TSMC manufacturing capacity to its next-generation Vera Rubin architecture instead, as reported by the Financial Times. The same month, U.S. senators called for a full suspension of Nvidia's export licenses to China after the Super Micro smuggling scandal revealed that sanctioned chips were reaching Chinese military-linked universities through intermediary networks.

The zigzag had a predictable effect. Chinese buyers, unable to rely on stable access to Nvidia silicon, made the rational decision to invest in domestic alternatives - even when those alternatives were objectively worse. A chip that's 60% as fast as an H100 but available on a 12-month guaranteed delivery schedule beats a chip that's 100% as fast but might get sanctioned mid-order.

"The export controls didn't stop China from building AI compute. They changed who China buys it from." - Analysis, East Asia Forum, March 2026

The numbers make this vividly clear. The total AI accelerator market in China grew substantially even as Nvidia's share shrank. Chinese data centers didn't build fewer servers - they built more, and they filled them with domestic silicon. The policy created exactly the market conditions that domestic chipmakers needed to achieve escape velocity: guaranteed demand, government subsidies, and the elimination of the most formidable competitor's ability to compete on price and availability.

The 80% Ambition: China's Five-Year Plan for Silicon Independence

Beijing's five-year plan makes semiconductors a strategic priority equal to national defense. Photo: Pexels

The 41% market share number is not the end state. It's the launchpad.

On March 31, TrendForce reported that 13 leading Chinese semiconductor executives have proposed a five-year roadmap targeting 80% chip self-sufficiency by 2030. This target, embedded within China's 2026-2030 Five-Year Plan, covers the entire semiconductor supply chain - not just AI accelerators but foundry capacity, manufacturing equipment, packaging, and design tools.

The current self-sufficiency rate, measured by the share of domestic supply provided by Chinese companies, stood at approximately 33% in 2024, according to Nikkei's analysis. Getting from 33% to 80% in six years would require the kind of industrial mobilization not seen since China's high-speed rail buildout of the 2010s. Beijing appears to believe the geopolitical environment leaves no alternative.

The plan's specific targets are ambitious bordering on aggressive:

- Build and test production lines using fully domestic equipment for 7nm chips. Currently, only SMIC has demonstrated 7nm capability, and it relies on older DUV lithography rather than ASML's EUV machines. Hua Hong Group, China's second-largest foundry, is now developing 7nm process technology, as Reuters reported on March 16 in an exclusive.

- Achieve stable production at 14nm using domestic equipment. This is more realistic and already underway at SMIC's Shanghai and Beijing fabs.

- Grow mature-node manufacturing capacity from 25% of global share in 2024 to 42% by 2028. SEMI China's president Lily Feng confirmed this projection at Semicon China 2026.

- Develop "atomic level packaging" with sub-0.2nm surface roughness. JCET Group's CEO Zheng Li described this as the post-Moore's Law frontier, where performance gains come from packaging innovation rather than transistor shrinkage.

On the equipment side, AMEC - China's leading semiconductor equipment manufacturer - unveiled tools for logic chips at the 5nm node and below at Semicon China 2026. AMEC chairman Gerald Yin stated the company plans to increase its in-house supply of high-performance products to over 60% within five to ten years. Naura, the country's largest chip equipment maker, expanded its product lineup following its 2025 acquisition of Kingsemi, introducing tools incorporating nanometer-level technologies.

The gap remains significant. Photolithography is the bottleneck. Without access to ASML's EUV machines, Chinese foundries are performing what amounts to semiconductor surgery with a butter knife - using multiple DUV patterning passes to achieve feature sizes that EUV can hit in one shot. It works, but it's slower, more expensive, and lower-yield. SMIC's 7nm process using DUV achieves roughly 45,000-60,000 wafer starts per month, compared to TSMC's EUV-based 3nm and 5nm lines that run at multiples of that volume.

But "good enough" is a powerful concept in industrial competition. China doesn't need to match TSMC nanometer-for-nanometer. It needs to build enough domestic capacity to train and run AI models at competitive cost. The 41% market share number suggests it's already doing that at the chip level. The question is whether the foundry and equipment layers can follow.

The Geopolitical Chessboard: What the Data Means for the AI Race

The semiconductor supply chain is now a primary vector of geopolitical competition. Photo: Pexels

There are three second-order consequences of this shift that most analysis overlooks.

First: Nvidia's China revenue is not coming back. The company's China revenue peaked in fiscal 2023 and has been declining as a percentage of total revenue ever since. Even if export controls were lifted tomorrow - which they won't be - Chinese buyers have already invested billions in Huawei and Cambricon-based infrastructure. Switching costs are real. Software ecosystems have been rewritten for CANN (Huawei's compute architecture) instead of CUDA. The window for Nvidia to recapture China closed sometime in 2024, and the IDC data just confirmed what the market already knew. Jensen Huang's lobbying for looser export controls was never about regaining share - it was about slowing the bleeding.

Second: The Chinese AI software stack is diverging from the Western stack. When DeepSeek optimizes for Ascend hardware, when Zhipu trains GLM-5 on Huawei chips, when Baidu deploys inference on Cambricon MLU590s - they're building an entirely separate computational infrastructure. This is the real decoupling. Not trade statistics or tariff rates, but two incompatible silicon ecosystems supporting two incompatible AI development pipelines. A researcher trained on one stack will find the other increasingly foreign. Models optimized for one architecture won't transfer cleanly to the other. We're watching the bifurcation of the global AI compute layer in real time.

Third: This reshapes the semiconductor industry's global power dynamics. If Chinese chip firms can build a domestic ecosystem that serves the world's second-largest AI market without Nvidia, AMD, or Intel - and they're demonstrably doing this - then the leverage that U.S. chip companies hold over the global technology order diminishes. China's next move is already visible: the Five-Year Plan explicitly links AI computing infrastructure to "capacity building" for partner nations. Offshore computing facilities built for Belt and Road countries will run on Chinese silicon. The Diplomat reported in March that Washington hasn't noticed this dimension of the plan. By the time it does, the installed base may already be locked in.

U.S. BIS issues sweeping chip export controls targeting China. Nvidia's A100 and H100 banned for export.

Nvidia launches H20 - a China-specific downgraded chip designed to comply with export rules.

Huawei ships Mate 60 Pro with SMIC-fabricated 7nm chip, shocking Western analysts.

DeepSeek releases V3, trained partly on Huawei hardware, challenging frontier Western models.

Commerce Dept shifts H200 export policy to case-by-case licensing. Too late - Chinese buyers have moved on.

Nvidia halts H200 production for China. Senators demand export license suspension. Super Micro smuggling scandal breaks.

Huawei unveils Ascend 920. ByteDance and Alibaba place orders. Hua Hong Group readies 7nm production.

IDC data reveals Chinese chipmakers at 41% market share. The tipping point arrives.

The Manufacturing Backbone: SMIC, Hua Hong, and the Foundry Question

China's foundry capacity is expanding rapidly even without access to EUV lithography. Photo: Pexels

Designing competitive AI chips is only half the battle. You also need somewhere to manufacture them. This is where China's position gets more complicated - and where the export control regime still has real teeth.

SMIC, China's largest foundry, has demonstrated 7nm manufacturing capability using DUV (deep ultraviolet) lithography - a feat that most industry observers considered technically improbable before Huawei's Mate 60 Pro shocked the world in September 2023. SMIC's production capacity at advanced nodes sits at approximately 45,000-60,000 wafer starts per month, expanding toward 60,000 through 2026, according to industry analysis by Oplexa. For context, TSMC's total capacity across all nodes exceeds 2 million wafer starts per month.

The volume gap is enormous. But it's shrinking on a percentage basis, and China is throwing money at the problem. Nexchip, a foundry backed by the Hefei municipal government, filed for a Hong Kong listing in late March to fund a $5.1 billion Phase IV expansion, as reported by The Next Web. SMIC's own action plan, unveiled in March, explicitly calls out AI demand as a structural growth driver and warns that the AI memory cycle is "squeezing" capacity for other chip types.

The most significant foundry development is Reuters' March 16 exclusive that Hua Hong Group - China's second-largest chip foundry, which currently operates at 22nm and 28nm nodes - has developed 7nm process technology. If Hua Hong can achieve production-ready 7nm, China would have two independent foundry sources for the AI chip designs coming out of Huawei, Cambricon, and Biren. That's a redundancy advantage that reduces supply chain risk significantly.

Advanced packaging is emerging as the equalizer. JCET Group CEO Zheng Li told attendees at Semicon China 2026 that the industry is undergoing a "leap" in packaging technologies, with next-generation "atomic level packaging" targeting surface roughness below 0.2nm. In the post-Moore's Law era, where shrinking transistors yields diminishing returns, packaging innovation - stacking chips in three dimensions, connecting them with ultra-fast interconnects, integrating different function blocks into a single package - may matter as much as the lithography node itself. China has world-class packaging capabilities and no export control restrictions on packaging technology.

What Comes Next: The 2026 Inflection Points

The AI silicon landscape is splitting into two spheres of influence - and the boundary lines are being drawn now. Photo: Pexels

Several catalysts in 2026 will determine whether the 41% share was a ceiling or a floor.

Huawei's Ascend 920 shipping timeline. Reuters reported ByteDance and Alibaba are placing orders. If the 920 delivers on its inference optimization promise and ships in volume by mid-2026, Huawei could absorb a significant chunk of the inference compute market that currently runs on Nvidia H20 and older A100 chips. The 910C is already scheduled to begin shipping to customers from May.

Biren's BR20X launch. The next-generation GPU from Biren Technology is slated for 2026 and represents the company's first architecture built from the ground up for AI-native workloads rather than adapted from general-purpose GPU designs. If it performs, Biren joins Huawei as a credible training-capable domestic option.

DeepSeek V4. The anticipated trillion-parameter multimodal model is reportedly being optimized for Huawei Ascend hardware. If DeepSeek ships a frontier-class model trained primarily on domestic silicon, it demolishes the argument that Chinese hardware can't support cutting-edge AI research. The model's release - expected imminently based on technical leaks circulating in Chinese AI research communities - would be a symbolic milestone comparable to Sputnik for the semiconductor industry.

Washington's next move. The Chip Security Act, introduced in the wake of the Super Micro scandal, could impose even stricter controls. But the IDC data creates a powerful counter-argument: the controls have already failed to prevent China from building competitive AI compute. Further restrictions would primarily hurt Nvidia's remaining China revenue without materially degrading Chinese AI capabilities. This is the trap that sanctions architects find themselves in - doubling down on a strategy whose unintended consequences are already visible.

The government procurement mandate. Beijing has reportedly instructed all new government-affiliated data centers to prioritize domestic chips. The Cyberspace Administration of China has requested major corporations to stop purchasing Nvidia H20 chips and buy from domestic suppliers instead. This is where the 41% could become 50%, then 60%, through administrative fiat rather than market competition. When the buyer and the regulator are the same entity, market share shifts can happen at policy speed rather than product-cycle speed.

For Nvidia, the path forward is clear - and it doesn't run through Beijing. Jensen Huang's pivot to the Vera Rubin architecture and aggressive expansion in Middle Eastern, Southeast Asian, and Indian markets reflects an implicit acknowledgment that the China revenue story is over. The company will remain the global AI chip leader for the foreseeable future. But "global leader excluding China" is a different trophy than "global leader including China," and the financial implications for a company trading at 30x forward earnings are significant.

For Washington, the IDC data forces an uncomfortable reckoning. Export controls were designed to maintain a technology gap. Instead, they appear to have compressed the timeline for Chinese self-sufficiency. The 80% target for 2030 looked aspirational when it was announced. After the 41% market share report, it looks aggressive but achievable. The policy didn't fail in the traditional sense - it achieved something. It just wasn't what anyone intended.

The silicon curtain is real, and it's falling. On one side, an NVIDIA-TSMC-ASML axis that still produces the world's most powerful individual chips. On the other, a Huawei-SMIC-Cambricon axis that produces chips that are good enough, available immediately, and backed by the combined purchasing power of a $18 trillion economy with a government that has decided semiconductor independence is an existential national priority.

That second axis just captured 41% of the world's second-largest AI market. And it's accelerating.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram