The Federal Bureau of Investigation built its own cryptocurrency tokens. Not to trade them. Not to profit from them. To catch the people who fake the market.

On Monday, three men walked into an Oakland federal courtroom - two of them CEOs - after being extradited from Singapore to face charges of orchestrating one of the most systematic crypto manipulation schemes ever prosecuted in the United States. They are the latest additions to a growing roster of ten foreign nationals from four countries indicted over the past year, all connected to four market-making firms that prosecutors say ran coordinated wash trading and pump-and-dump operations across multiple exchanges.

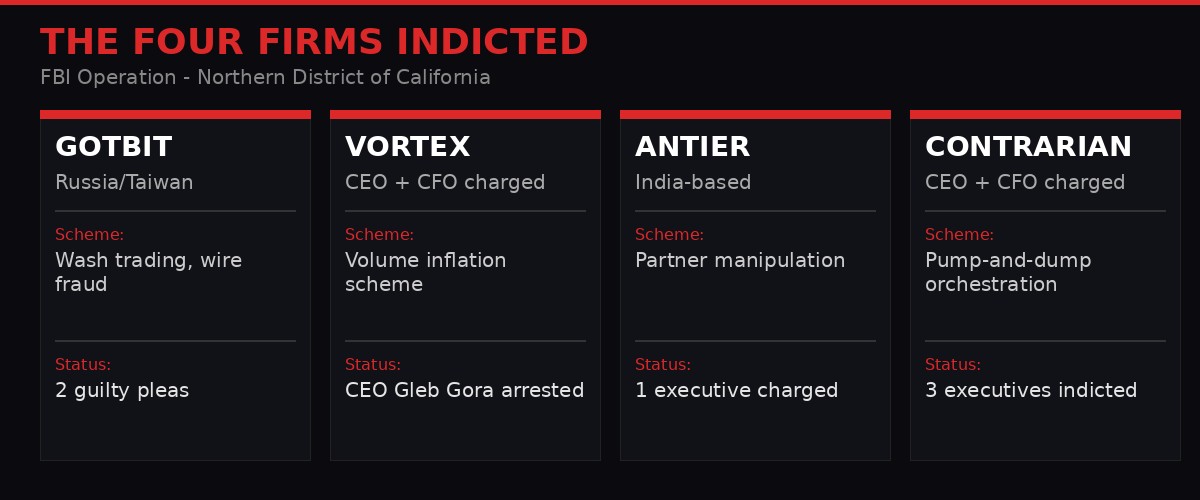

The firms - Gotbit, Vortex, Antier, and Contrarian - are accused of acting as both buyer and seller on the same tokens simultaneously, manufacturing fake volume that lured retail investors into purchasing inflated assets. When prices hit target levels, insiders dumped. The investors were left holding worthless bags. The indictments, filed in the Northern District of California, carry maximum penalties of 20 years in federal prison for each defendant.

It is the largest coordinated enforcement action against crypto market-making firms in DOJ history. And it arrived on the first day of Q2 2026 - a quarter that opens with Bitcoin at $68,680 after its worst first quarter since 2018, the Fear and Greed Index stuck at 8 out of 100, and a market that just watched $900 billion in total capitalization evaporate over 90 days.

The FBI's Undercover Token Factory

The investigation began in 2024, when the FBI and IRS Criminal Investigation division launched a joint probe into suspicious trading patterns flagged across multiple centralized exchanges. But instead of simply monitoring existing tokens, agents took an unprecedented step: they created their own cryptocurrencies and approached market-making firms to provide "liquidity services."

This was not entrapment. This was engineering a controlled test. By creating tokens with known supply, known holders, and zero organic demand, federal agents could precisely measure how much artificial volume each firm generated. Every trade was logged. Every communication recorded. The trap was set in plain sight.

According to the indictment documents filed in the Northern District of California, the undercover operation revealed a consistent playbook across all four firms. Market makers would create clusters of coordinated accounts on target exchanges. These accounts would execute simultaneous buy and sell orders on the same token - sometimes within the same second - creating the illusion of active trading. Volume charts would spike. Price tickers would turn green. Social media bots, in some cases operated by the same firms, would amplify the appearance of organic interest.

"They not only conspired to inflate the trading volume and price of cryptocurrencies, but also profited through the sale of the cryptocurrencies at inflated prices to unwitting investors." - U.S. Attorney's Office, Northern District of California

The scheme's elegance was in its simplicity. Wash trading requires no technical exploit, no smart contract vulnerability, no zero-day. It requires only coordination and a willingness to lie about what the numbers represent. In traditional finance, wash trading has been illegal since the Commodity Exchange Act of 1936. In crypto, it operated for years as a gray-area service - market makers advertised "volume enhancement" packages openly on Telegram and Discord, with pricing tiers based on the level of fake activity desired.

The FBI's operation changed the calculus. By becoming a client, the Bureau documented the full lifecycle of manipulation from initial pitch to final dump. Prosecutors now have recordings, transaction logs, and communications showing executives explicitly discussing how to evade detection systems on exchanges.

The Defendants: CEOs, CFOs, and a Cross-Border Network

The indicted individuals span four countries and three continents. None are U.S. citizens. All operated in the global crypto market-making industry, which exists in a regulatory no-man's land between traditional financial oversight and the decentralized ethos of cryptocurrency.

Gotbit was the first firm to fall. In March 2025, a federal grand jury indicted three Gotbit employees: Antoine Tsao, a Taiwanese national serving as business development manager; Nemanja Popov, a Serbian national working as account manager; and Ian Sofronov, a Russian national and sales manager. Tsao and Popov have since pleaded guilty to conspiracy to commit wire fraud, according to court records. Sofronov's case remains unresolved. Prosecutors allege Gotbit "conducted wash trades involving millions of dollars and received tens of millions in proceeds," making it the most financially significant operation among the four firms.

Vortex saw its entire leadership structure dismantled. CEO Gleb Gora, CFO Sergei Ryzhkov, and business development manager Michael Vogel were all indicted between August and September 2025. Gora was among the three defendants extradited from Singapore who appeared in the Oakland courtroom on March 31, 2026. The Vortex indictment alleges the firm operated coordinated trading desks that could generate artificial volume across dozens of tokens simultaneously.

Contrarian faced a similar sweep. CEO Manu Singh, CFO Kushagra Srivastava, and business development associate Vasu Sharma were all charged. The firm allegedly partnered with Antier Solutions Private Limited, an India-based blockchain services company, to scale their manipulation operations. Antier's business development manager, Sabby Singh, was separately indicted.

All ten defendants face charges of wire fraud and conspiracy to commit wire fraud. Each count carries a maximum sentence of 20 years in federal prison. Federal investigators have seized over $1 million in cryptocurrency assets linked to the scheme, though prosecutors suggest the actual proceeds were substantially higher.

The geographic diversity of the defendants - Taiwan, Russia, Serbia, India, with arrests in Singapore - illustrates the challenge of enforcing securities law in a market designed to be borderless. It also shows the DOJ's growing willingness and capability to pursue cross-jurisdictional cases. The Singapore extraditions required bilateral cooperation under mutual legal assistance treaties, a process that typically takes months.

The Wash Trading Economy: How Big Is It Really?

This case is a drop in a very deep ocean.

The National Bureau of Economic Research published a study in 2022 estimating that 70% of reported trading volume on unregulated crypto exchanges was fake. Bitwise Asset Management's 2019 report to the SEC found that 95% of Bitcoin trading volume on CoinMarketCap was artificial. While the situation has improved on regulated exchanges that now deploy surveillance tools, the problem persists on mid-tier and smaller platforms where most retail traders in emerging markets operate.

Wash trading in crypto works differently from traditional markets because the infrastructure makes it trivially easy. Creating exchange accounts - even multiple accounts - requires minimal KYC on many platforms. API access allows algorithmic execution of thousands of trades per minute. And unlike traditional stock exchanges, where the Consolidated Tape Associates track every transaction through a unified reporting system, crypto exchanges self-report their own volume numbers with no external verification.

This creates a perverse incentive. Exchanges benefit from reporting high volume because it attracts traders, which generates fees. Market makers benefit from generating high volume because it's literally what they're paid to do. Token projects benefit from high volume because it signals legitimacy to investors. The only loser is the retail trader who believes the numbers are real.

Research firm Kaiko estimates that across the top 100 crypto exchanges by reported volume, the gap between genuine and reported activity ranges from 30% to 90% depending on the platform. The most egregious offenders tend to be exchanges headquartered in jurisdictions with minimal regulatory oversight - though the Gotbit case demonstrates that firms based in regulated countries can and do provide these services globally.

The economics of the wash trading industry are surprisingly transparent. In Telegram groups and broker forums, market-making firms have historically advertised "volume packages" starting at $5,000 per month for small-cap tokens, scaling to $50,000-$100,000 per month for projects that want to appear on the top volume lists of major exchanges. Premium services include coordinated social media campaigns, exchange listing facilitation, and what one firm described as "organic-looking accumulation patterns" - sophisticated algorithmic trading designed to mimic genuine investor behavior on charts.

The FBI's undercover operation captured these conversations in real-time. According to prosecutors, the defendants discussed specific strategies for evading exchange surveillance systems, including randomizing trade sizes, varying timing intervals, and distributing wash trading across multiple account clusters to avoid triggering automated alerts.

Q1 2026: The Backdrop of Blood

These indictments arrive at a moment of maximum fragility for crypto markets.

Bitcoin closed Q1 2026 at roughly $67,800 - a 22% decline from its January open of $87,508. That makes it the worst first-quarter performance since Q1 2018, when BTC cratered 49.7% in the aftermath of the ICO bubble. From its all-time high of $126,000, Bitcoin has now dropped approximately 45%. The total crypto market cap sits at $2.42 trillion, down from a cycle high near $3.15 trillion, representing roughly $900 billion in destroyed value over three months.

Ethereum fared even worse. ETH closed Q1 at $2,070, a 32.8% quarterly loss that represents its steepest first-quarter decline in years. The ETH/BTC ratio has compressed to multi-year lows. Spot Ether ETFs posted $769 million in net outflows for the quarter - three consecutive months of negative flows.

On the Bitcoin ETF side, the picture is mixed but net negative. Spot Bitcoin ETFs posted $496.5 million in net outflows for Q1, with $1.8 billion leaving in January and February before a March reversal brought $2.5 billion back in. The late-quarter inflows suggest institutional accumulation at depressed prices - a pattern consistent with whales buying what retail is selling.

The Fear and Greed Index tells the psychological story. At 8 out of 100 on April 1, the index has been lodged in "Extreme Fear" territory for 59 consecutive days - the longest streak since the FTX collapse in November 2022. Historically, readings below 15 have preceded positive 30-day returns in roughly 78% of instances since 2020, with median gains of 12.4%. But the FTX bottom came only after an additional 30% drawdown from the initial fear spike, so extreme fear alone is not a reliable entry signal.

Derivatives data reinforces the bearish positioning. Perpetual funding rates across every major asset on Binance are negative, meaning short sellers are paying to maintain positions. Solana's funding rate of -0.0138% stands out as particularly aggressive. Total 24-hour liquidations hit $98.3 million, with 66.4% coming from longs - traders trying to catch a bottom and getting burned.

The macro picture adds fuel to the fire. Trump's "Liberation Day" tariff package targeting over 50 nations takes effect on April 2. The Federal Reserve has pushed back rate-cut expectations. The S&P 500 posted five consecutive weekly losses. Oil prices have surged amid the ongoing Iran conflict. A record $13.5 billion derivatives expiry on March 27 created enormous selling pressure. And 50,000 BTC of miner capitulation sell pressure hit the market in Q1 alone, as global electricity prices rose 15% and mining operations ran out of runway.

Into this environment, the DOJ drops a message: the market you're trading may not be what it appears. The volume you're watching may not be real. The liquidity you're relying on may vanish the moment insiders decide to pull the plug.

The Regulatory Squeeze: SEC, CFTC, and the New Token Taxonomy

The wash trading crackdown does not exist in isolation. It is one piece of a broader regulatory offensive that accelerated dramatically in March 2026.

On March 17, the SEC and CFTC issued a joint interpretive release establishing a five-category token taxonomy - the first formal framework defining which digital assets fall under securities law and which qualify as commodities. The release identified 16 specific tokens as "digital commodities" under CFTC jurisdiction, while creating clear criteria for classifying future tokens. The SEC simultaneously declared that "most crypto assets are not securities," a 180-degree turn from the enforcement-by-litigation approach that defined the Gensler era.

This taxonomy matters for the wash trading case because it clarifies jurisdiction. If a token is classified as a commodity, the CFTC has enforcement authority. If it's a security, the SEC takes the lead. If it's neither - a utility token, for example - enforcement falls to the DOJ under general fraud statutes. The Gotbit/Vortex indictments were filed under wire fraud statutes, suggesting prosecutors are not waiting for regulatory classification debates to conclude before acting.

On March 31, the CFTC permanently banned KuCoin from serving U.S. users after a federal court entered a consent order. Binance launched oil perpetuals contracts on the same day, signaling that regulated derivatives products are expanding even as enforcement tightens on unregulated activity. Kraken received a Federal Reserve master account - the first crypto exchange to gain direct access to the central banking system.

Congress is pushing legislation on two fronts. The GENIUS Act, a bipartisan stablecoin regulation bill, is expected to reach the Senate floor in the second half of April, though a fight over stablecoin yield provisions has created friction between crypto advocates and traditional banking lobbyists. The CLARITY Act, which would formalize the SEC-CFTC jurisdictional split, advanced through committee with bipartisan support. And the PARITY Act proposed a stablecoin tax exemption for small transactions while closing the crypto wash sale loophole - a move that would eliminate a popular tax-loss harvesting strategy used by traders.

The combined effect is a market entering Q2 with more regulatory clarity than it has ever had - and more enforcement action than it has ever faced. The old playbook of operating in the gaps between agencies is closing. The wash trading indictments are the sharpest demonstration yet that the DOJ will use traditional fraud statutes to prosecute crypto manipulation regardless of whether the underlying asset is a security, commodity, or neither.

The Hack Economy: $501 Million Stolen in Q1 Alone

While prosecutors chase market manipulators, the theft economy continues to bleed the industry dry.

CertiK's March 2026 security report confirmed $59.5 million lost to exploits, phishing, and scams in the month alone, with a recovery rate of just 0.04% - $21,912 clawed back out of nearly $60 million stolen. For Q1 2026 as a whole, CertiK tracked $501 million in initial losses across 145 incidents. PeckShield's parallel analysis found $52 million in March hack losses across 20 separate incidents, nearly double February's $26.5 million.

The largest single incident was the Resolv Labs exploit, which accounted for 66% of March's total damage. An attacker exploited a vulnerability in Resolv's AWS KMS integration to execute an 80 million USR "infinite mint," draining $25 million directly. The minted tokens then crashed 80%, creating cascading bad debt across MorphoBlue, Euler, and Fluid - a phenomenon PeckShield has labeled "shadow contagion," where a single exploit triggers losses across interconnected DeFi protocols.

Wallet compromises led all categories at $26.8 million, followed by phishing scams at $21.4 million. Together, these two attack vectors accounted for more than 80% of monthly losses. Social engineering attacks surged in sophistication, with the largest single-victim loss being an $18.2 million theft from a Kraken user and a $24 million coordinated attack on the wallet known as "Sillytuna."

The Uranium Finance case adds historical context. U.S. prosecutors this week secured a critical indictment against the hacker behind a $54 million DeFi exploit on Binance Smart Chain from April 2021. The defendant, identified as Spalletta, allegedly told an associate: "Crypto is all fake internet money anyway." He faces charges after prosecutors traced laundered funds through Tornado Cash - demonstrating that even mixer services cannot guarantee anonymity against determined federal investigators.

Chainalysis reported that 2025 saw illicit crypto addresses receive at least $154 billion - a 162% increase from the prior year. Sanctioned entities drove a 694% increase in illicit flows. Stablecoins accounted for 84% of this activity. The numbers suggest that despite billions spent on security audits, bug bounties, and compliance infrastructure, the crypto industry remains structurally vulnerable to both technical exploits and social engineering at massive scale.

The connection to the wash trading case is more than thematic. Both the manipulation and the hacking represent market structure failures that erode investor confidence. When retail traders cannot trust that the volume they see is real, and cannot trust that the protocols they use are secure, the rational response is to leave. The Fear and Greed Index at 8 is the market's way of saying: trust has left the building.

What Happens Next: The Market Enters Q2 Under Siege

The immediate question is whether additional indictments are coming. The DOJ's announcement specifically references "ongoing prosecution" for several defendants, and the use of undercover operations suggests the Bureau has evidence against firms beyond the four named. Market-making is a competitive industry, and Gotbit, Vortex, Antier, and Contrarian are far from the only players offering volume enhancement services.

For the crypto market itself, the wash trading crackdown creates a paradox. In the short term, it's another negative headline in a market drowning in them. It reinforces the narrative that crypto markets are manipulated, which could accelerate retail outflows and deepen the fear cycle. CoinGlass data shows 24-hour liquidations at $98.3 million, with longs accounting for two-thirds of the damage.

In the medium term, however, the crackdown is constructive. Eliminating fake volume forces exchanges to compete on genuine metrics - real users, real trades, real liquidity. It protects the retail investors who remain in the market from unknowingly buying into manufactured demand. And it establishes precedent that manipulation in crypto markets will be prosecuted with the same severity as manipulation in equities or commodities.

The timing is significant. With the SEC-CFTC token taxonomy now established, with the GENIUS and CLARITY Acts advancing through Congress, and with Kraken holding a Federal Reserve master account, crypto's integration into the regulated financial system is accelerating. Wash trading prosecutions clean the house before institutional capital fully arrives. Blackrock, Fidelity, and the other ETF sponsors need to assure their clients that the markets underlying their products are not fabricated. This crackdown gives them that ammunition.

On the technical side, Bitcoin is trading at $68,680 with a 2.88% daily gain, having reclaimed the 21-day EMA for the first time in 11 sessions. Exchange netflows show 8,400 BTC withdrawn in the past 24 hours - the largest single-day outflow in three weeks. Addresses holding 100-1,000 BTC increased positions by 2.3%. Whale wallets accumulated 270,000 BTC over the past 30 days - the largest monthly accumulation in 13 years. Smart money is buying what everyone else is selling.

Ethereum's 4.82% daily gain outpaces Bitcoin by 194 basis points, with L2 total value locked rising 8.3% week-over-week to $47.2 billion. Base network daily transactions hit 6.2 million, up 34%. ETH staking deposits are the highest since mid-March. The ecosystem is building even as the price chart bleeds.

But the macro calendar looms. Trump's April 2 tariff package could trigger another round of risk-off selling. Powell's next speech is being watched for any signal on rate cuts. The Iran conflict continues to push oil prices higher. And the derivatives market, with negative funding rates across every major asset, is positioned for more pain before relief.

The Bigger Picture: Trust as the Scarcest Asset

Step back from the individual defendants and the specific firms, and the wash trading case reveals something fundamental about where crypto stands in April 2026.

This is an industry that grew up fast and messy. Market-making in traditional finance is a heavily regulated profession with strict compliance requirements, audit trails, and surveillance systems. Market-making in crypto was, until very recently, a Telegram DM away. Firms openly advertised their ability to fake whatever metrics a project needed - volume, holder counts, social sentiment - and the projects paid gladly because inflated numbers attracted investors who could not tell the difference.

The retail investor was always the exit liquidity. The wash trading scheme documented in the Gotbit indictments is just the formalized, prosecutable version of a dynamic that pervades the industry. When a new token launches with suspiciously high volume and a chart that only goes up, someone is paying for that chart. And the person buying in at the top is paying the ultimate price.

The FBI's decision to create its own tokens was a statement of strategic intent. The Bureau is not waiting for victims to come forward. It is proactively infiltrating the infrastructure of manipulation, documenting the mechanics, and building cases that can withstand federal trial standards. The fact that two defendants have already pleaded guilty suggests the evidence is overwhelming.

For the industry, the message is clear: the era of consequence-free market manipulation in crypto is over. The DOJ has the tools, the international cooperation frameworks, and the willingness to prosecute across borders. The SEC and CFTC have established the classification framework that determines jurisdiction. Congress is writing the laws that will formalize these standards. And the exchanges themselves - at least the regulated ones - are deploying increasingly sophisticated surveillance tools to detect wash trading in real time.

None of this will eliminate manipulation entirely. Where there is money, there will be fraud. But the cost of getting caught just went up dramatically. Twenty years in federal prison concentrates the mind in ways that a Telegram warning message does not.

Bitcoin at $68,680. Fear and Greed at 8. Fifty-nine consecutive days of extreme fear. $900 billion in market cap destroyed in Q1. $501 million stolen by hackers. And now, ten executives facing prison for manufacturing the volume that made it all look more legitimate than it was.

Q2 2026 opens with blood on the floor, handcuffs on the manipulators, and smart money quietly loading the truck.

The market doesn't need more confidence. It needs more convictions.

Sources: U.S. Department of Justice, Northern District of California (March 31 / April 1, 2026); Mercury News (March 31, 2026); FinanceFeeds (April 1, 2026); CertiK Security Report (March 2026); PeckShield Alert (April 1, 2026); Blockchain Magazine (April 1, 2026); Spoted Crypto Q1 Analysis; CoinGlass; Kaiko Research; Chainalysis 2026 Crypto Crime Report; Bitbo.io; Phemex Q1 Report Card.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram