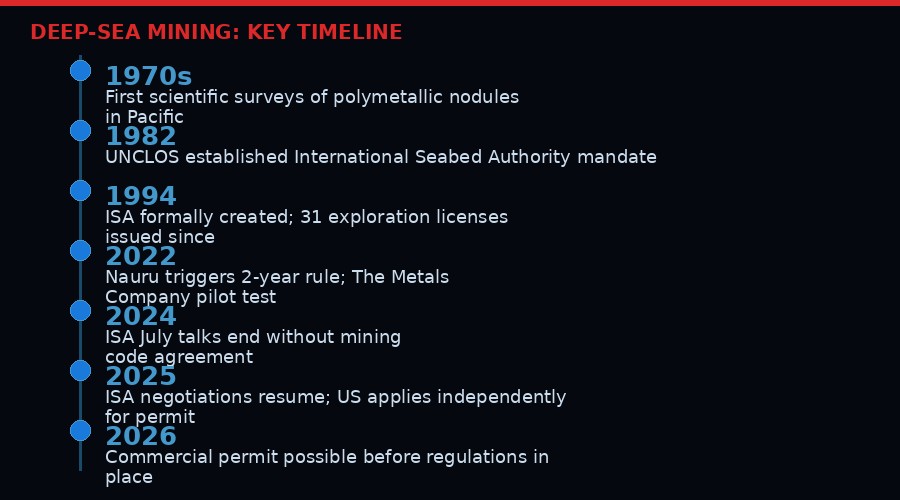

More than 13,000 feet below the surface of the Pacific Ocean, a machine bigger than a city bus trundled across the seafloor on caterpillar tracks, sucking up potato-sized rocks and pumping them through a two-mile riser pipe to a ship above. It was 2022, the pilot was declared a success, and the age of industrial deep-sea mining edged another step closer.

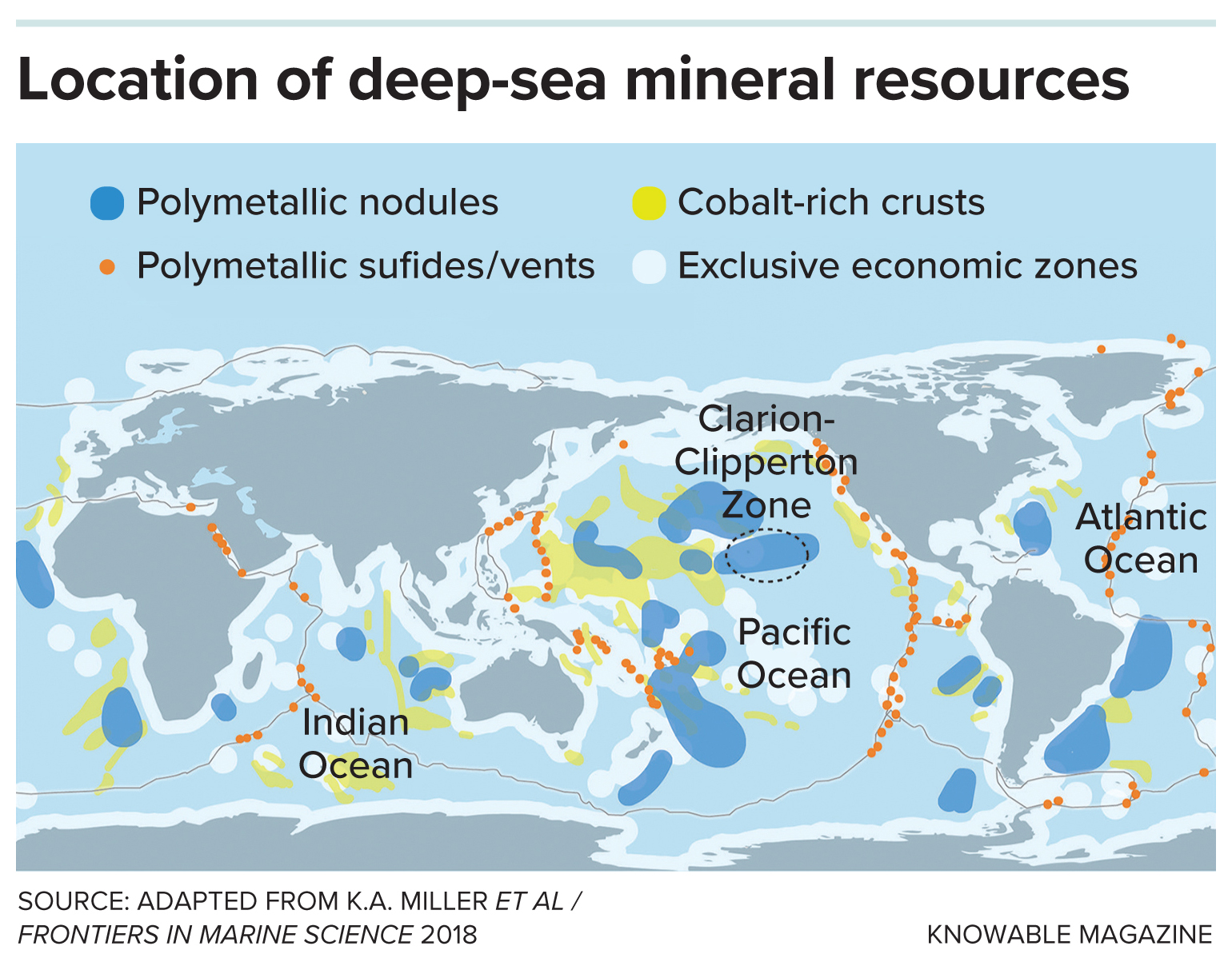

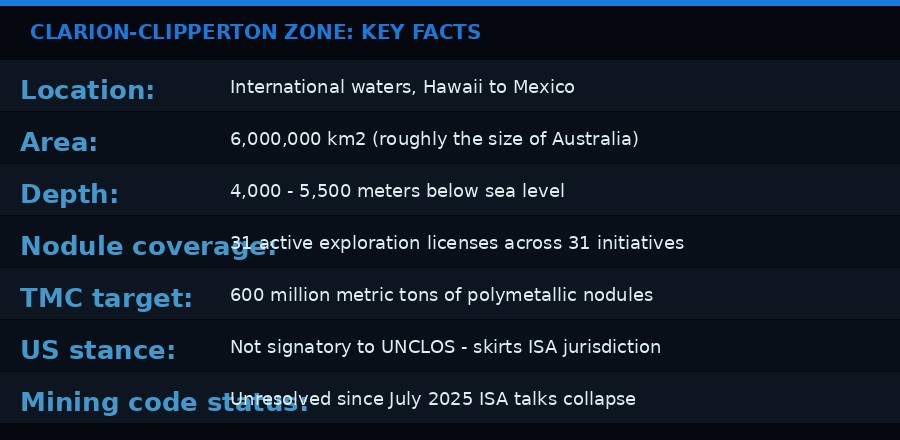

That machine belonged to The Metals Company, a Canadian mining firm that now wants to deploy similar hardware commercially across 65,000 square kilometers of the Clarion-Clipperton Zone - an area between Hawaii and Mexico roughly the size of France. The target: 600 million metric tons of polymetallic nodules, each one a layered sphere of manganese, cobalt, nickel, and copper built up over millions of years at the pace of a few millimeters per million years.

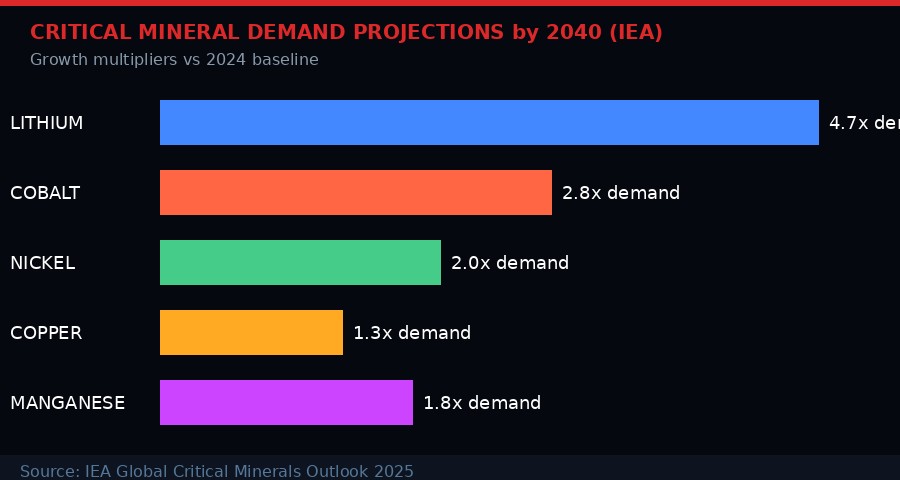

The stakes are enormous in both directions. The green energy transition genuinely requires vast quantities of critical minerals, and the question of where to get them is increasingly urgent. The International Energy Agency projects that demand for lithium will grow 4.7 times by 2040. Cobalt demand is expected to nearly triple. Copper - the metal that carries electricity through wind turbines, EV motors, and grid infrastructure - faces projected shortfalls as early as 2035.

But the rules governing who can mine the deep ocean, how, under what conditions, and with what environmental safeguards - are still being negotiated. International talks collapsed in July 2025 without agreement. Meanwhile, companies are finding ways to start before any code exists.

What's Actually Down There

The Clarion-Clipperton Zone is a 6-million-square-kilometer tract of international seafloor stretching from roughly Hawaii to Mexico. It sits 4,000 to 5,500 meters below the surface - deep enough that sunlight never penetrates, pressure runs at 400-500 atmospheres, and temperatures hover near freezing year-round.

What makes it commercially interesting is what sits on the sediment: billions of polymetallic nodules. These are naturally occurring rock formations that grow around a microscopic nucleus - often a shark tooth or a fragment of ancient sediment - one layer at a time, over geological timescales. A nodule the size of a potato took several million years to grow.

Each nodule contains roughly 26 percent manganese, 1.3 percent nickel, 1.1 percent copper, and 0.2 percent cobalt by weight, according to the International Seabed Authority (ISA). The ISA estimates the Clarion-Clipperton Zone alone holds more cobalt than all known land-based deposits combined. Nickel reserves in the Zone exceed the entire nickel inventory of Indonesia - currently the world's largest supplier.

The nodules are also unusually concentrated and accessible compared to terrestrial ore bodies. They sit on top of the sediment, not buried within it. In theory, you don't need to blast or chemically leach rock - you drive a machine over them and vacuum them up. That's the pitch, anyway.

Thirty-one national and commercial entities currently hold ISA exploration licenses in the Zone, including China (the most aggressive, with multiple contractors), India, South Korea, Japan, France, Germany, and Russia. Each license covers a specific plot of seafloor and authorizes research and surveying - not commercial extraction. That step requires a separate commercial permit under an as-yet-unfinished mining code.

The ISA has been drafting that code since 2012. It is still not finished.

The Green Transition's Dirty Secret

The case for deep-sea mining is inseparable from the energy transition. Electric vehicles need lithium, cobalt, and nickel for their batteries. Wind turbines need copper for their generators. Solar panels need indium, gallium, and tellurium. Grid-scale battery storage needs manganese and vanadium. And all of this demand is projected to grow simultaneously over the next two decades.

The IEA's 2025 Global Critical Minerals Outlook modeled three scenarios - conservative, moderate, and aggressive renewable deployment - and in every scenario, projected mineral demand outpaces projected land-based supply by the mid-2030s. The most vulnerable metal is lithium, where demand growth of 4.7 times by 2040 strains even optimistic supply projections. Copper shortfalls could begin as soon as 2035.

"In general, the rock with high copper content has really been mined already," Shobhan Dhir, a critical minerals analyst at the IEA, told Knowable Magazine. The easy deposits are gone. What remains requires going deeper, processing lower-grade ore, or finding entirely new sources.

The IEA estimates the green transition will require more than 85 new lithium mines by 2050, up to 40 new nickel mines by 2030, and at least 35 new copper mines by 2050. Each of those projects takes 10 to 20 years from discovery to production. The math is uncomfortably tight.

Proponents of deep-sea mining argue that the Clarion-Clipperton Zone alone could supply decades of critical mineral demand without the land-clearing, water contamination, and community displacement that characterizes terrestrial mining. The Metals Company likes to point out that its nodule mining would displace no human communities, generate no toxic tailings ponds, and leave no open pits. These points are technically accurate. They do not tell the whole story.

The Ecology No One Fully Understands

The abyssal plains of the Pacific are among the least studied environments on Earth. Scientists estimate that fewer than 0.0001 percent of the deep ocean floor has been sampled with any biological detail. The Clarion-Clipperton Zone is home to thousands of species - many of them found nowhere else on the planet - and the vast majority have not been formally described or named.

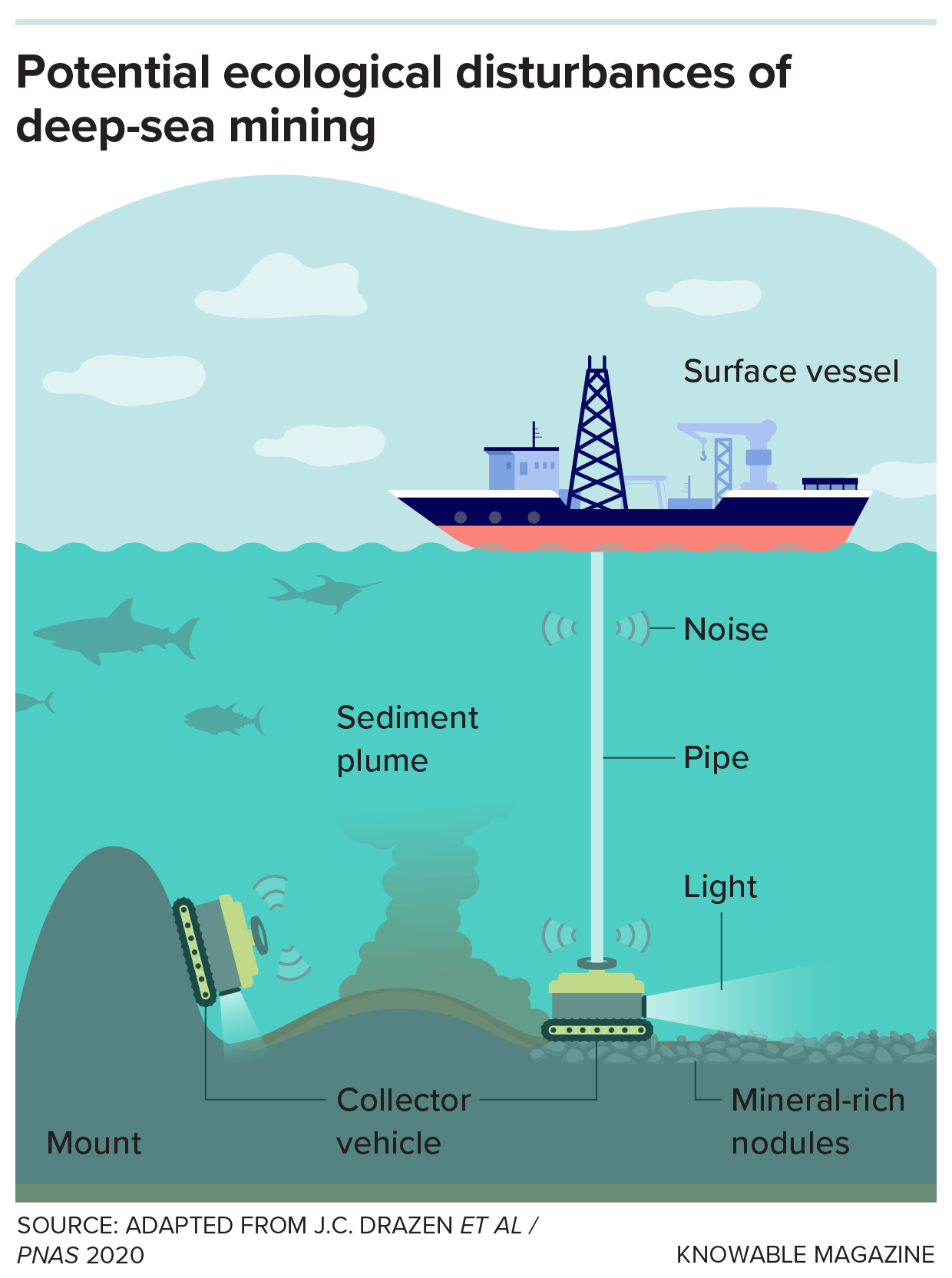

Mining operations in this environment create several distinct categories of harm. The harvester vehicles themselves crush whatever is directly in their path as they move across the nodule fields. The collection process kicks up dense plumes of fine sediment that can travel hundreds of kilometers through the water column, suffocating filter-feeding organisms and blocking light for chemosynthetic bacteria. Extraction releases heavy metals - cadmium, lead, mercury, arsenic - that have been locked in the nodules for millions of years, into water that was previously clean.

And then there are the nodules themselves. The same slow growth rate that makes them geologically remarkable makes their loss permanent on any human timescale. A nodule that took 10 million years to form cannot be regrown in a regulatory cycle or a mining company's operational lifespan. When they're gone, they're gone.

The Metals Company cites research suggesting that "some" deep-ocean fauna communities could start to recover within one year of disturbance, and that microbial communities might recover within 50 years. These figures come from small-scale test mining experiments, not commercial-scale operations. The extrapolation from a test patch to 65,000 square kilometers of commercial extraction is not scientifically validated.

"The effects of polymetallic nodule mining are likely to be long term. Our analyses show considerable negative biological effects of seafloor nodule mining, even at the small scale of test mining experiments."

- Research paper The Metals Company cites for quick recovery claims

Anna Metaxas, a deep-sea ecologist at Dalhousie University, attempted to develop a comparative framework for assessing whether terrestrial or deep-sea mining causes more environmental harm. Her team published their conclusion in 2024: the data do not currently exist to make that comparison with any scientific credibility. "Our knowledge gaps are really large," says Matthias Haeckel of the GEOMAR Helmholtz Centre, who is leading the ISA's technical working group on environmental standards.

That working group is expected to submit a first draft of monitoring standards sometime later in 2026. Commercial mining permits could theoretically be issued before those standards are finalized.

The Governance Void - And the Loopholes Being Exploited

The International Seabed Authority is a UN body established under the 1982 United Nations Convention on the Law of the Sea (UNCLOS). Its mandate covers the governance of mineral resources on seabeds in areas beyond national jurisdiction - the international commons sometimes called "the Area." It has jurisdiction over the deep ocean floor that no country claims as its own, including the Clarion-Clipperton Zone.

Since 1994, when the ISA formally began operations, its member states have been negotiating a "mining code" - the set of rules, standards, and procedures that would govern commercial extraction. Despite three decades of effort, that code does not exist in final form. ISA talks in July 2025 ended with major unresolved issues: how to measure ecological impacts, what baseline data would be required before permits are issued, how mining revenues would be distributed to developing nations, and what environmental liability would look like if a company caused irreversible damage.

Into that void, two actors are moving fast. The first is Nauru, a 21-square-kilometer island nation in the southwestern Pacific with a population of roughly 10,000. Nauru sponsors The Metals Company's exploration license. In 2021, Nauru invoked an obscure provision in UNCLOS known as the "two-year rule" - which obliges the ISA to complete the mining code within two years of being formally notified that a member state wishes to proceed with commercial applications. That notification expired in 2023 without a completed code. Legal scholars are still debating whether that triggers an obligation for the ISA to grant permits anyway or simply creates a procedural anomaly.

The second actor is the United States - which is not an ISA member at all.

Washington never ratified UNCLOS. It is not bound by the ISA's authority. And in 2025, The Metals Company applied directly to the US government for a commercial mining permit under US domestic law. The application covers operations in the Clarion-Clipperton Zone - international waters that the ISA considers to be under its jurisdiction. The US disagrees with that framing and has its own legal framework for authorizing US nationals to mine the deep seabed, predating UNCLOS, called the Deep Seabed Hard Mineral Resources Act of 1980.

The company says it expects a US permit by the end of 2026 and plans to begin commercial operations shortly after. This would make it the first company to commercially mine the international seabed - and it would do so outside the ISA framework entirely, setting a precedent that could unravel a decade of multilateral negotiations.

Governance Risk

A US-permitted mining operation in the Clarion-Clipperton Zone, proceeding outside ISA jurisdiction, would create a direct conflict with international seabed governance. It could trigger a legal challenge at the International Tribunal for the Law of the Sea - but the US, not being an UNCLOS signatory, would not be bound by any resulting ruling.

Can Land Mining Fill the Gap Instead?

Not everyone accepts the premise that deep-sea mining is necessary. Gavin Mudd, director of the Critical Minerals Intelligence Centre at the British Geological Survey, argues that the case has been overstated. Land-based reserves for most critical minerals are actually growing, not shrinking, as exploration advances and higher prices make previously uneconomic deposits viable.

USGS data from 2025 show global lithium reserves on land of 30 million metric tons and resources of 115 million metric tons. With annual demand projected to reach 1.5 million metric tons by 2040, that represents at least 20 years of reserves at full demand - and resources for many decades beyond that. "There is no rational case to argue that we will be running out of lithium reserves any time soon," Mudd says.

Mudd makes similar arguments for cobalt and nickel. A 2022 assessment he co-authored estimates land-based nickel reserves and resources can meet demand for over 100 years. The challenge, he says, is not geological scarcity - it's investment timelines, permitting backlogs, and geopolitical concentration of supply chains.

Recycling adds another dimension. The IEA estimates that by 2050, battery recycling alone could reduce new mining requirements by 25 percent for lithium and nickel, and 40 percent for copper and cobalt. A 2025 UC Davis study found that optimistic recycling scenarios could cut the number of new lithium mines needed from 85 to just 15. Paul Anderson, a chemist leading battery recycling research at the University of Birmingham, argues the industry has largely designed recycling as an afterthought rather than a core system requirement.

The counter-argument is not that land-based supply is physically unlimited - it's that the timelines don't work. Opening a new terrestrial mine requires 10-20 years from discovery to first production. If demand shortfalls arrive in 2035, projects that haven't started permitting yet won't help. Deep-sea proponents argue the Clarion-Clipperton Zone could compress that timeline - and do so while displacing populations of approximately zero humans.

The comparison breaks down when you account for the fact that deep-sea mining has no operational track record at commercial scale, has never been done in a way that allows post-hoc environmental assessment, and would occur in an ecosystem that science cannot currently characterize fully.

Competing Powers, Competing Agendas

The geopolitics layered over this debate are considerable. China currently dominates the processing of most critical minerals, even when they're extracted elsewhere - it controls roughly 60 percent of global lithium processing, 80 percent of cobalt refining, and 90 percent of rare earth processing. Chinese state-owned enterprises hold multiple ISA exploration licenses in the Clarion-Clipperton Zone.

For the US and its allies, deep-sea mining has an obvious appeal that goes beyond climate policy: it's a potential route to critical mineral supply chains that bypass Chinese processing dominance. The US Geological Survey currently lists 50 minerals as "critical" to national security and economic competitiveness, and China is a dominant player in supply chains for most of them.

Trump administration officials have been explicit about this framing. Executive orders signed in 2025 directed federal agencies to identify and develop domestic and allied-nation critical mineral supply chains, citing national security. The Metals Company's application for a US permit sits directly within that political context - it offers a legal vehicle for US-licensed extraction of minerals the government wants access to, using a domestic law that bypasses the multilateral governance structure Washington was never part of.

The European Union is watching with anxiety on multiple fronts. EU member states - France, Germany, Belgium - hold ISA exploration licenses and want to operate within the ISA framework. The prospect of a US-licensed operation proceeding unilaterally undermines both the governance framework EU states have invested in and the competitive position of European mining companies that have played by multilateral rules.

India is the third major actor. It holds several ISA licenses and has been less aggressive about timelines than China or the US-backed commercial applicants. But Indian officials have signaled that they view deep-sea minerals as a long-term strategic resource, not just an economic opportunity.

Who Holds Exploration Licenses in the CCZ

- China - Multiple contractors via COMRA and state enterprises

- The Metals Company (Nauru-sponsored) - Largest single commercial applicant

- Belgium (DEME subsidiary) - Global Sea Mineral Resources, active testing

- Germany - Federal Institute for Geosciences (BGR)

- France - IFREMER (state oceanographic institute)

- India - National Institute of Ocean Technology

- South Korea - Korea Institute of Ocean Science

- Japan - JOGMEC (state resource agency)

- 31 total licenses across multiple zones including Indian Ocean

What the Science Can and Cannot Tell Us

The scientific community is not monolithic on this issue. Some researchers, like Saleem Ali at the University of Delaware, argue that deep-sea mining should be evaluated comparatively - not against a perfect alternative, but against the realistic alternative of massively expanding terrestrial mining with its documented record of deforestation, water contamination, and human rights abuses in the Global South.

Studies suggest that terrestrial mining is responsible for 9 percent of all Amazon forest cleared between 2005 and 2015. It uses enormous volumes of water in regions already under water stress. The cobalt mines of the Democratic Republic of Congo, which supply most of the world's battery cobalt, have a well-documented record of child labor and community displacement.

Deep-sea mining, Ali notes, would not directly displace any communities. Its carbon footprint per tonne of mineral extracted may be lower than terrestrial alternatives. Its waste streams are better understood and more spatially contained. These are real advantages - if the environmental cost to deep-sea ecosystems can be accurately measured and mitigated.

That "if" is doing a lot of work. The critical problem is not that deep-sea mining is definitively more harmful than terrestrial mining - it's that we don't know. The ecosystem baseline data required to assess harm doesn't fully exist. The monitoring standards to detect harm are still being drafted. The legal framework to assign liability if harm occurs hasn't been agreed.

Anna Metaxas, whose team tried to build the comparison framework, concluded in 2024 that existing data are too sparse to support a scientifically credible comparison. Matthias Haeckel's ISA technical working group is trying to develop that baseline now - but their first draft isn't due until later this year, and commercial operations could begin before it's even completed.

The European project MiningImpact, led by Haeckel, is returning this year to research sites where Belgian company DEME ran small-scale test operations in 2021. The goal is to assess how the ecosystem has fared five years later - a crucial data point that will either support or undercut claims about recovery timelines. That data will arrive around the same time as the first commercial permit decisions.

In that sense, the science and the politics are racing each other. The companies want to mine before regulations exist. Regulators want regulations before mining starts. Scientists want data before regulations are written. And the deep ocean, utterly indifferent to all of it, continues its million-year cycles 4,500 meters below.

The Second-Order Effects: What Mining Means for the Broader Ocean

Even if the direct footprint of nodule harvesting is contained to the immediate seabed, the secondary effects extend further than the machines. Sediment plumes generated by the collector vehicles can spread across hundreds of kilometers. Research from past test mining operations in the 1970s - the IOMeC experiment - documented sediment plumes persisting for decades in the water column. Those tests covered a few square kilometers. Commercial operations would cover tens of thousands.

The riser pipes that carry nodules from the seafloor to surface ships release processing water back into the deep ocean at a different depth than it was extracted from. That water contains disturbed sediment, fine particles of crushed minerals, and elevated concentrations of metals. The chemical signature of that discharge in an otherwise pristine water column is poorly characterized.

Noise pollution deserves particular attention. The deep ocean is not silent - it's a rich acoustic environment used by whales, fish, and other marine mammals for communication, navigation, and foraging. The commercial mining operations envisioned for the Clarion-Clipperton Zone would run continuously, 24 hours a day, across a geographic area the size of France. The acoustic footprint of that activity - and its interaction with existing cetacean migration routes - has received almost no systematic study.

There is also a carbon accounting question that proponents rarely address head-on. The deep ocean is the planet's largest carbon reservoir. Sediment on the abyssal plains sequesters organic carbon that has settled from the surface ocean over millions of years. Mechanical disturbance of that sediment releases carbon back into the water column and eventually the atmosphere. Quantifying that release - and comparing it against the carbon savings from the clean energy technologies those minerals would enable - is a calculation that has not been published in peer-reviewed form.

None of this means the answer is no. It means the question has not been answered rigorously, and the clock is running.

The Crunch Point: 2026

Three decisions are converging in 2026 that will shape the trajectory of deep-sea mining for decades.

First, the ISA Council met in Jamaica in March and will convene again in July. Those sessions represent the last realistic opportunity to adopt a mining code before commercial permits become live controversies rather than theoretical possibilities. The July session is widely viewed as the critical one.

Second, The Metals Company's US permit application is proceeding through the National Oceanic and Atmospheric Administration (NOAA), which administers the Deep Seabed Hard Mineral Resources Act. The company says it expects a decision by the end of 2026. If that permit is granted, it creates an immediate collision between US domestic law and international seabed governance - with no established mechanism for resolution.

Third, the MiningImpact scientific cruises will report back on the five-year recovery status of test mining sites. If the news is good - meaningful ecological recovery, contained disturbance - it provides ammunition for the "mining can be done responsibly" camp. If it's bad, the political pressure to pause and reassess will intensify at exactly the moment commercial operations are on the verge of starting.

Forty countries, led by the Pacific island nation of Palau, have called for a moratorium or outright ban on deep-sea mining until the science and governance catch up. That coalition includes France, which simultaneously holds an ISA exploration license - a tension that reflects how difficult it is to hold consistent positions when both geopolitical advantage and environmental principles are at stake.

"The regulator is no longer an independent regulator - we do not know whose interests it is serving. The safety culture is under threat."

- Allison Macfarlane, former NRC chair (speaking about a parallel deregulation story, but the sentiment echoes here)

The deeper structural problem is that the global governance architecture for the commons - the high seas, the atmosphere, the shared spaces that belong to no nation - was built for a world that moved more slowly. The ISA has been negotiating for 14 years and counting. The technology to commercially mine the seabed has outpaced the institutions designed to manage it.

That gap - between what is technically possible and what is politically governed - is the real frontier in the deep-sea mining debate. Not whether the minerals are there. They clearly are. Not whether demand will materialize. It already is. But whether humanity can organize itself to extract those resources without first destroying environments it has barely studied and certainly cannot recreate.

The machines are ready. The permits are pending. The science is incomplete. The rules don't exist yet. And the ocean doesn't negotiate.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on TelegramPrimary Sources

- Ars Technica / Knowable Magazine: "Mining the Deep Ocean" (March 22, 2026)

- IEA Global Critical Minerals Outlook 2025 - iea.org

- ISA International Seabed Authority Council sessions, Jamaica, March 2026

- Mudd & Jowitt: "The New Century for Nickel Resources" - Economic Geology, 2022

- Metaxas et al: Comparative framework for terrestrial vs deep-sea mining - Global Change Biology, 2024

- MiningImpact European Research Project - GEOMAR Helmholtz Centre for Ocean Research

- Drazen et al: Ecological overview of the Clarion-Clipperton Zone - PNAS, 2020

- Deep Seabed Hard Mineral Resources Act of 1980 (US domestic law)

- UNCLOS, Article 153 & Annex III (ISA mandate)

- UC Davis: Recycling impacts on lithium mine requirements - Nature Sustainability, 2025