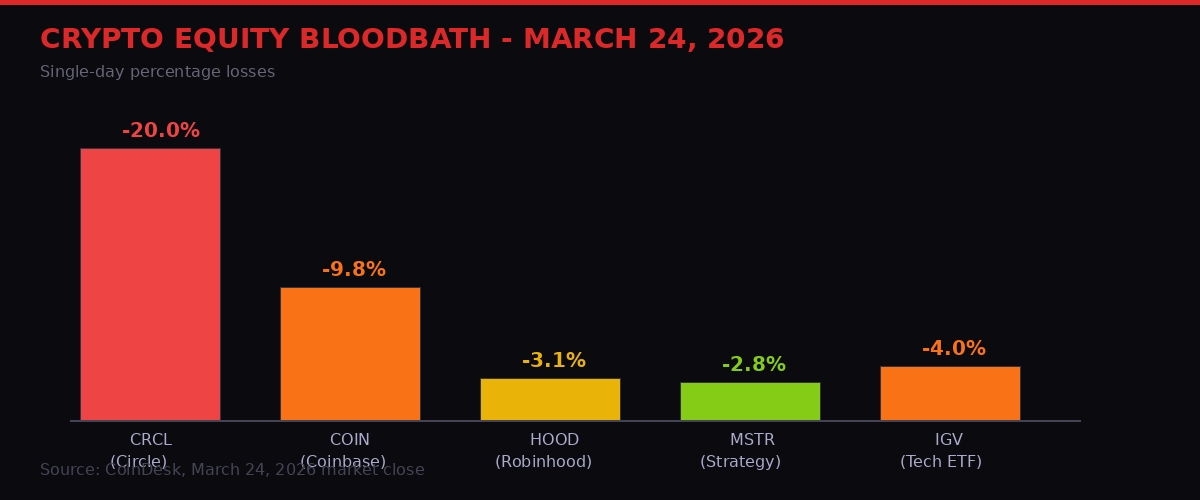

Tuesday, March 24, 2026 will be remembered as the day a Senate draft text - not a hack, not a rug pull, not a Fed decision - blew up one of the most successful crypto IPO stories in years. Circle Internet Group, issuer of the USDC stablecoin, saw its shares crater 20% in a single session. Coinbase, which shares USDC revenue with Circle, dropped nearly 10%. Bitcoin slipped from $71,000 to $69,600 before a late-session geopolitical relief rally pulled it back toward $70,500.

The trigger: a closed-door Capitol Hill review of the Digital Asset Market Clarity Act's latest draft language - which would ban stablecoin issuers from paying yield on passive balances and ban anything "economically equivalent to interest." Industry insiders who saw the text said it was narrower and more restrictive than the market had assumed. The sell-off that followed was immediate and brutal.

This is not a one-day event. It is a structural repricing. Here is what actually happened, what it means for the stablecoin industry, and why the broader backdrop - rate hike bets at a two-year high, oil above $104, Iran back in the headlines - makes this one of the more consequential trading days of 2026.

Market Snapshot - March 24, 2026

Circle's stock had rallied over 170% in six weeks before Tuesday's catastrophic reversal. (Pexels)

What the Clarity Act Actually Says - And Why It Matters

The Digital Asset Market Clarity Act is the "second act" of U.S. crypto legislation - meant to follow the GENIUS Act (which became law governing stablecoin issuers) and establish the full legal framework for digital asset markets. Getting it through the Senate Banking Committee has been a multi-year grind involving turf wars between banking regulators, Senate factions, and the crypto lobby.

The latest sticking point - stablecoin yield - was supposed to be resolved. Senators Angela Alsobrooks (D-MD) and Thom Tillis (R-NC) announced last Friday that they had struck a deal: stablecoin rewards on activities would be allowed, but not on passive balances. That sounded like a workable compromise. The market assumed it was.

Then industry lawyers actually read the draft. [CoinDesk, March 23]

"The language would ban yield payments for simply holding a stablecoin. It would also restrict any approach that makes the program in any way equivalent to a bank deposit... the mechanics of determining activities-based stablecoin rewards is left uncertain." - Person familiar with the Clarity Act draft, via CoinDesk

That uncertainty is the problem. The pass-through model - where Circle earns interest on USDC's Treasury-backed reserves, shares revenue with Coinbase, which in turn funds user rewards - sits in a legal grey zone under the new language. The phrase "economically equivalent to interest" could swallow the entire structure.

"It pulls the rug on the pass-through model that has been driving stablecoin adoption," said Amir Hajian, a digital asset researcher at Keyrock, in comments cited by CoinDesk. [CoinDesk, March 24]

Crypto-linked equity losses on March 24, 2026. Circle led the carnage with a -20% single-session drop. (BLACKWIRE analysis)

Circle's Spectacular Reversal - From 170% Gain to -20% in One Day

Context matters here. Circle went public in early 2026 and had been one of the hottest names in financial markets. From its February lows, CRCL shares gained over 170% - an extraordinary run fueled by surging USDC volumes, the broader crypto rally, and investor enthusiasm for "real-world utility" crypto businesses that generate actual revenue.

Then Tuesday happened. The stock dropped 20% in a single session, snapping six weeks of momentum in one trade. Coinbase (COIN) - which earns roughly 20% of its revenue from its USDC partnership with Circle - fell nearly 10%.

The core of Circle's revenue model is this: USDC is backed primarily by U.S. Treasury bills. Those T-bills earn interest. Circle keeps a portion and shares the rest with Coinbase, which uses it to fund the yields it pays USDC holders on its platform. With short-term rates still elevated - even as rate cut expectations have completely evaporated - this model generates significant cash flow. Coinbase reported hundreds of millions in USDC-related revenue last year alone.

The Clarity Act's new language, if it stands, would not just reduce that revenue - it would structurally alter how stablecoins compete. USDC's ability to offer yield through Coinbase was a core differentiator versus Tether's USDT, which does not offer yield to end users. Kill that, and you narrow the competitive moat significantly.

"That weakens a key part of the bull case by making USDC harder to evolve from a payments utility into a real store-of-value product." - Shay Boloor, Chief Market Strategist, Futurum Equities [X/Twitter]

Mizuho analyst Dan Dolev quantified the concern: a yield ban "could reduce the use case for Circle in the near-term, while not paying rewards would reduce the long-term attractiveness of holding USDC on Coinbase's platform." [CoinDesk, March 24]

Not everyone is panicking. Owen Lau at Clear Street called it "an overreaction - the market tends to shoot first and ask questions later." Ryan Rasmussen at Bitwise noted Circle is still up over 30% year-to-date even after the crash, and said "there will be workarounds" - loyalty programs, for example, that replicate yield incentives without technically paying interest. Circle's 30% share of a stablecoin market projected to grow 10x over four years is not disappearing overnight.

But the psychological damage is done. Investors bought Circle on the yield thesis. That thesis just took a direct hit from Capitol Hill.

Bitcoin Below $70K: The Rate Hike Fear Nobody Wanted to Price In

Bitcoin has fallen as much as 45% from its late-2025 all-time highs as rate expectations reversed sharply. (Pexels)

The Circle crash did not happen in a vacuum. Bitcoin was already struggling. BTC hit $71,000 earlier in the session before sliding toward $69,600 as U.S. stocks opened lower. The move tracked a broader risk-off rotation - the iShares Tech-Software ETF (IGV) dropped 4%, and crypto has been moving closely with software stocks for months. Both have been trending lower since October.

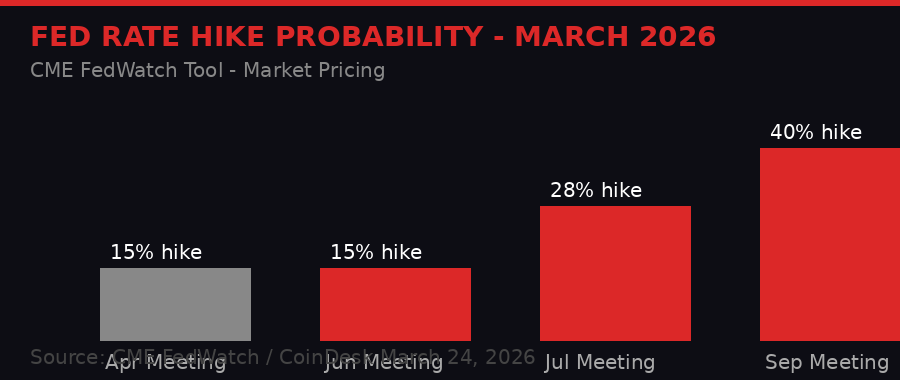

The macro picture is getting genuinely uncomfortable. In what CoinDesk described as "one of the more remarkable 180-degree turnarounds in recent years," markets have gone from debating how many rate cuts the Fed would deliver in 2026 - the consensus was three to four as recently as December - to now pricing a 15% probability of an outright rate hike by June. [CoinDesk, March 24]

According to CME FedWatch data, there is currently zero probability of a cut at either the April or June Federal Reserve meetings. Zero. That is not a minor recalibration - it is a complete narrative reversal in under three months.

CME FedWatch data shows the probability of a June 2026 rate HIKE has risen to 15% - a dramatic reversal from December's unanimous cut expectations. (BLACKWIRE / CME data)

The DXY (dollar index) is holding above 99. Oil spent most of Tuesday above $104 per barrel. Global bond yields are climbing. The traditional formula - tight money, strong dollar, rising real yields - is historically hostile to risk assets, and crypto is very much a risk asset in 2026 institutional portfolios.

There is an added layer of political uncertainty. President Trump nominated Kevin Warsh to replace Jerome Powell as Fed Chair, with the stated rationale of pushing rates lower. But Warsh is a known inflation hawk who was among the first to call for tightening after the 2008 crisis. The market is not sure he would actually cut - especially with inflation data still sticky and the Middle East conflict keeping energy prices elevated.

Bitcoin has fallen roughly 45% from its late-2025 all-time highs. That is a severe correction by any measure. The question is whether $60,000 holds as the next major support, or whether this becomes a deeper structural bear market driven by macro factors outside crypto's control.

Tether Makes Its Move - A Big Four Audit Is a Power Play

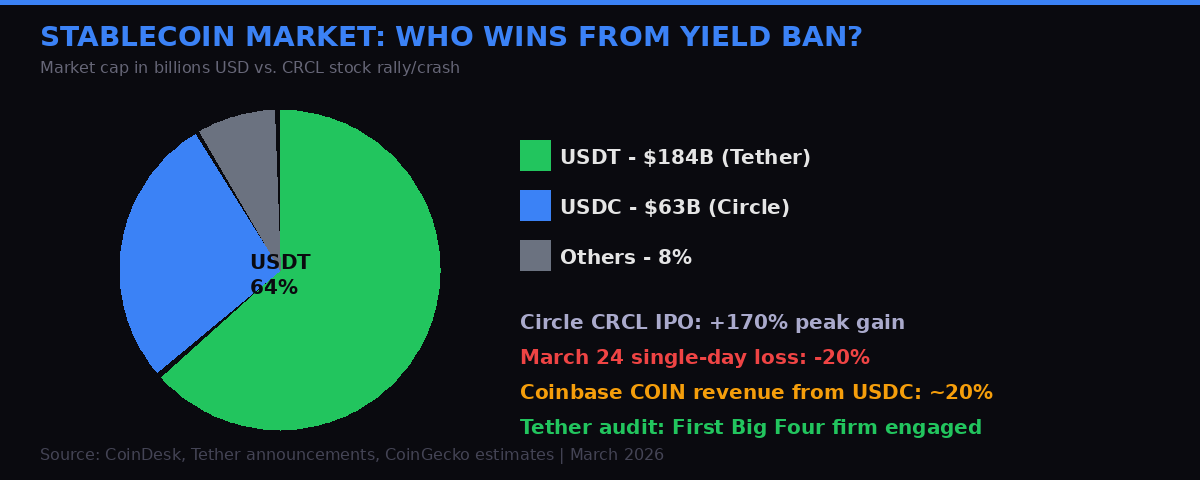

While Circle was hemorrhaging share price points, its arch-rival made a calculated announcement. Tether - issuer of the world's largest stablecoin USDT at $184 billion market cap - said Tuesday it has engaged a "Big Four" accounting firm for its first-ever full financial statement audit. [CoinDesk, March 24]

"The Big Four firm was selected through a competitive process because the organisation is already operating at Big Four audit standard. The audit will be delivered." - Simon McWilliams, CFO, Tether [via CoinDesk]

Tether has previously published only periodic attestations - a weaker form of financial verification that confirms certain numbers at a point in time but does not involve a comprehensive review of controls, liabilities, and reporting systems. A full audit goes far beyond that. It is the standard applied to publicly traded companies. For Tether to submit to that standard is a significant institutional maturation.

The timing is almost certainly not coincidental. With Circle under legislative fire and its stock in freefall, Tether is positioning itself as the "safe" stablecoin - the one with real reserves and now real audit credibility. If the full audit confirms that USDT's $184 billion in circulating supply is fully backed by liquid, high-quality assets (primarily U.S. Treasury bills, as Tether claims), it would dramatically strengthen USDT's standing with institutional users who have long harbored doubts.

Tether did not name the auditor. The Big Four are Deloitte, EY, KPMG, and PwC. Given that BDO previously conducted attestations for Tether and a Big Four engagement signals an upgrade, market observers are speculating across all four. The firm will conduct "a detailed review of assets, liabilities, controls and reporting systems" - the full package.

Tether commands 64% of the stablecoin market at $184B. The Clarity Act yield ban would primarily hurt Circle's USDC and its Coinbase pass-through model. (BLACKWIRE analysis)

The backdrop: S&P downgraded USDT's rating in November 2025, citing bitcoin and gold allocations within its reserve mix as liquidity risk factors. Tether has also faced questions about loans to counterparties that might not be immediately liquid in a stress scenario. A clean Big Four audit would address many of these concerns in a way that attestations cannot.

For the market, the implications are pointed. If the audit goes well, institutional hesitation about USDT evaporates. Pension funds, corporate treasuries, and sovereign wealth vehicles that have been sitting on the sidelines - wary of Tether's opacity - might shift. That would be USDT market share expansion at USDC's expense, at exactly the moment USDC's yield advantage is being legislated away.

The NYSE-Securitize Deal: Traditional Finance Goes All-In on Tokenization

Buried under the Circle crash headlines, the New York Stock Exchange announced a partnership with Securitize to build the infrastructure backbone of NYSE's planned Digital Trading Platform. [CoinDesk, March 24]

This is not a pilot program or a research initiative. NYSE parent Intercontinental Exchange (ICE) signed a memorandum of understanding with Securitize - the BlackRock-backed tokenization specialist currently going public via a SPAC deal with Cantor Equitize Partners (CEPT). The goal: migrate stock ownership records and settlement infrastructure to blockchain rails, enabling 24/7 trading and near-instant settlement for equities.

The implications are profound. Stock markets currently operate on T+1 settlement (trade plus one business day). Blockchain-native settlement would be near-instant and always-on - no market hours, no weekend closures, no clearinghouse delays. For global investors in different time zones, that is a structural improvement in capital efficiency.

"As we explore how tokenization can enhance capital markets, it is critical that new infrastructure is developed in a way that preserves the trust, transparency, and protections investors expect." - Lynn Martin, President, NYSE Group [via CoinDesk]

The competitive race is already accelerating. Nasdaq received regulatory approval for its tokenized stock trading framework last month and has tapped Kraken to distribute tokenized stock tokens globally. NYSE-parent ICE also recently invested in OKX to develop tokenized stocks and derivatives. Invesco took over Superstate's $900 million onchain Treasury fund. Securitize's CEPT shares jumped 6% on the NYSE news.

This is the other side of the crypto story that gets lost in the noise of daily price moves: the infrastructure of traditional finance is quietly migrating to blockchain rails. The question is not whether markets tokenize - it is who controls the plumbing when they do. Right now, it is a three-way race between crypto-native platforms, traditional exchanges going hybrid, and bank-built solutions.

Bernstein Calls the Bottom - $150K Target Unchanged

At the same time markets were melting down, Wall Street broker Bernstein published a note to clients reiterating its $150,000 year-end price target for bitcoin. [CoinDesk, March 24]

"We believe Bitcoin has found its trough and is now heading higher." - Gautam Chhugani, Bernstein analyst

The bull case from Bernstein rests on three pillars. First, onchain cost basis data suggests the $60,000 zone is a critical support - representing the average acquisition cost of bitcoin bought in 2023, a cohort that historically holds through corrections. Second, ETF flows remain resilient even during the pullback, with institutional buyers treating dips as entry points rather than exits. Third, corporate treasury demand continues to expand - Strategy (formerly MicroStrategy) now holds approximately 3.6% of all bitcoin in circulation, worth roughly $53.5 billion at current prices.

Bernstein also noted a striking macro data point: since the onset of the Iran conflict in late February, bitcoin has outperformed gold by 25%. That is not a coincidence. Gold is the traditional crisis hedge. Bitcoin is the new one - for investors who need censorship-resistant, portable, 24/7 liquid stores of value. Geopolitical stress is supposed to hurt risk assets. For bitcoin, it increasingly doesn't.

The implied volatility picture supports the bottoming thesis. DVOL (Deribit's Bitcoin Volatility Index) and BVIV (Bitcoin Volatility Index) suggest peak fear has passed. Leverage has been washed out. Long liquidations from overleveraged positions are mostly behind the market. What remains is spot demand from ETF flows and corporate treasuries.

The counterargument is macro. A rate hike - even a 15% probability - changes the calculus for risk assets broadly. Bitcoin at $150,000 by year-end requires either rate cuts materializing by Q3, or a geopolitical resolution that collapses oil prices and relieves pressure on inflation data. Neither is guaranteed.

Iran Ceasefire Report - The Last-Minute Wildcard

Oil's sudden 4% drop after reports of a potential Iran-Israel ceasefire framework temporarily lifted crypto markets late Tuesday. (Pexels)

Just when Tuesday looked like a clean bearish close, Israeli Channel 12 reported that a one-month ceasefire between Israel and Iran could be announced soon, as part of a package being negotiated by White House envoys Steve Witkoff and Jared Kushner. The reported deal terms: Iran would dismantle its existing nuclear capabilities and vow to never seek nuclear weapons. [CoinDesk, March 24]

The immediate market reaction was sharp. Brent crude dropped from $104 to below $100 in minutes - a 4% swing triggered by a single news report. Bitcoin, which had been trading near $69,000, quickly recovered to $70,000. U.S. stock index futures posted small gains.

The Iran conflict has been the defining macro event of early 2026. Since hostilities escalated in late February, oil has added roughly $15-20 per barrel. That has kept inflation expectations elevated and progressively eroded the rate cut narrative that crypto bulls were counting on. If a genuine ceasefire materializes, the policy picture shifts materially: oil back toward $85-90 would ease inflation pressure, restore rate cut expectations, and remove the risk premium currently embedded in energy-sensitive assets.

But a single Israeli TV report is not a signed treaty. The market has been burned before by ceasefire headlines that evaporated within 48 hours. The relief rally was muted - bitcoin recovered $1,000, not $10,000. The smart money is pricing geopolitical resolution as a low-probability event, not a base case.

BlackRock's New Thesis: AI, Not Altcoins, Is Crypto's Next Driver

Separately, BlackRock's head of digital assets, Robbie Mitchnick, spoke at the Digital Asset Summit in New York on Tuesday and offered an unusually blunt assessment of where institutional interest in crypto is heading. [CoinDesk, March 24]

"The majority of that is nonsense." - Robbie Mitchnick, Head of Digital Assets, BlackRock, referring to the vast majority of crypto tokens in circulation

Mitchnick's message: institutional money is concentrating into bitcoin and ether, with "pretty ferocious" turnover among other tokens. Most newer tokens fail to maintain long-term relevance. The result is a portfolio landscape where BTC and ETH dominate allocations and altcoin exposure is minimal and declining.

What replaces altcoin enthusiasm as the narrative driver? According to Mitchnick: artificial intelligence. His framing was precise and worth quoting in full: "AI agents are very unlikely to use Fedwire and SWIFT. What is crypto? Crypto is computer-native money. AI is computer-native data and intelligence. And so there's a natural symbiosis there."

That positions crypto not as speculative capital - the meme coin casino - but as infrastructure. The money layer for the AI economy. Bitcoin miners are already pivoting toward AI workloads: Hut 8, Core Scientific, and Iren are all either repurposing data centers or signing hosting deals for AI high-performance computing. The revenue is steadier than block rewards and the demand is accelerating.

From a portfolio construction standpoint, Mitchnick suggested bitcoin also functions as a diversifier during technological disruption - a "stabilizing allocation" when AI-driven automation reshapes industries and creates uncertainty. That is a more sophisticated institutional narrative than "digital gold" or "inflation hedge" - and it has more staying power.

Timeline - Key Events, Q1 2026

What Comes Next: The Clarity Act Fight Is Not Over

Tuesday's session was brutal but not terminal for the stablecoin yield story. The Clarity Act has been stuck in legislative limbo for nearly two years. Getting it through the Senate Banking Committee is the next major step - and the yield language is just one of multiple sticking points remaining.

Democrats are pushing for provisions that ban senior government officials from personally profiting from crypto - a clause obviously aimed at President Trump's crypto interests. There are also unresolved questions about DeFi oversight and anti-money laundering protections. The yield ban may be a negotiating chip rather than a final position.

"There will be workarounds," said Bitwise's Ryan Rasmussen. The most likely path: loyalty programs and activity-based reward structures that technically comply with the "activities not balances" framework while functionally replicating yield. Companies like Circle and Coinbase have armies of lawyers. They will find the structure that works.

The longer game favors both companies. Circle still commands 28% of a stablecoin market projected to grow 10x over four years. Coinbase is the dominant U.S. crypto exchange with diversified revenue from trading fees, custody, and its Base blockchain ecosystem. A 20% single-day drop on legislative uncertainty does not change those fundamentals.

But the market has been reminded of something important: crypto companies are operating in a regulatory environment that can change the rules faster than their stock prices can adjust. The Clarity Act's text moved in closed-door sessions on a Monday night, and by Tuesday afternoon, $4 billion in market cap had evaporated. That is the tail risk that no DCF model fully captures.

Meanwhile, Tether is executing a quiet power play. The Big Four audit - assuming it goes forward and returns clean results - would validate USDT's reserve structure in a way that no attestation ever could. It would remove the final major institutional objection to USDT adoption and potentially flip the market share narrative that briefly turned USDC's way when volumes crossed over last month.

Watch the Fed. Watch the audit. Watch the Clarity Act markup. All three have direct lines to crypto asset prices, stablecoin market structure, and crypto equity valuations. Tuesday was not the end of the story - it was the setup for a chapter that will likely define crypto market structure for the rest of 2026.

Key Numbers To Track

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram