Tokyo's 200ms Edge: How Crypto's "Decentralized" Exchanges Run on One AWS Region and the Latency Arms Race That's Coming for DeFi

Glassnode research exposes the geographic advantage baked into Hyperliquid's infrastructure. All 24 validators cluster in AWS Tokyo. European traders face a 200-millisecond handicap on every order. The latency war that consumed Wall Street just arrived in decentralized finance.

The infrastructure behind "decentralized" finance often lives in a single cloud region. (Pexels)

Two milliseconds versus two hundred. That is the gap between a trading desk in Tokyo and one in Frankfurt on Hyperliquid, the decentralized perpetual futures exchange that now handles more than $4 billion in daily volume. One trader's order reaches the validators in the time it takes a neuron to fire. The other's arrives after the market has already moved.

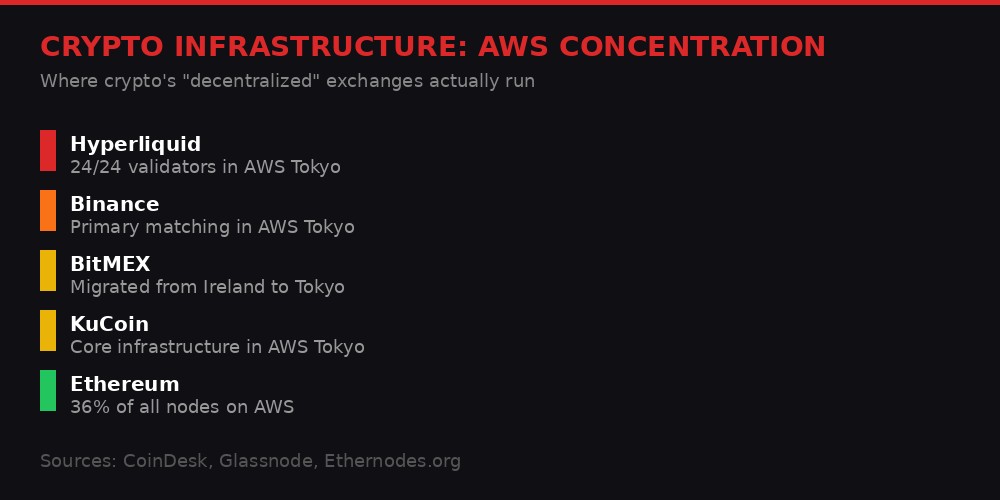

New research published March 30 by Glassnode - the blockchain analytics firm that tracks everything from on-chain flows to validator topology - lays bare a structural advantage that crypto's fastest-growing derivatives platform has never publicly addressed. Hyperliquid's entire validator set, all 24 nodes, runs in Amazon Web Services' ap-northeast-1 region. That is Tokyo. One city. One cloud provider. One set of data centers clustered across a few availability zones in eastern Japan.

The platform processes perpetual futures on Bitcoin, Ethereum, Solana, and dozens of altcoins. It has attracted institutional flow, sophisticated market makers, and a growing retail base. It is, by most definitions, decentralized: open access, no KYC gate, permissionless listing, transparent order books. But its physical infrastructure tells a different story. And that story has implications not just for Hyperliquid, but for every protocol that claims decentralization while running on centralized cloud rails.

Round-trip latency varies by up to 300ms depending on trader location. (BLACKWIRE/Glassnode)

The Numbers Behind the Edge

In time-ordered systems, milliseconds determine who gets filled first. (Pexels)

Glassnode's Hyperlatency tool, which launched alongside the research, measures order-to-fill round-trip times from multiple AWS regions. The results quantify what many high-frequency traders already suspected but could not prove with public data.

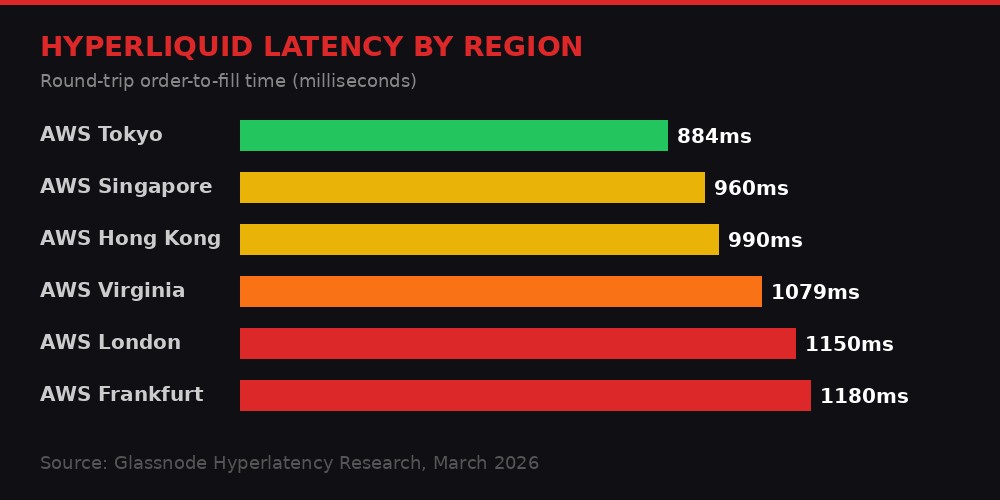

From AWS Tokyo, the median round-trip to place and confirm an order is 884 milliseconds. Of that, roughly 879 milliseconds is server-side processing - the matching engine doing its work. Just 5 milliseconds is network transit. The order essentially arrives at the validators' door instantaneously.

From Ashburn, Virginia - the AWS region that serves most of the U.S. East Coast's financial infrastructure - the total rises to roughly 1,079 milliseconds. The extra 195 milliseconds is almost entirely network transit. The matching engine processes at the same speed regardless of origin, but the order from Virginia arrives later, sits in the queue behind Tokyo-based orders, and gets filled after them.

From European locations like London and Frankfurt, the gap widens further. Glassnode's data shows round-trip times exceeding 1,100 milliseconds, with some measurements pushing past 1,200 milliseconds during high-activity periods. That is a 200 to 300 millisecond disadvantage on every single trade.

These numbers might sound small. They are not. On a platform handling $4 billion in daily perpetuals volume, 200 milliseconds is an eternity. It means a Tokyo-based desk can see a price move, submit an order, and receive a fill confirmation before a European competitor's order even reaches the validator. In a time-ordered matching system, that translates directly to better queue position, tighter spreads, and higher fill probability.

Key Latency Numbers

Tokyo: 884ms median round-trip (5ms network, 879ms processing)

Virginia: 1,079ms median round-trip (200ms network, 879ms processing)

Europe: 1,100-1,200ms median round-trip (220-320ms network, 879ms processing)

Gap: 200ms+ advantage for Tokyo-based traders on every order

Daily volume at stake: $4 billion+ in perpetual futures

One critic on X, posting under the handle @Algoquanttrade, noted that more complex order instructions from the Tokyo region can push round-trip latency to 400 milliseconds. That is a valid caveat. But even at 400 milliseconds from Tokyo versus 1,100 from London, the structural advantage remains massive. The gap compresses for simple orders and widens for complex ones, but it never closes.

Why Tokyo Became Crypto's Mahwah

Tokyo's role as crypto's infrastructure capital predates Hyperliquid by years. (Pexels)

The concentration of crypto infrastructure in Tokyo did not happen by accident. It is the product of a decade of regulatory evolution, geographic positioning, and the simple economics of where trading flow originates.

Japan was ground zero for cryptocurrency. Mt. Gox, the exchange that handled 70% of all Bitcoin transactions before its spectacular 2014 collapse, ran from Tokyo. The disaster could have killed Japanese crypto. Instead, it produced the world's first comprehensive cryptocurrency regulatory framework. Japan's Financial Services Agency (FSA) built a licensing regime that was stringent enough to satisfy institutional requirements but clear enough to attract serious operators.

That framework took years to produce results, but by 2024 it had created what Konstantin Richter, CEO of Blockdaemon, described at Token2049 in Singapore as an infrastructure environment "that's institutionally scalable and about ready to pop." The regulatory clarity attracted not just exchanges but the entire backend ecosystem - custodians, market makers, data providers, and the cloud infrastructure that serves them.

AWS ap-northeast-1 became the default because the trading flow demanded it. Asia generates a disproportionate share of global crypto volume. During peak hours, which align with Asian business hours, exchange order books are deepest and spreads are tightest. Market makers who need to hedge across multiple venues - Binance, BitMEX, KuCoin, Hyperliquid, and dozens of smaller platforms - want their infrastructure as close to the matching engines as possible. When one major exchange deploys in Tokyo, it creates gravitational pull for the others.

The "decentralized" financial system's uncomfortable dependency on one cloud region. (BLACKWIRE)

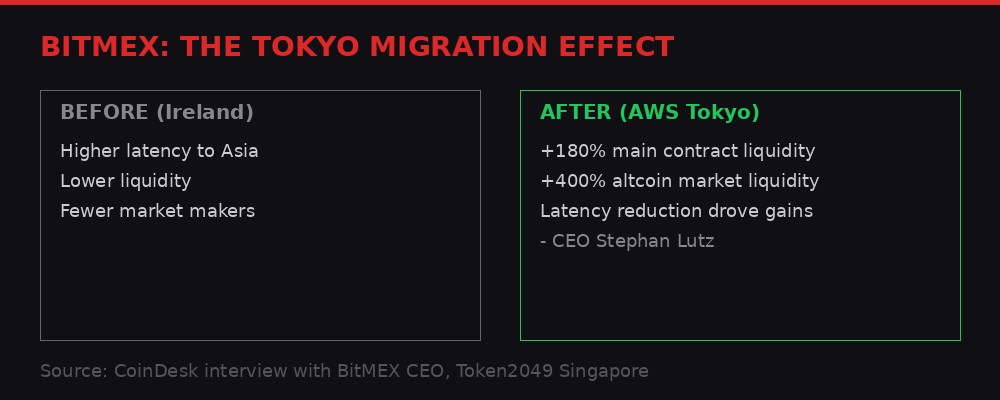

Binance, the world's largest centralized exchange by volume, runs significant infrastructure on AWS ap-northeast-1. KuCoin operates its core systems in the same region. And BitMEX's migration story is perhaps the most telling.

BitMEX CEO Stephan Lutz was blunt about the decision. "We were in Ireland before," he told CoinDesk at Token2049, "but it became more and more difficult because basically everyone except the U.S. players are in the Tokyo data centers." The switch from Ireland to Tokyo boosted liquidity by roughly 180% in BitMEX's main contracts and up to 400% in some altcoin markets. Lutz attributed the gains entirely to the latency reduction - not to marketing, not to market-maker recruitment, not to fee changes. Just proximity.

That is a remarkable admission. A major exchange doubled its effective liquidity simply by moving closer to where the other exchanges were running. The lesson was not lost on newer platforms. When Hyperliquid launched its validator network, there was never a serious discussion about geographic distribution. The validators went to Tokyo because that is where the matching engines needed to be.

The Wall Street Precedent: Decades of Fairness Engineering

Traditional finance spent decades building speed equalization. Crypto has done nothing. (Pexels)

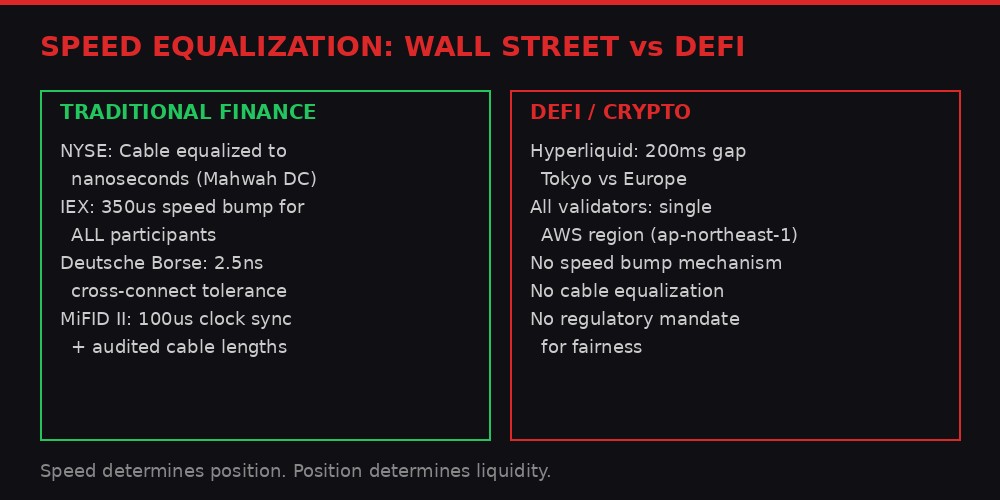

Traditional finance encountered this exact problem decades ago. The response was systematic and, eventually, regulatory. Crypto has inherited the problem without inheriting any of the solutions.

The New York Stock Exchange's Mahwah data center in New Jersey is the most famous example. NYSE uses optical backscatter reflectometry to equalize cable lengths between co-located servers and the matching engine. Every firm gets the same physical distance, measured to the nanosecond. The playing field is not level because of good intentions. It is level because the exchange operator engineered it that way, and regulators required it.

Deutsche Borse in Frankfurt normalizes cross-connects to within 2.5 nanoseconds. That is not a typo. Not 2.5 milliseconds - 2.5 billionths of a second. The precision required to achieve that level of fairness is extraordinary, and it reflects the seriousness with which European regulators treat market microstructure.

IEX, the exchange founded by Brad Katsuyama and made famous by Michael Lewis's "Flash Boys," took a different approach. Rather than equalizing cable lengths, IEX routes every order through a 350-microsecond speed bump - 38 miles of coiled fiber optic cable that introduces an artificial delay. The idea is simple: if you slow everyone down by the same amount, proximity advantage disappears. The speed bump does not eliminate high-frequency trading. It eliminates the advantage of being physically closer to the matching engine.

Wall Street built fairness into infrastructure over decades. DeFi has no equivalent mechanism. (BLACKWIRE)

Europe's MiFID II directive, the regulatory framework governing financial markets across the European Union, mandates clock synchronization to 100 microseconds and requires externally audited cable-length equalization. These are not suggestions. They are legal requirements, enforced with fines and trading suspensions.

Nothing equivalent exists in decentralized markets. There is no regulatory mandate for geographic distribution of validators. There is no speed bump mechanism. There is no cable equalization. There is not even a disclosure requirement. Hyperliquid's users had to wait for a third-party analytics firm to tell them that every validator runs in one AWS region.

The contrast is stark. Traditional finance recognized that in a time-ordered system, geography is destiny, and spent decades building mechanisms to neutralize that reality. Crypto, which loudly claims to be building a fairer financial system, has done precisely nothing.

The Gamma Trap: Bitcoin's Parallel Prison

Bitcoin has traded in a tight range around $67,000 as covered-call selling suppresses volatility. (Pexels)

While the Hyperliquid latency story exposes structural inequality in DeFi's fastest market, Bitcoin itself is trapped in a different kind of structural cage - and the mechanism is equally mechanical.

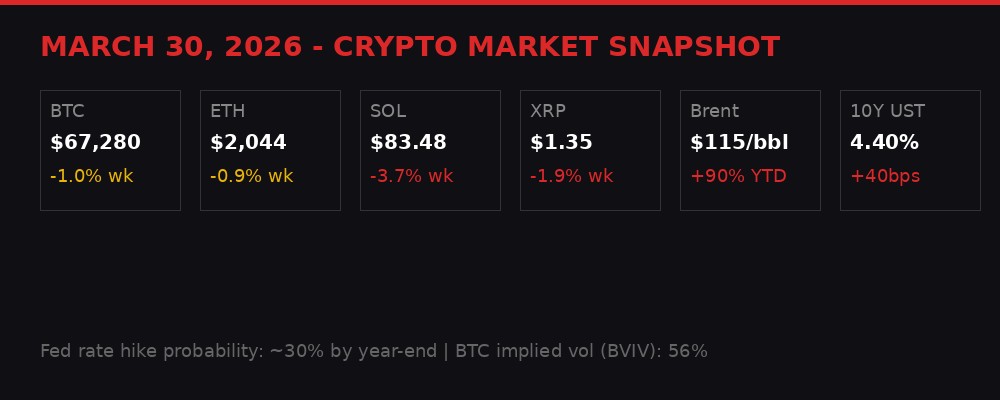

Bitcoin touched $65,112 early Monday morning, its lowest level since the war-related February crash, before recovering to $67,280. The 24-hour whipsaw - dip on escalation headlines, recovery on Asian buying - has become so predictable that traders are running automated strategies against it. BTC has not sustained a move above $75,000 or below $65,000 since mid-February, a five-week range that is remarkable given the macro backdrop.

The explanation lies in the options market. Throughout Q1 2026, institutional participants have been systematically selling covered calls at higher strikes. They own BTC. They sell someone else the right to buy it at a higher price. They collect the premium. It is the most vanilla yield-generation strategy in finance, and crypto institutions have been running it at industrial scale.

"Throughout Q1, institutional participants have been systematically overwriting calls at higher strikes to harvest premium in a down/sideways market. That activity transferred significant gamma exposure to dealers, who have been hedging by buying into dips and selling into rallies to maintain delta neutrality." - James Harris, CEO at Tesseract

The mechanics work like this: when institutions sell calls, market makers buy them. That leaves market makers with positive gamma - a position that forces them to buy BTC when it falls and sell BTC when it rises, purely to maintain a hedged book. The result is mechanical suppression of price swings. Every dip gets bought. Every rally gets sold. Not by conviction. By mathematics.

The Bitcoin 30-day implied volatility index (BVIV) has declined 5% to 56% this month. That is the opposite of what you would expect during a hot war in the Middle East, with oil at $115 a barrel, the 10-year Treasury yield at 4.40%, and the Nasdaq in correction territory. Every other asset class is seeing volatility spike. Bitcoin's is falling. The covered-call machine is the reason.

Bitcoin trades flat while oil, yields, and equities swing wildly. The gamma trap holds. (BLACKWIRE)

The irony is thick. Bitcoin was supposed to be the chaos hedge, the asset that moves when everything else is moving. Instead, the yield-seeking behavior of its own institutional holders has turned it into the most range-bound major asset on the planet. The Iran war pushed oil up 90% year-to-date. Gold fell 20% from its March highs. The Nasdaq entered correction. Bitcoin moved 3% in either direction and came right back.

The Macro Backdrop: Rate Hikes Return to the Table

The Fed faces its hardest policy decision since 2022 as inflation expectations reverse course. (Pexels)

The broader market context makes the latency and structure conversations even more urgent. Capital allocation decisions are being made in a macro environment that has turned upside down in five weeks.

The CME FedWatch Tool now shows nearly a 30% probability that the fed funds rate will be higher by year-end than its current 3.50-3.75% level. The odds of rates going lower have crashed to 2.9%. Six weeks ago, markets were pricing multiple rate cuts in 2026. The reversal is almost unprecedented in speed.

The driver is crude. Brent rose 2.5% Monday morning to approximately $115 a barrel, now up roughly 90% from the $70 level it traded at before the U.S.-Iran conflict escalated at the end of February. Oil at $115 feeds directly into consumer prices - gasoline, shipping costs, petrochemical inputs, food production. Core CPI was already running at 2.5% year-over-year in February, well above the Fed's 2% target. The oil shock threatens to push it past 3%.

Longer-term inflation expectations are moving too. Five-year breakevens sit at 2.5%, ten-year at 2.3%. These are not panic levels, but they are above target and trending in the wrong direction. The Federal Reserve does not set policy based on one month of data, but the combination of sticky core inflation, surging energy prices, and expanding geopolitical risk gives Chair Jerome Powell zero room to cut.

"Food and energy prices are tragically going to climb and remain high for a while, at least until the utter mess of Middle East shipping is sorted out. Even if a peace deal were to be agreed tomorrow (unlikely), that would take months at best." - Crypto is Macro Now Newsletter

The 10-year Treasury yield has climbed from below 4% to 4.40% in a matter of weeks. That 40 basis point move reprices everything - mortgages, corporate debt, risk assets, and particularly the discount rate applied to speculative technology bets. It explains the Nasdaq's correction and the pressure on growth stocks.

The U.S. economy has offsetting factors. It is a net energy exporter, which means higher oil prices flow partly into domestic revenue rather than purely into costs. Military spending is ramping up to replenish hardware used in the Iran campaign, adding fiscal stimulus. Both factors should prevent a sharp GDP contraction. But they do not prevent the inflation spiral that keeps the Fed trapped.

Bitcoin's relative performance is deceptive. Yes, it has held the $65,000-$70,000 range while gold dropped 20% and the Nasdaq fell 10%. But BTC was already down 50% from its October 2025 record high when the war started. It was underperforming before the conflict and it is still underperforming on any timeframe longer than five weeks. The "Bitcoin is outperforming" narrative requires cherry-picking the start date to February 28.

DeFi's Regulatory Collision Course: The CLARITY Act and Yield Kill Switch

The CLARITY Act threatens to redefine stablecoins as pure payment rails - no yield allowed. (Pexels)

The infrastructure centralization exposed by Glassnode's Hyperliquid research arrives at a moment when DeFi faces an entirely separate existential threat from Washington. The CLARITY Act - the crypto market structure bill winding through the Senate - contains language that would effectively ban yield on stablecoin balances.

The proposal redefines stablecoins as payment instruments, not savings products. No yield. No rewards. No interest-like distributions. The stablecoin becomes a digital dollar bill, useful for transactions but generating zero return for the holder. This might sound like a technical regulatory distinction. It is a structural shift in how capital flows through DeFi.

Markus Thielen, founder of 10x Research, laid out the implications in a March 29 report. "This represents a clear re-centralization of yield," he wrote. If stablecoins cannot offer yield, that yield gets pulled back into traditional finance - banks, money market funds, regulated wrappers that can offer returns under existing frameworks. The onchain yield that powered DeFi's growth evaporates.

The initial reaction from DeFi advocates was optimism. If centralized platforms cannot offer stablecoin yield, users will migrate to decentralized alternatives. Uniswap, Aave, Compound, dYdX - these protocols could absorb the displaced demand. But Thielen argues the math does not work that way. The CLARITY Act's framework is likely to extend to front-end interfaces and token models, particularly where fee generation or governance resembles equity.

Decentralized exchanges like Uniswap (UNI), SushiSwap, and dYdX could face tighter constraints on how they distribute value. Lending protocols like Aave (AAVE, currently $97.91) and Compound (COMP, $18.29) might see reduced volumes and weaker token demand as the regulatory framework narrows what is permissible. The result, according to 10x Research, is structurally bullish for infrastructure players like Circle (CRCL) and structurally bearish for DeFi tokens.

The Alsobrooks-Tillis agreement-in-principle, which industry representatives reviewed on March 23-24, drew complaints from both crypto and banking interests. Nobody is happy, which in legislative terms often means the compromise is close to final. Congress goes on Easter recess this week, but a markup hearing - where senators debate amendments before voting - is expected in the second half of April.

Aave's internal situation underscores the sector's fragility. The protocol, which holds roughly $26 billion in deposits, is navigating a governance crisis alongside its v4 technical upgrade. The Aave Chain Initiative (ACI), one of the DAO's most active governance groups, shut down in early March after clashing with Aave Labs over revenue distribution. BGD Labs, a key engineering contributor behind Aave v3, departed earlier citing strategic disagreements. CEO Stani Kulechov frames the churn as "very normal," but losing two of your most active contributors while regulators are rewriting the rules does not inspire confidence.

The Centralization Paradox: What Comes Next

When BitMEX moved from Ireland to Tokyo, liquidity jumped 180%. The gravity is real. (BLACKWIRE)

The Hyperliquid latency research is one data point. But it crystallizes a tension that runs through the entire crypto ecosystem: the gap between the decentralization narrative and the centralized reality.

Ethernodes.org data shows that approximately 36% of all Ethereum nodes run on AWS. An April 2025 AWS outage caused service degradation across Binance, KuCoin, and multiple other platforms, demonstrating how much of crypto's plumbing runs through a single corporate provider. The system is permissionless at the protocol layer and dangerously concentrated at the infrastructure layer.

For Hyperliquid specifically, the concentration creates two distinct risks. The first is the fairness problem exposed by Glassnode. In a time-ordered system, geography determines queue priority. A trading desk in Tokyo can reach the matching layer hundreds of milliseconds ahead of competitors in Hong Kong, Singapore, or the United States, securing better position, tighter spreads, and higher fill probability. This is not a bug. It is physics. And Hyperliquid has made no attempt to mitigate it.

The second risk is operational. Twenty-four validators in one AWS region means a single regional outage could halt the entire protocol. The April 2025 AWS incident proved this is not hypothetical. If ap-northeast-1 goes down for sustained period, Hyperliquid's $4 billion daily volume goes to zero until it comes back. There is no failover. There is no geographic redundancy. There is no backup.

Traditional exchanges solve this with multi-site architectures, disaster recovery data centers in different geographic zones, and regulatory requirements for business continuity planning. Crypto's decentralized exchanges have none of this. They run on one cloud, in one region, with one provider, and call it decentralized because the software layer is permissionless.

The path forward is technically clear. Hyperliquid could distribute validators across multiple AWS regions or multiple cloud providers. They could implement a speed bump mechanism similar to IEX's approach. They could add geographic randomization to order processing. They could publish latency data voluntarily rather than waiting for Glassnode to expose it. None of these solutions are technically impossible. They are economically undesirable because they would reduce the performance that attracts high-frequency traders, who generate a disproportionate share of volume.

That trade-off - performance versus fairness - is the same one Wall Street faced in the 1990s and 2000s. The answer there was regulation. Co-location rules, clock synchronization mandates, cable equalization requirements, and speed bumps were not voluntary improvements. They were imposed because exchanges would never voluntarily give up the advantages that attracted their most profitable clients.

Crypto is not there yet. There is no CFTC rule requiring geographic distribution of validator nodes. There is no SEC mandate for latency disclosure on decentralized exchanges. There is no MiFID II equivalent for DeFi market microstructure. The regulators are focused on whether prediction markets constitute gambling and whether stablecoins can offer yield. The infrastructure fairness question is years away from their attention.

In the meantime, the latency arms race that reshaped Wall Street over two decades is arriving in decentralized finance. It runs through Tokyo. It runs on AWS. And the traders who figured this out first have been collecting their 200-millisecond tax on every order, from every slower participant, on every trade, every day.

The question is not whether this is fair. The question is how long "decentralized" platforms can get away with infrastructure that makes a mockery of the word.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram