Fannie Mae Backs Crypto Mortgages: Bitcoin Holders Can Now Buy Homes Without Selling

The $3.8 trillion Fannie Mae guarantee machine just updated its rules. Crypto holders are the beneficiaries. (Pexels)

The government-sponsored entity that backstops roughly a third of all American mortgages just told the market something it has been waiting a decade to hear: you can pledge your bitcoin to buy a house without liquidating it first. Fannie Mae is preparing to accept crypto-backed mortgages for the first time, via a product developed with digital mortgage lender Better Home & Finance and Coinbase, according to reporting from the Wall Street Journal on March 26, 2026.

This is not a niche fintech pilot. This is not a crypto bank doing one-off deals for high-net-worth clients. This is Fannie Mae - the entity Congress created to guarantee liquidity in American housing markets - formally blessing a new class of collateral. When Fannie updates its underwriting guidelines, lenders across the country follow. Credit unions in Ohio, community banks in Texas, mortgage originators in every zip code adjust their policies to match. That is how significant this decision is.

The deal reflects something broader happening across U.S. financial infrastructure: crypto is being integrated at the institutional level faster than retail markets have absorbed the last cycle's losses. The same week Fannie Mae cleared crypto mortgages, Visa became a Super Validator on the Canton Network alongside JPMorgan and Goldman Sachs. MARA Holdings restructured $1 billion of convertible debt using bitcoin proceeds. Coinbase-backed advocacy group Stand With Crypto is targeting six congressional battleground races ahead of the November midterms. The convergence of all these signals in a single week is not coincidental - it is the result of two years of regulatory clearing happening at once.

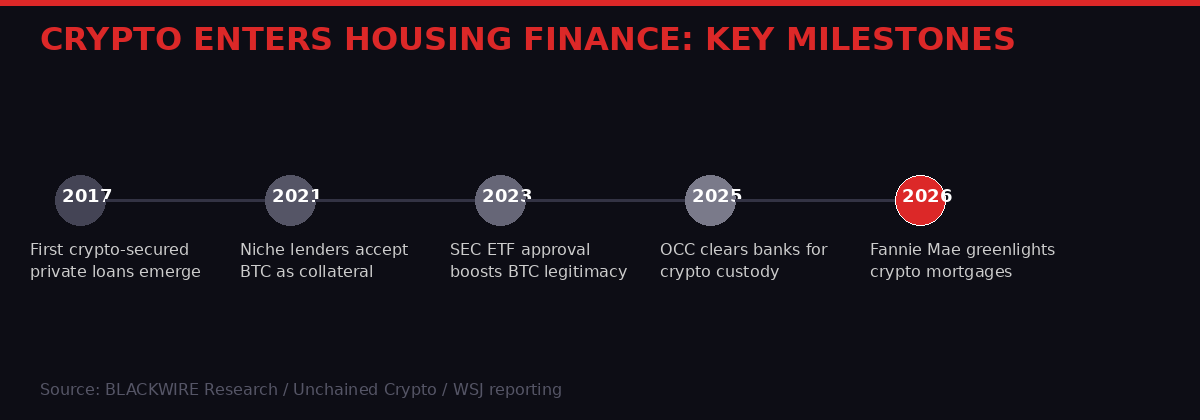

Crypto's path into housing finance - from niche private loans in 2017 to Fannie Mae's landmark 2026 clearance.

What Fannie Mae Actually Said - and What It Means

Fannie Mae's underwriting decisions ripple across every lender in America. (Pexels)

Fannie Mae has not published final guidelines yet. The Wall Street Journal's reporting, confirmed by Unchained Crypto, describes a product in development with Better Home & Finance and Coinbase that will let borrowers pledge crypto holdings as collateral when securing a Fannie-backed loan. The key departure from prior practice: borrowers will not need to liquidate their digital assets to fund a down payment. Instead, the holdings serve as collateral in a structure that keeps the borrower's crypto position intact.

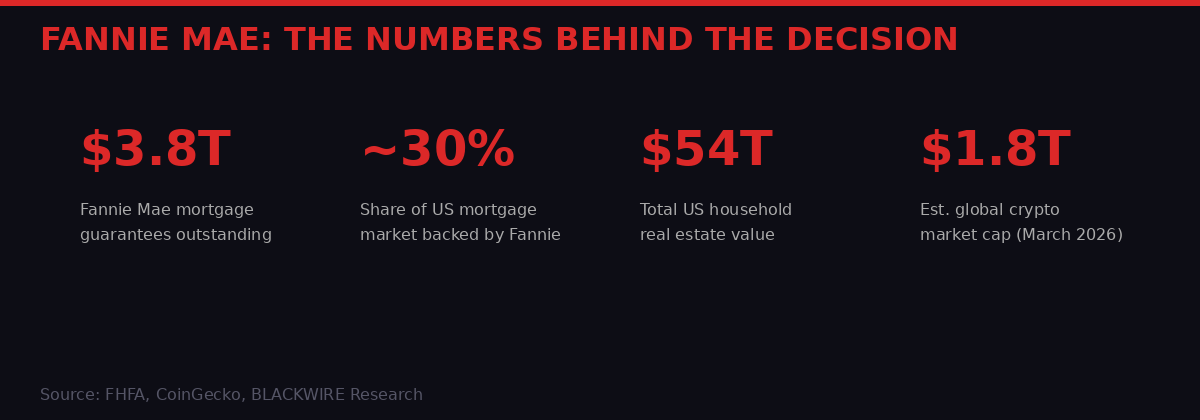

The significance of Fannie's involvement cannot be overstated. Fannie Mae does not originate mortgages - it buys them from lenders and packages them into mortgage-backed securities, providing the liquidity that allows originators to keep making new loans. Its underwriting standards function as the de facto rulebook for the American mortgage market. Private lenders like Ledn, BlockFi (pre-collapse), and Arch Lending have offered crypto-backed mortgage products for years, but without Fannie's backing they were confined to portfolio lending - carrying the loans on their own books with no secondary market. Fannie's clearance means these loans can now be securitized, meaning the market for them scales.

Better Home & Finance is the digital mortgage originator that went public via SPAC in 2023, having nearly collapsed twice amid executive drama and mass layoffs. CEO Vishal Garg's company has spent the past two years rebuilding its balance sheet and reputation, and this partnership with Coinbase positions it squarely at the intersection of the two markets it needs to win: tech-forward homebuyers and crypto-native wealth holders. For Coinbase, it is another step in the Prime Finance strategy - positioning Coinbase not just as an exchange but as the institutional custody layer for any use of digital assets in traditional finance.

The scale of Fannie Mae's reach makes its crypto policy shift a system-level event, not just a product launch.

The Mechanics: How Crypto-Backed Mortgages Actually Work

Pledging bitcoin without selling it - the core mechanics that make crypto mortgages structurally different from traditional loans. (Pexels)

The structural details matter enormously here, and they have not been fully disclosed. What is known from prior crypto mortgage products and the general architecture Coinbase would apply gives a framework for what borrowers will face.

In standard crypto-collateralized lending, the borrower deposits cryptocurrency into a custodied account - in this case almost certainly held with Coinbase Custody Trust Company, a federally chartered limited purpose trust. The lender applies a collateralization ratio, typically requiring borrowers to pledge 125-150% of the loan amount in crypto value. This accounts for price volatility - if the crypto collateral drops below a threshold, the borrower faces a margin call requiring either additional collateral or partial liquidation.

The volatility management problem is the central engineering challenge. Bitcoin's price has moved from $93,000 in January 2025 to under $69,000 in March 2026 before recovering toward $71,000. A borrower who pledged BTC at peak prices in late 2024 would have faced significant margin pressure in Q1 2026. The haircut structure - how much below market value the lender values the crypto collateral - is the risk dial that determines whether this product is usable for most borrowers or only for those with large, diversified digital asset positions.

"Many banks see the lack of privacy as a dealbreaker for moving meaningful activity on-chain." - Rubail Birwadker, Visa's global head of growth products (in the context of institutional blockchain adoption, Canton Network, March 25, 2026)

Custody is the second critical question. Where the crypto sits, who controls the keys, and what happens in a lender default scenario all affect the product's attractiveness. If Coinbase holds custody, borrowers are effectively trusting both their lender and Coinbase not to commingle, mis-manage, or lose access to assets. The 2022 BlockFi and Celsius failures demonstrated exactly how badly this can go when custody is sloppy and collateral is rehypothecated - used to fund the lender's own positions. The FDIC and OCC's March 2026 guidelines on tokenized securities signaled that regulators expect institutional-grade safeguards, but the devil is always in the implementation.

From a borrower's perspective, the appeal is clear. A crypto holder sitting on 20 BTC accumulated over a decade does not want to sell and trigger a massive capital gains event just to fund a $400,000 down payment. They would rather pledge the bitcoin, keep the position, and pay the mortgage from income. If BTC appreciates, they win on both sides. If it drops significantly, the margin call creates a stressful forced decision - but at least they maintained the position through the up-cycle.

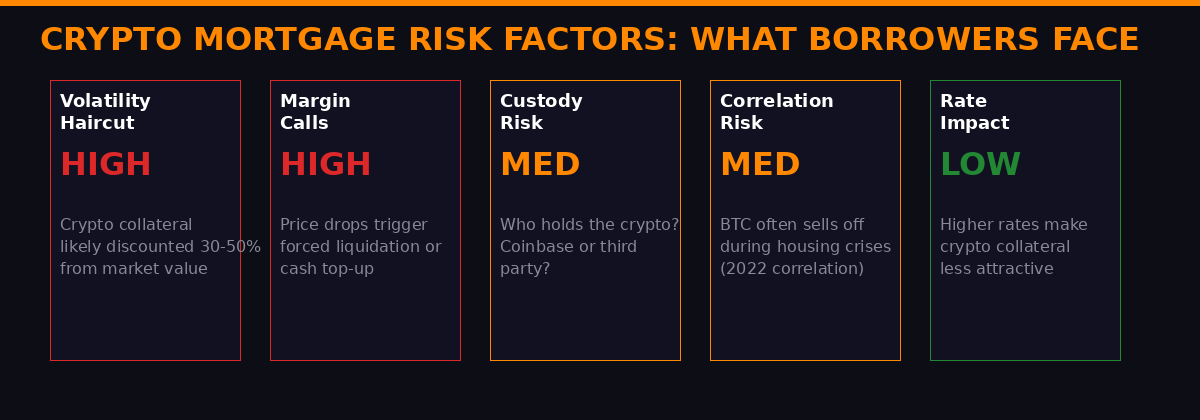

Five risk vectors every crypto mortgage borrower needs to model before pledging digital assets as home collateral.

MARA Holdings Dumps $1.1 Billion in BTC - and the Stock Jumps

MARA's disciplined debt restructure sent a message Wall Street has been waiting to hear from bitcoin miners. (Pexels)

The same day Fannie Mae made its crypto mortgage announcement, MARA Holdings - the largest publicly listed bitcoin mining company in the United States by hashrate - disclosed it had sold 15,133 BTC over a three-week window ending March 25, 2026. The proceeds: approximately $1.1 billion. The use of proceeds: buying back $1.0 billion in convertible senior notes at a 9% discount to face value, capturing an estimated $88.1 million in value from the spread.

The transaction cut MARA's convertible debt load by roughly 30%, from $3.3 billion to $2.3 billion outstanding. The company repurchased $367.5 million of notes due 2030 for $322.9 million, and retired $633.4 million of notes due 2031 for $589.9 million. After the sale, MARA retains 38,689 BTC - still one of the largest corporate bitcoin treasuries in existence, behind only MicroStrategy (now rebranded as Strategy) and Coinbase's own holdings.

CEO Fred Thiel was explicit that this was not a change in investment thesis. MARA still holds a massive BTC position. But it was a change in capital allocation philosophy - and the market responded accordingly. Shares jumped 10% in premarket trading. That response is significant: investors did not read the BTC sale as a bearish signal. They read it as financial discipline.

MARA Holdings Debt Restructure - Key Numbers

- BTC Sold: 15,133 bitcoin between approximately March 4-25, 2026

- Gross Proceeds: ~$1.1 billion

- 2030 Notes Retired: $367.5M face value, purchased for $322.9M

- 2031 Notes Retired: $633.4M face value, purchased for $589.9M

- Discount Capture: ~$88.1 million in value from buying below par

- Debt Reduction: $3.3B to $2.3B (-30%)

- BTC Remaining in Treasury: 38,689 BTC

- Stock Move: +10% premarket on announcement day

The contrast with Strategy's approach is instructive. Michael Saylor has pursued an unconstrained accumulation strategy - issuing equity and debt to buy more bitcoin, regardless of the balance sheet load. MARA under Thiel is experimenting with something more nuanced: treating the bitcoin treasury as an active tool for capital structure optimization, not just a passive accumulation bet. Selling BTC at a moment when it trades near $71,000 to retire debt at a discount is a classic risk-adjusted move. It reduces leverage precisely when markets are unsettled by oil prices and geopolitical noise around the Iran conflict.

The broader mining sector is watching. Marathon is not alone in carrying massive convertible debt loads - it was one of the dominant fundraising structures during 2024-2025 when mining companies issued billions in convertibles to fund expansion and bitcoin purchases. If BTC trades sideways or below conversion thresholds, those notes eventually need to be addressed. MARA's willingness to use its treasury to buy back debt at a discount sets a precedent the sector is likely to follow.

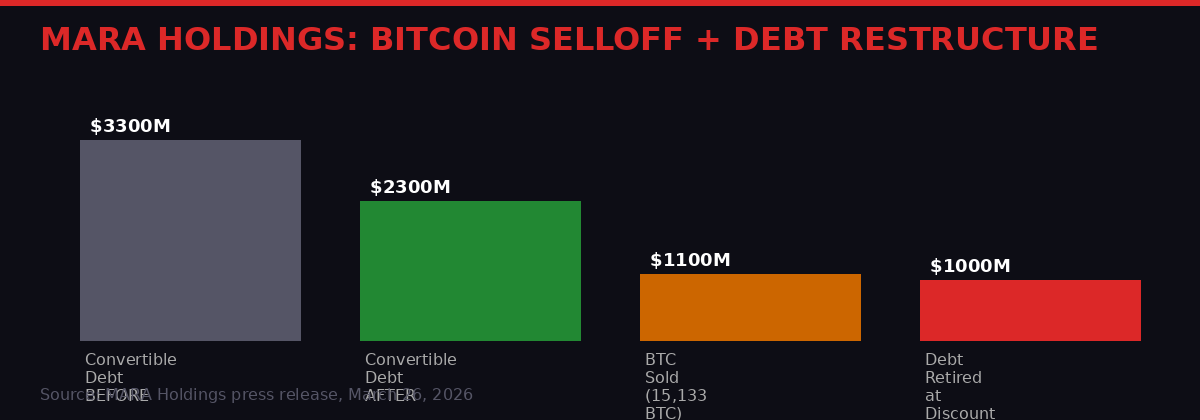

MARA used $1.1B in BTC proceeds to retire $1B face value of convertible notes at a 9% discount - $88M captured in a single trade.

Stand With Crypto Fires First Shot at the 2026 Midterms

Stand With Crypto's early bipartisan endorsements signal the crypto industry is playing a long game in 2026 congressional races. (Pexels)

Stand With Crypto - the Coinbase-backed political advocacy group that spent tens of millions in the 2024 election cycle - announced March 26 its first wave of endorsements for the 2026 midterm elections, targeting six battleground congressional races with a deliberately bipartisan slate of candidates.

The six endorsed candidates: Republicans Zach Nunn (Iowa), Mike Lawler (New York), and Rob Bresnahan (Pennsylvania); Democrats Don Davis (North Carolina), Susie Lee (Nevada), and Greg Landsman (Ohio). The selection is calculated. Nunn, Lawler, and Bresnahan are vulnerable incumbents in competitive districts. Davis, Lee, and Landsman represent the organization's argument that crypto has supporters across party lines that the industry needs to keep onside regardless of which party controls the House.

The stakes are outlined directly in the announcement. Kalshi prediction markets put the probability of Democrats flipping the House at over 84% as of late March 2026 - a scenario that would reshape the legislative environment crypto has been working to construct. The Digital Asset Market Clarity Act, stablecoin regulation, crypto tax reform, and the strategic bitcoin reserve legislation all assumed a crypto-friendly House majority. A Democratic flip does not automatically mean hostile legislation - the party has its own pro-crypto contingent - but it adds uncertainty.

"64% of crypto holders say they're enthusiastic about supporting pro-crypto candidates, and 59% say they don't always vote along party lines." - Impact Research polling released by Stand With Crypto, March 26, 2026

The polling number that matters most is the 59% who say they don't vote strictly along party lines. That is the classic swing-voter profile, and it is exactly what makes crypto voters potentially decisive in tight House races. A motivated, cross-partisan bloc of 52+ million Americans who own crypto - the estimate Coinbase has used publicly - is a constituency both parties need to court rather than antagonize.

Six battleground races, three Republicans, three Democrats - Stand With Crypto's bipartisan 2026 strategy laid out in full.

What is interesting about Stand With Crypto's early positioning is how much it echoes the 2024 strategy - except with higher stakes and clearer legislative targets. In 2024, the group was fighting to stop hostile regulators and protect the industry from enforcement-first oversight. In 2026, it is trying to ensure specific bills pass. The GENIUS Act stablecoin legislation, the DAMA market structure bill, and related frameworks are all queued in various states of Senate and House deliberation. The midterm lineup will determine whether the legislation that has been drafted over the past two years actually becomes law or gets shelved for another cycle.

Visa Joins the Institutional Blockchain Stack - Canton Network Super Validator

Visa's legal and compliance team formally approved the company's first blockchain governance role - the Canton Network Super Validator appointment. (Pexels)

The week's fourth significant institutional signal came from Visa on March 25. The payments giant was appointed as a Super Validator on the Canton Network - the privacy-enabled, permissionless Layer 1 blockchain built specifically for institutional use - with the highest Super Validator Weight of 10, three days after submitting its application. More significantly: it was the first time Visa's legal and compliance teams formally approved a blockchain governance proposal.

Canton's validator list reads like the guest list for a high-finance blockchain conference: DTCC, JPMorgan (deploying JPM Coin for near-instant settlement), Goldman Sachs, Citadel Securities, BNP Paribas, and Circle are among the 849 validators, 42 of which hold Super Validator status. DTCC plans to tokenize a subset of U.S. Treasury securities on Canton in H1 2026. The network processes more than $9 trillion in monthly volume.

Visa's entry is not about payment volume - the company already processes $14+ trillion annually through its own rails. It is about the stablecoin infrastructure Visa has been building. Visa's stablecoin settlement operations hit an annualized run rate of $4.6 billion, with stablecoin-linked card programs running across more than 130 programs in 50 countries. The Canton Super Validator role lets Visa help clients understand how onchain settlement on a permissioned institutional chain integrates with its existing stablecoin architecture.

The privacy angle is what makes Canton specifically attractive to institutions that have resisted Ethereum and Solana for core operations. On public blockchains, transaction data is visible. For a payments processor, a bank, or a securities firm, that is unacceptable - competitors, regulators, and adversarial actors would all be able to see transaction flows in real time. Canton uses cryptographic confidentiality guarantees at the protocol level, allowing institutions to settle assets onchain without exposing their books. Birwadker's comment - that privacy has been a dealbreaker for institutions on public chains - is the clearest statement of why Canton has attracted this specific roster of validators.

Canton Network - Current Scale (March 2026)

- Monthly Volume: $9+ trillion processed on-network

- Total Validators: 849

- Super Validators: 42

- Visa Super Validator Weight: 10 (maximum)

- Key Participants: DTCC, JPMorgan, Goldman Sachs, Citadel, BNP Paribas, Circle, Visa

- Upcoming: DTCC Treasury tokenization H1 2026

- Visa Stablecoin Run Rate: $4.6 billion annualized

What It All Adds Up To: The Institutional Integration Moment

Wall Street is not adopting crypto. It is building a parallel architecture where crypto rails become the default infrastructure. (Pexels)

Look at what happened in the seven days ending March 26, 2026. The Federal Reserve, FDIC, and OCC issued joint guidance telling banks how to handle tokenized securities. The SEC and CFTC published clearer enforcement frameworks for crypto. Fannie Mae cleared crypto-backed mortgages. Visa joined Canton as a Super Validator. MARA restructured $1 billion in debt using bitcoin proceeds. Morgan Stanley filed for ETF access to crypto. Stand With Crypto launched its midterm campaign targeting six House seats.

None of these are isolated events. They are the downstream consequences of a regulatory and legislative environment that shifted fundamentally in late 2024 - when the election handed Congress a pro-crypto majority and the SEC's hostile leadership was replaced. The pipeline that opened then is now delivering product: cleared frameworks, new financial products, institutional governance votes, and lobbying infrastructure for the next election cycle.

The Fannie Mae decision is the most symbolically powerful of the week's developments precisely because it touches ordinary Americans rather than institutional traders. A family with $200,000 in bitcoin accumulated over five years now has a path to homeownership that does not require liquidating the position and paying capital gains taxes. That is a real material change in financial access. Whether most borrowers should actually use this product - given the volatility and margin call risks - is a separate question. That they can is the point.

The bear case for all of this is concentration and correlation risk. The more crypto gets woven into traditional financial infrastructure - mortgages, ETFs, institutional reserves, payment networks - the more a major crypto price collapse looks like a systemic financial event rather than a contained market correction. 2022's $2 trillion wipeout hurt mostly retail investors and a cluster of overleveraged crypto firms. A 2027 or 2028 collapse that takes down crypto-collateralized mortgage pools, miners' balance sheets, and institutional stablecoin programs would look very different. The same integration that makes the ecosystem more legitimate also makes its failures more contagious.

Regulators know this. The OCC and Fed guidance from earlier this month was not a blank check - it was a framework with explicit risk management requirements. Fannie Mae's mortgage product will come with volatility haircuts, custody requirements, and probably limits on which digital assets can serve as collateral. The question is whether those guardrails are calibrated to the actual risks of a sector that can lose 30% of its value in six weeks.

What Comes Next: Legislative Timeline and Market Triggers

The next 90 days of crypto legislation will determine whether 2026's infrastructure push translates into permanent market architecture. (Pexels)

The legislative queue heading into summer 2026 is the most consequential in crypto's history. Three major pieces of legislation are in various stages of House and Senate action, and the midterm election looms as the hard deadline for the current congressional alignment.

First, the GENIUS Act stablecoin bill. Senate deliberations have been complicated by disagreements between the banking sector and crypto industry over oversight structure - specifically whether stablecoin issuers should be subject to the same capital and reserve requirements as banks. Senators reportedly reached a preliminary agreement in late March to resolve the main sticking points, per CNBC reporting, but the bill has not yet passed committee. Market structure legislation in the form of the Digital Asset Market Clarity Act faces similar dynamics in the House.

Second, the crypto tax treatment reform. The debate over whether crypto-to-crypto swaps should constitute taxable events - a question that affects millions of DeFi users who currently face massive theoretical tax liabilities from routine swaps between tokens - has been part of the legislative discussions but has not found a vehicle. Any legislative action here would be transformative for DeFi volume and adoption.

Third, the strategic bitcoin reserve. The executive order establishing a strategic BTC reserve using forfeited government assets was signed, but the mechanism for expanding it through Treasury purchases remains pending congressional authorization. The reserve's current size - approximately 190,000 BTC from forfeitures - could grow dramatically if Congress appropriates funds, but that step requires the same House majority Stand With Crypto is now trying to protect through its midterm campaign.

Against that legislative backdrop, the market is trading near a critical zone. Bitcoin near $71,000 is caught between the deflationary pressure of oil prices above $100 and the positive impulse of institutional adoption news. The Iran conflict's impact on oil - and oil's impact on inflation expectations and Fed policy - is the dominant macro variable. A Fed that cannot cut rates because oil keeps CPI elevated is a Fed that keeps the risk-off pressure on Bitcoin's correlation with equities. The institutional news flow this week is bullish. The macro backdrop is neutral to bearish. The tension between those two forces is exactly where Bitcoin has been trading for the past month.

VOLT Watchlist: Key Dates and Triggers (April-June 2026)

- GENIUS Act Stablecoin Vote: Senate committee markup expected Q2 2026

- Fannie Mae Final Guidelines: Watch for Federal Housing Finance Agency publication

- Fed Rate Decision: May 6-7 FOMC - inflation data will determine crypto/equities move

- MARA Q1 Earnings: First full-quarter report with new balance sheet structure

- Canton DTCC Treasury Tokenization: First half 2026 - watch for launch date announcement

- Stand With Crypto Fundraising Deadline: Q2 campaign finance filing will show crypto PAC power

- Bitcoin Halving Anniversary: April 2026 marks one year since the fourth halving - miner economics shift

The Fannie Mae story is the hinge. It is the moment when crypto stopped being an alternative asset class for people who opted out of traditional finance and started being embedded in the infrastructure of traditional finance itself. You can now borrow against your bitcoin to buy a house. You can now settle Treasuries on a blockchain with Visa's governance blessing. You can now buy a spot ETF through your brokerage account. The product is mainstream. Whether the risk management around it is mature enough is the next question - and the answer to that will not come in a press release. It will come the next time the market breaks and we find out what happens to crypto mortgage pools when BTC drops 40% in a month.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram