$870 Million Whitewash: How Predatory Lender Tom Dundon Is Cashing Out on Oregon's Dime

The incoming Portland Trail Blazers owner built a $4 billion fortune trapping low-income car buyers in loans regulators called predatory. Now Oregon is handing him $870 million in public money - and the same politicians whose state sued his company are looking the other way.

A billionaire's new home - built, in part, on loans that Oregon called predatory and harmful. Photo: Pexels

Oregon sued his company for preying on vulnerable borrowers. His company paid $550 million to settle. Now Oregon is giving him $870 million to renovate a basketball arena.

That is the arc of Tom Dundon's career - subprime auto lender turned NBA franchise owner - and it is a story about how wealth launders reputation, how politicians forget their own lawsuits, and how the money that stripped equity from working families gets recycled into the kind of public spectacle that makes everyone feel good.

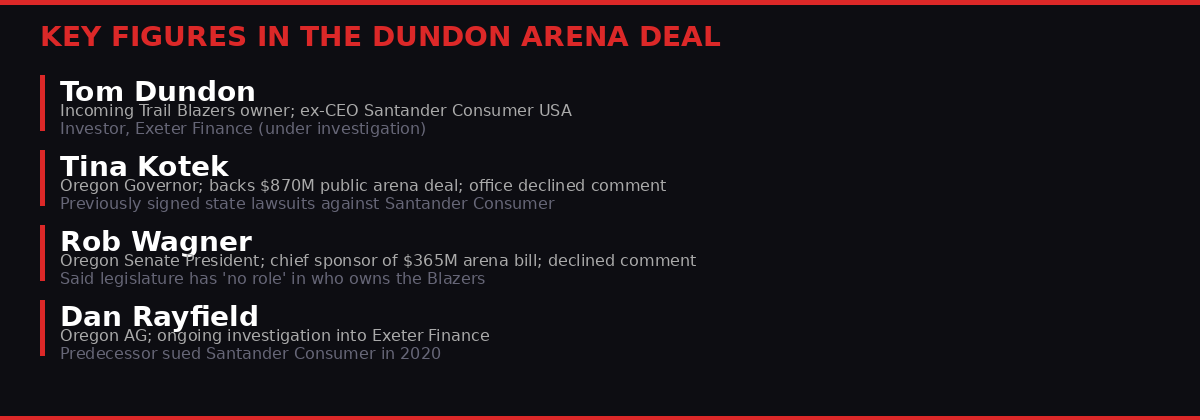

Dundon, a 59-year-old Texas billionaire, agreed in 2025 to buy the Portland Trail Blazers for $4 billion. The deal is expected to close March 31, 2026. Oregon Governor Tina Kotek and Portland Mayor Keith Wilson both publicly championed keeping the team in Portland. The state legislature approved $365 million in public arena funding. Combined with city and county contributions, total public exposure has reached $870 million - far more than the team originally requested, according to ProPublica and Oregon Public Broadcasting's joint investigation published March 25, 2026.

That investigation found that Dundon was not just connected to predatory lending allegations - he was at the center of them. Internal emails obtained by the newsrooms show Dundon personally ordered the waiver of proof-of-income requirements for car loans at Santander Consumer USA in January 2013. The company's own chief risk officer warned the move could violate federal law. The plan proceeded anyway.

Dundon's financial trajectory from subprime auto lender to NBA franchise owner - mapped against the regulatory actions his companies triggered.

Built on Borrowed Names: The Subprime Machine

Tom Dundon did not inherit his fortune. He built it in the least glamorous corner of American finance - used car lots in Texas, where people with bad credit and few options come looking for transportation they cannot afford to buy outright.

In the mid-1990s, Dundon and other former car dealership workers co-founded Drive Financial Services. The company's pitch was simple: it would loan money to people other companies would not touch. Credit scores below 540. Bankruptcy in the file. Prior repossessions. None of it was disqualifying at Drive Financial, as long as the interest rate was high enough to absorb the expected defaults.

In 2006, Spain's Banco Santander bought Drive Financial for $636 million and renamed it Santander Consumer USA. Dundon kept a 10% stake and a seat on the board. He became CEO of the newly formed company and began scaling it aggressively.

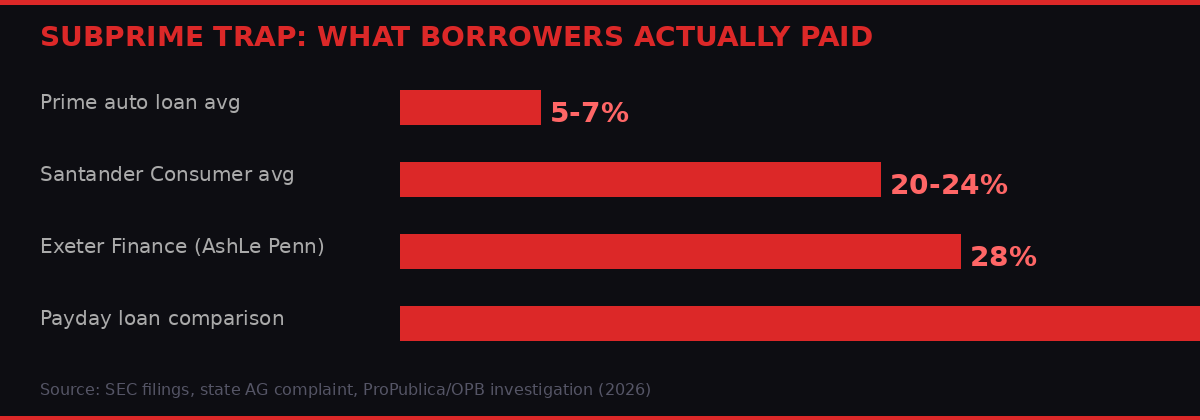

Under Dundon's leadership, Santander Consumer's valuation ballooned from just over $600 million at acquisition to nearly $9 billion by 2014, according to Bloomberg. The company went public in 2014. The growth engine was relentlessly subprime - SEC filings from the company's early years show the average credit score on its loans was below 540, and roughly two-thirds of loans carried interest rates above 20%.

"The money used to buy the Portland Trail Blazers is money that was built on predatory lending. He had an opportunity. He seized it. He made lots of profit. And how did he make that profit? He made it on the backs of low- and poor-credit individuals." - Mark Williams, former Federal Reserve regulator and Boston University finance professor, to ProPublica (2026)

That description - "on the backs of" - captures something regulators would later confirm in legal filings. The system was designed to profit even from failure. Santander Consumer charged higher interest rates specifically to compensate for expected defaults, and it structured loans knowing many borrowers would default and lose their vehicles. Oregon's 2020 court complaint stated that many borrowers took out loans under the "false pretense" that they were acquiring a car they would eventually own, when in fact the terms were so onerous that default was nearly inevitable.

Santander Consumer USA issued loans with average interest rates above 20% to borrowers regulators later called systematically misled. Photo: Pexels

The Proof-of-Income Email

The most damaging material in the ProPublica and OPB investigation is not a regulatory filing or court complaint. It is a series of emails from January 2013 in which Dundon, as CEO, personally pushed to eliminate one of the most basic safeguards in lending: the requirement that borrowers prove they can afford to repay a loan.

On January 21, 2013, Dundon wrote to two senior employees: "Lets do a test. I want to waive poi more often." POI stands for proof of income - the standard documentation showing that a borrower earns enough to service the debt they are taking on.

The same day, Santander Consumer's chief risk and compliance officer, Michele Rodgers, raised alarm. She sent an email identifying potential violations of anti-money laundering and identity theft laws. She also noted that federal regulators were about to implement rules for mortgage lenders requiring them to assess a borrower's ability to repay - and flagged the parallel risk for car loans.

Her concerns did not stop the plan.

Two weeks later, Santander's executive vice president of sales and marketing, Matt Fitzgerald, described a conversation with Dundon in an email: "I just rode up the elevator with TD and he wants us to market (fax, e-mails, sale handout) the waiving of stips to all dealers. And he wants to see these communications by the end of the day."

Stips - stipulations - are the income and address verifications that protect lenders from fraud and protect borrowers from loans they cannot afford. Dundon wanted them gone because they were "reducing capture especially in the nearprime segment" - limiting how many loans the company could close.

The $550 million settlement with attorneys general in 2020 covered more than 265,000 borrowers. Oregon's share was $25 million, affecting over 2,000 state residents.

The risk-versus-profit calculus was explicit. According to the slide presentation regulators prepared for Santander Consumer during the multistate investigation, the company would "build in pricing to cover the incremental risk" - meaning it would charge higher rates precisely because it knew some of these no-income-verification loans would fail. Profit was built into the failure.

Dundon left Santander Consumer in 2015. The multistate investigation concluded five years later with a $550 million settlement covering more than 265,000 borrowers in 33 states. Oregon's then-Attorney General Ellen Rosenblum described the practices as "predatory and harmful and will not be tolerated in Oregon." The settlement agreement specified that it did not constitute an admission of liability by Santander Consumer.

Exeter Finance: The Investigation Still Running

Dundon did not exit the subprime auto lending industry when he left Santander Consumer. He invested in Exeter Finance, another national subprime auto lender, and served as chairman of its board. His investment website lists Exeter as a portfolio holding.

As of March 2026, Oregon is part of an ongoing multistate investigation into Exeter Finance. The Oregon Department of Justice confirmed to ProPublica and OPB its role in the investigation - which Exeter itself has disclosed in securities filings. The company says it is cooperating.

The human cost is not abstract. AshLe' Penn, a single mother of three in Oregon, needed a car in 2021. Her credit was poor. A dealership secured her an Exeter Finance loan on a 2014 Chrysler 300 at 28% interest - $511 per month for 72 months.

By January 2023, Penn was three payments behind and had been evicted from her apartment. She was living in the Chrysler when Exeter sent a repossession agent late at night, while she was parked outside her ex-partner's home. Her daughters watched from inside. Penn spent more than ten hours locked in her car in a standoff with the repo agent before a bankruptcy attorney intervened.

"It was horrific. I mean, I cried. I cried for God. I was afraid to leave my car. I couldn't get out of my car after that. I was just so afraid somebody was going to take it." - AshLe' Penn, Exeter Finance borrower, to ProPublica/OPB (2026)

Penn complained to Exeter and demanded $150,000 in compensation. Exeter told her it had conducted a thorough review and concluded she had failed to make payments and was warned ahead of time. Her version of events, the company wrote, could not be corroborated.

Oregon consumers have filed 23 complaints against Exeter Finance with the Consumer Financial Protection Bureau. All are listed as "closed with explanation."

Santander Consumer and Exeter Finance borrowers paid interest rates three to five times higher than standard auto loan rates - structured, experts say, to profit even from default.

The $870 Million Deal Nobody Discussed

When the Portland Trail Blazers went up for sale in 2025 for the first time in three decades, Oregon politicians moved fast. Governor Tina Kotek and Portland Mayor Keith Wilson co-signed a letter to the NBA promising to work with any incoming owner to secure a renovated arena. The message was unambiguous: Portland would pay to keep its team.

Dundon's group was not the only bidder. But his $4 billion offer won out. Fans celebrated. Local media ran profiles of the Texas billionaire who owned the Carolina Hurricanes hockey team and was now bringing his investment approach to Oregon.

What did not get covered - in any local public discussion before the arena funding vote - was that Oregon had accused his company of preying on its residents. That its attorney general had called those practices "predatory and harmful." That another company in his portfolio was still under multistate investigation by the same office.

Oregon's legislature approved $365 million in public funding for arena renovation in early 2026. Combined with Portland city and county contributions, total public backing reached $870 million. Kotek's office told reporters that was "a great first step."

Total public exposure in the Trail Blazers arena deal - $870 million in taxpayer money flowing to a billionaire whose wealth was built on lending practices Oregon called predatory.

The chief sponsor of the arena bill, Senate President Rob Wagner, declined to answer when asked whether he was aware of Oregon's investigations into Dundon's businesses. His office said: "The Oregon Legislature does not have a role in who owns the Trail Blazers." Governor Kotek's office did not respond to questions about whether she knew of the investigations into businesses connected to Dundon or whether that affected her support for the deal.

State Senator Khanh Pham, one of only six senators to vote no on the bill, said she was not aware of Dundon's history in Oregon until ProPublica and OPB asked her about the newly obtained emails.

"This new information affirms that guardrails on public-private partnerships are important in all instances and especially this one." - Oregon State Senator Khanh Pham (D-Portland), statement to ProPublica/OPB (March 2026)

Current Oregon Attorney General Dan Rayfield, who is part of the ongoing Exeter investigation, offered the sharpest comment. Responding to the proof-of-income waiver emails without referencing Dundon by name, he said: "Proof of income requirements exist for a reason - they protect borrowers from being sold loans they cannot afford. When those guardrails get waived, dealerships win in the short term, and consumers lose."

Oregon's legislature approved arena funding without public discussion of the state's own history with Dundon's companies. Photo: Pexels

How the Machine Works: Anatomy of a Whitewash

What is happening in Portland is not unique. It follows a well-established pattern in how American wealth launders itself through sports franchises, civic partnerships, and public goodwill.

Step one: build wealth in a sector that exploits regulatory gaps and targets people without political power. Subprime auto lending is ideal - the borrowers are dispersed, individually small, and easy to dismiss as bad credit risks who knew what they were getting into.

Step two: exit before the settlement lands. Dundon left Santander Consumer in 2015. The $550 million settlement came in 2020. He was insulated from direct reputational damage by the five-year gap and by the settlement's non-admission clause.

Step three: invest in prestige. Sports franchises are the ultimate reputation cleanser in American culture. NBA ownership confers civic identity. No one asks where the money came from when the team is in the playoffs.

Step four: extract public subsidy. Governments desperate to retain sports franchises routinely offer hundreds of millions in taxpayer money with minimal due diligence on ownership history. The leverage is the threat of relocation - an implicit hostage-taking that politicians rarely resist.

Mark Williams, the former Federal Reserve regulator, summarized the dynamic with precision: "The money used to buy the Portland Trail Blazers is money that was built on predatory lending." That money does not disappear. It does not get redistributed to the borrowers who lost their cars. It buys a franchise, it funds an arena renovation, and it generates decades of positive press coverage.

The officials who approved or remained silent about Oregon's $870 million commitment - despite the state's own legal history with Dundon's companies.

What Accountability Looks Like When It Doesn't Come

The Oregon Department of Justice confirmed it is investigating Exeter Finance. That is meaningful - it means the state's legal machinery is still engaged with Dundon's lending portfolio. But that investigation has nothing to do with the arena deal. The two tracks run in parallel, with no apparent mechanism for one to inform the other.

Dundon himself, when contacted by ProPublica and OPB, responded to a text message: "Unfortunately at this point in the process I am not available. Happy to speak with you after closing. Thx." The deal closes March 31, 2026. After that, the public money will have been committed.

The trail of documentation assembled by the two newsrooms is extensive. Internal Santander Consumer emails. Regulatory slide presentations. Court filings from the multistate investigation. Consumer CFPB complaints. Exeter Finance securities disclosures acknowledging state investigations. None of it was placed before the Oregon legislature before the $365 million vote. None of it was in the public domain at the time the governor's office championed the deal.

The $550 million settlement with Santander Consumer included $65 million in direct restitution to borrowers - roughly $245 per person across 265,000 cases. The rest went to state coffers and legal funds. Kenneth Dost, an Oregon borrower who lost his car during the financial crisis and ended up in a Santander Consumer loan, spoke to ProPublica about the experience of being trapped in debt by a company that was simultaneously being investigated for trapping people in debt. His situation was not exceptional. It was the business model.

There is a version of events in which Oregon's politicians genuinely did not know about the Santander Consumer history or the Exeter investigation when they signed off on the arena deal. That version is not reassuring. It describes a state that failed to conduct basic due diligence on the business record of the billionaire it was about to hand $870 million in public money.

There is another version - one that several of the politicians' non-responses suggest - in which they knew, or should have known, and chose not to make it an issue. That version is more troubling. It describes a state that actively looked away from its own legal record because the prize of keeping the Trail Blazers in Portland was worth more than the accounting.

Neither version is flattering. Both versions are consistent with the documented facts.

The arc of subprime wealth - from loan origination fees extracted from borrowers without proof of income, to a $4 billion franchise purchase backed by $870 million in public money. Photo: Pexels

The Borrowers Who Funded the Arena

It is worth being concrete about who paid for Tom Dundon's $4 billion bid on the Portland Trail Blazers.

They are the 265,000 borrowers in 33 states who were party to the 2020 Santander Consumer settlement. They are the 2,000 Oregon residents whose loans were explicitly included in the state's legal complaint. They are people like AshLe' Penn, who paid 28% annual interest on a car she needed to get to work, then watched a repo agent try to take it while her daughters looked on.

They are the people the University of Utah's Mark Jansen describes as having "no alternative" - borrowers in areas without public transportation where no car means no job, who accepted whatever terms were offered because the alternative was worse. Their interest payments, their late fees, their repossession fees, their refinancing costs - all of it flowed upward through the corporate structure into the returns that made Tom Dundon a billionaire.

Now those returns are being matched, and in some cases exceeded, by public money. Oregon taxpayers - including those same borrowers, those same former Santander Consumer customers now living in the state - will fund $365 million of the arena renovation. Portland's residents will contribute hundreds of millions more.

The money moves in one direction. The reputational benefits flow to Dundon. The public celebration of a new arena, a renovated team, a civic landmark - all of that attaches to his name. The $550 million settlement, the proof-of-income emails, the ongoing Exeter investigation - those are footnotes. Business journalism. Things that happened before the real story began.

That is how whitewashing works at scale. Not through deception, exactly - all of this is in the public record, findable by anyone who looks. Through the much simpler mechanism of attention. People follow the franchise. They follow the arena. They follow the games. The regulatory history of the man who owns the team is available but not interesting. Not until reporters find the emails and publish them. And by then, the money is already committed.

What Comes Next

The NBA's board of governors must still formally approve Dundon's purchase of the Trail Blazers. That process typically takes several months after a deal is agreed and involves a review of the prospective owner's financial and legal background. Whether the multistate investigations into Santander Consumer USA's legacy practices, or the ongoing Exeter Finance investigation, have been disclosed to and assessed by the NBA's review process is not publicly known.

The Exeter Finance investigation is live. Oregon's Department of Justice confirmed its participation. The investigation has been disclosed by Exeter in securities filings. Its resolution - settlement, charges, or clearance - will shape how much of the Dundon story is still unwritten.

Oregon Governor Kotek's office declined to answer whether knowledge of Dundon's regulatory history would affect her position on the arena deal. Her spokesperson pointed to public remarks she made in support of public funding for the Blazers after the legislature adjourned: "This is a great first step. We're going to get the best deal possible for Oregon."

It is not clear what Oregon got in exchange. The legislature approved $365 million. The city and county are contributing hundreds of millions more. What revenue sharing, what equity stake, what community benefit clauses, what protections for Oregon taxpayers if the franchise ultimately relocates - none of that was settled before the vote. State Senator Pham tried to win amendments requiring revenue sharing and private investment guarantees. She got six votes out of thirty.

Dundon is expected to be the Trail Blazers' owner in full as of March 31, 2026. The arena renovation will proceed. Portland will keep its team. The $870 million will flow.

The $550 million that 265,000 borrowers extracted from their paychecks to pay for Santander Consumer's profitable defaults - that already flowed. Some time ago. Into the fortune that made this deal possible.

The borrowers got an average of $245 each from the settlement. Oregon got a basketball team.

By the Numbers

- $4 billionDundon's bid for the Portland Trail Blazers

- $870 millionTotal public funding for arena renovation

- $365 millionOregon state legislature contribution

- $550 millionSantander Consumer USA settlement (2020)

- 265,000+Borrowers covered by the settlement in 33 states

- $245Average restitution per borrower from $65M restitution fund

- 28%Interest rate charged to AshLe' Penn by Exeter Finance

- 540Average credit score of Santander Consumer borrowers (below prime threshold)

Sources: ProPublica / Oregon Public Broadcasting joint investigation (March 25, 2026): "New Portland Trail Blazers Owner Played Key Role at Company Oregon Accused of Predatory Lending" and "Before Tom Dundon Agreed to Buy the Portland Trail Blazers, Oregon Accused the Company He Created of Predatory Lending." Internal Santander Consumer USA emails (2013), obtained via Oregon attorney general records request. Oregon multistate court complaint vs. Santander Consumer (2020). Exeter Finance securities filings (2025-2026). Consumer Financial Protection Bureau complaint database. SEC filings, Santander Consumer USA IPO prospectus (2014). Mark Williams, Boston University Questrom School of Business. Mark Jansen, University of Utah. Oregon AG Dan Rayfield statement (March 2026).

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram