The Invisible Crisis: Iran's War Destroyed the World's Helium Supply and Now AI Chips Are Next

The numbers behind the Iran war's collision with global semiconductor supply chains. Spot helium prices have doubled since the Ras Laffan strikes began. Source: AP News, Kornbluth Helium Consulting, QatarGas, USGS.

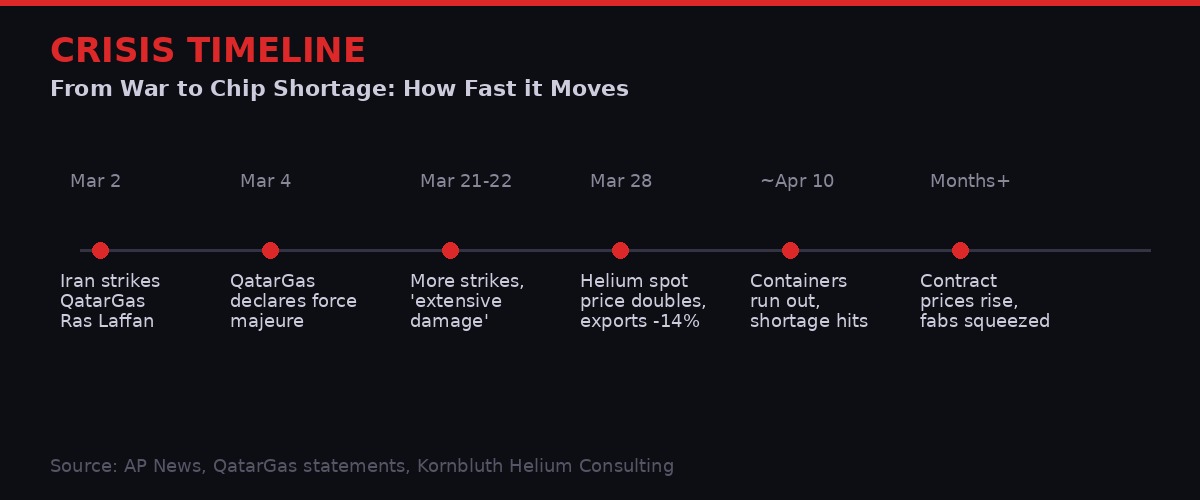

Qatar's Ras Laffan facility produces about a third of the world's helium. It's the largest liquefied natural gas plant on the planet, a cathedral of industrial infrastructure sitting on top of the world's biggest single natural gas reservoir. Since March 2, Iranian drone strikes have methodically dismantled it.

On that first day, QatarGas halted production of LNG and "associated products." Two days later it declared force majeure - legally absolved of its contractual obligations due to circumstances beyond its control. Then the strikes kept coming. Wednesday. Thursday. Reported "extensive" damage that QatarGas said would take years to repair. The company then announced a 14% cut in annual helium exports, and analysts said that number could climb higher.

Most of the world heard about Qatar's gas problems in terms of oil markets and energy prices. That framing missed the deeper story. Helium - the same gas that makes party balloons float - is a critical and irreplaceable input in semiconductor manufacturing. The chips inside every AI server, every smartphone, every gaming console, every MRI machine, need helium to be made. And now the world's largest supplier just went dark.

The shortage hasn't fully arrived yet. The containers of liquid helium that were en route when the war erupted are still working their way through the supply chain. But Phil Kornbluth, president of Kornbluth Helium Consulting and one of the foremost experts on global helium markets, put it plainly to AP reporters this week:

"Nobody's run out of helium yet. But it's a few weeks out when the shortage really hits." - Phil Kornbluth, President, Kornbluth Helium Consulting, March 2026

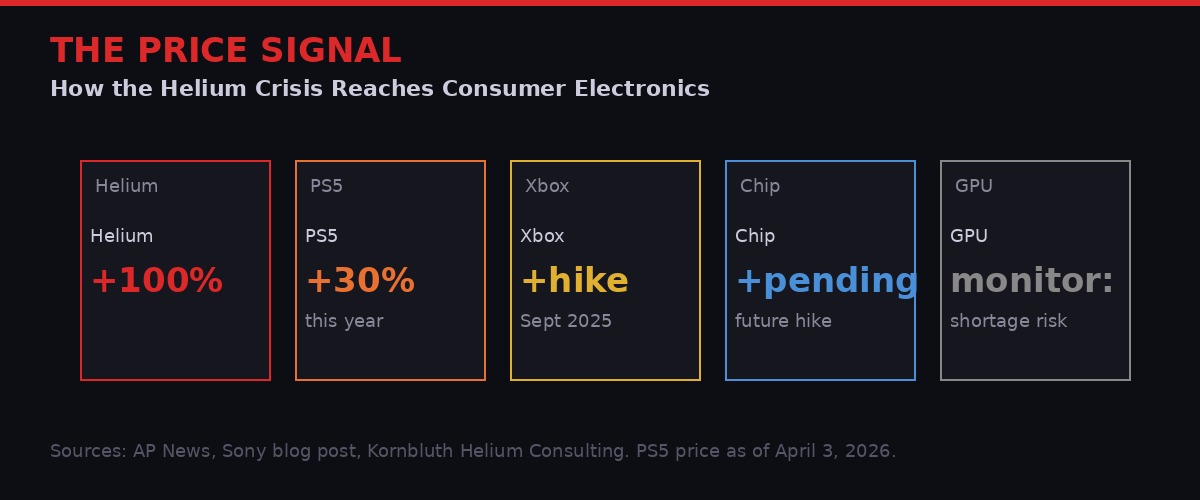

The second-order effects are already rippling through consumer electronics. Sony announced this week that the PlayStation 5 will cost $649.99 in the US starting next Thursday - a $100 increase, bringing the console's total price rise to roughly 30% over the past year. The company cited "continued pressures in the global economic landscape." It didn't specifically name helium. It didn't need to.

Why You've Never Heard of This Problem Before

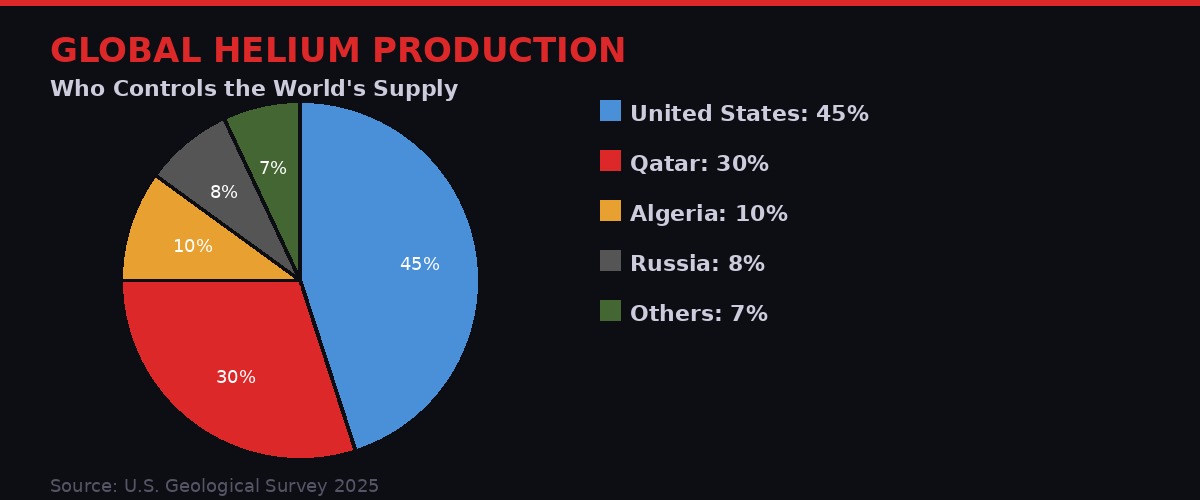

The United States dominates total helium reserves, but Qatar dominated the export market. With Russian supplies cut off by sanctions, a Qatar disruption leaves the world scrambling for alternatives. Source: U.S. Geological Survey.

Helium doesn't appear in the popular imagination as a strategic industrial resource. That's a failure of economic literacy, not a reflection of reality. The U.S. government recognized helium's critical importance decades ago - the Federal Helium Reserve in Amarillo, Texas was created in 1925, originally to supply military airships. The Reserve today holds 8.5 billion cubic meters of recoverable helium underground. It's the strategic oil reserve equivalent for a gas most people only think about in the context of birthday parties.

The industrial profile of helium is dominated by two properties: extreme coldness at liquid state (just 4 degrees above absolute zero) and excellent thermal conductivity in gas form. Both properties make it uniquely valuable in precision manufacturing environments where temperature stability is everything.

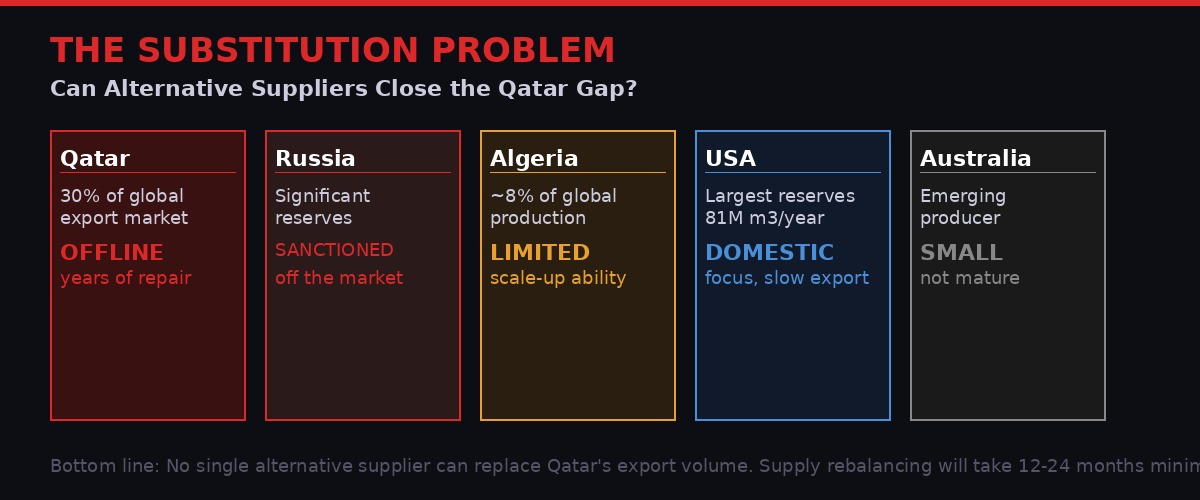

The global helium supply chain is a four-country operation. The United States produces the most, around 81 million cubic meters per year according to the U.S. Geological Survey. Qatar, Algeria, and Russia make up the rest of meaningful production. Russia is effectively off the table - US and EU sanctions banned those supplies. That leaves the United States, Algeria, and Qatar as the active export market. Qatar alone was supplying approximately 30% of global demand before the war.

The concentration problem is worse than the numbers suggest. While the US holds enormous reserves and produces significant volumes, most of that production is consumed domestically. The international export market was disproportionately dependent on Qatar's Ras Laffan facility. When Iran struck it, they didn't just damage a gas plant. They hit the world's helium distribution hub.

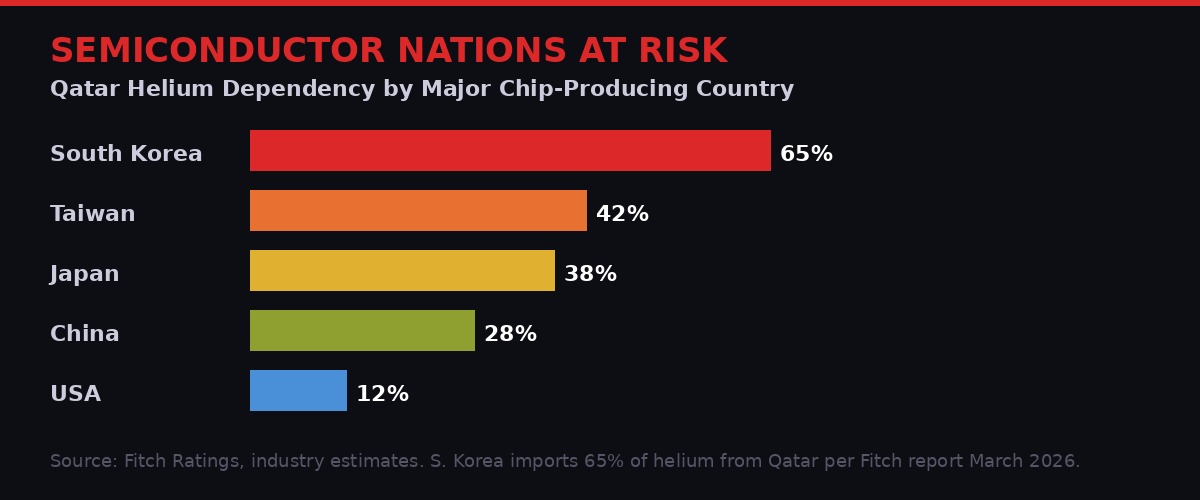

Qatar supplies approximately 30% of global helium. South Korea imports 65% of its helium from Qatar, according to Fitch Ratings. Samsung Electronics and SK Hynix - the world's two largest memory chipmakers - are both South Korean. The math is uncomfortable.

Inside the Fab: Why Chips Cannot Be Made Without Helium

The plasma etching stage is where helium dependency becomes absolute. There is no viable substitute for helium backside cooling during etching. Source: Georgetown CSET analysis, Sangmyung University.

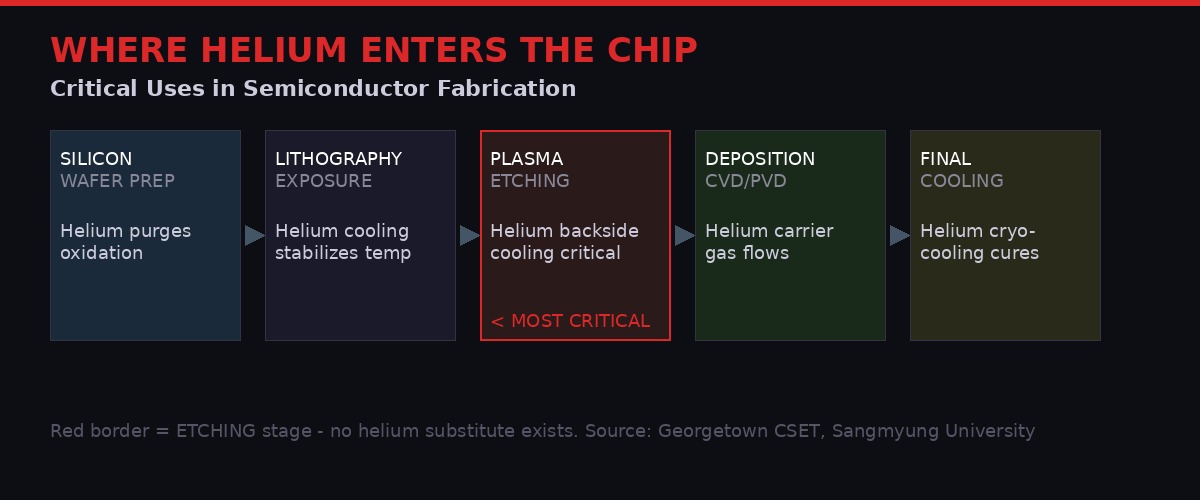

Semiconductor fabrication is one of the most thermally sensitive industrial processes humans have ever invented. A modern chip fab - TSMC's in Taiwan, Samsung's in South Korea, Intel's in Ohio - operates under conditions where a temperature variance of fractions of a degree can destroy an entire wafer batch worth tens of thousands of dollars.

Jacob Feldgoise, an analyst at Georgetown University's Center for Security and Emerging Technology, explained the core dependency to AP. During plasma etching - one of the most critical stages of chip manufacturing, where material deposited on silicon wafers is precisely scraped away to form transistor structures - temperature control is not optional. It's physics.

"You really want to maintain a constant temperature over the wafer. And in order to do that, you need to be able to draw heat away from the wafer that's being processed. Helium is an excellent thermal conductor. And so chip fabs will blow helium over the back of the wafer in order to speed heat removal and keep heat removal consistent." - Jacob Feldgoise, Georgetown University Center for Security and Emerging Technology

The critical detail is the finality of it: there is currently no viable substitute for helium in wafer backside cooling during etching. This is not a case of "helium preferred but alternatives work acceptably." Jong-hwan Lee, a professor of semiconductor devices at South Korea's Sangmyung University, was unequivocal: under current semiconductor manufacturing processes, helium cannot be replaced.

This isn't a niche corner of the process. Plasma etching is how transistors are made. Modern AI chips from Nvidia, AMD, and Apple contain billions of transistors packed at densities measured in nanometers. Every single one of them was shaped by a process that required helium gas continuously blown over the back of a silicon wafer to keep it at the right temperature.

Helium also appears at other points in the fabrication flow. It's used in the initial wafer preparation stages to purge oxidation. It serves as a carrier gas during chemical vapor deposition. At the back end, it plays a role in cooling systems that cure final chip packages. The etching stage is the most critical, but helium isn't easily extracted from any single point in the manufacturing chain - it's woven through the entire process.

The 35-Day Clock Ticking on Global Chip Supply

The crisis timeline runs faster than most people expect. Containers shipped before March 2 are the world's buffer. Once those run out, the shortage hits chip fabs and hospitals simultaneously.

Helium is harder to store and transport than almost any other industrial gas. Its atomic structure is the problem: helium atoms are the smallest in existence, and they slip through container walls and microscopic gaps that would hold any other gas. Even the specialized cryogenic containers used for liquid helium transport - insulated tankers that cost approximately $1 million each - can only hold liquid helium for 35 to 48 days before the gas warms and pressure-release valves vent it into the atmosphere.

There are about 200 of these containers currently stuck in the Middle East, according to Kornbluth. The containers need to get out of Qatar, get repositioned to alternative filling locations, and get back into the supply chain - all within a window measured in weeks, not months. Kornbluth didn't mince words about the complexity:

"It's going to take a fair amount of time to get these containers out of Qatar and to get them somewhere else where they might be able to be filled with helium. So this initial period when you lose Qatar supply and have to rejig the supply chain and reposition containers, that's going to be the worst part of the shortage most likely." - Phil Kornbluth, Kornbluth Helium Consulting

The math on this is stark. The war erupted in early March. Helium containers that were already filled and on ships before the fighting began continued their journeys - those supplies are the current buffer. Fabs in Asia have been receiving those shipments for the past three weeks. But Kornbluth's estimate is that "in a few weeks," those supplies run out and the shortage becomes real.

That puts the potential onset of actual chip production disruption somewhere in April. The timing coincides precisely with the period when the Iran war is expected to enter its most intense phase, following Israel's nuclear facility strikes last week and the deployment of the US 82nd Airborne in the region. There is no scenario where helium production resumes quickly in the current military environment.

Spot prices for helium have already doubled. But Kornbluth emphasized that spot trading is only about 2% of the total helium market. The bulk of helium is sold through long-term contracts, which lag spot prices. When those contract renewals come up - or when suppliers can renegotiate force majeure clauses - prices could move dramatically higher across the board.

The Countries That Can't Afford to Be Wrong

South Korea's semiconductor industry faces the sharpest exposure. Samsung and SK Hynix together dominate global memory chip production. Both are headquartered in a country that imports 65% of its helium from Qatar. Source: Fitch Ratings, March 2026.

A Fitch Ratings report issued this week identified South Korea as "particularly vulnerable" to the helium supply disruption. The reason is concentration risk compounded on concentration risk: South Korea hosts Samsung Electronics and SK Hynix, the world's two largest memory chip makers. The country imports approximately 65% of its helium from Qatar. When you're simultaneously the dominant global memory chip producer and the country most dependent on the specific supplier that just got bombed, the word "vulnerable" barely covers it.

Jong-hwan Lee at Sangmyung University said Samsung and SK Hynix likely have several months of inventory built up. This is normal for any commodity that companies know can be disrupted - chip fabs don't run on just-in-time delivery for critical gases any more than airlines hedge their fuel costs. But "several months" is a finite window. If the war continues into summer - which analysts increasingly view as the baseline scenario given the scale of the conflict - those buffers erode.

Lee's warning went further than just inventory levels. He flagged helium as one of 14 semiconductor supply chain materials the South Korean government has placed under monitoring due to war-related vulnerability. The critical systems thinking here is important: chip fabrication is a sequential process where each stage depends on the last. You don't need to run out of helium entirely to break a fab's output. You need only to disrupt one stage sufficiently to create quality failures or process halts that cascade through the entire production line.

"Even disruptions affecting just a handful of materials could destabilize the entire semiconductor manufacturing process as each stage of production depends on the previous one." - Jong-hwan Lee, Professor of Semiconductor Devices, Sangmyung University

Taiwan Semiconductor Manufacturing Company, the world's dominant logic chip foundry and the company that physically manufactures chips for Apple, Nvidia, AMD, and most of the AI industry, told AP that it does "not anticipate any significant impact at this time" but is "continuing to monitor the situation." TSMC's phrasing is careful. It's the kind of statement a company issues when it wants to avoid market panic while internally running contingency planning at full speed.

Taiwan's own helium dependency is significant, though Fitch's data suggests it has more diversification than South Korea. Japan - home to major chip component manufacturers including Shin-Etsu Chemical, the world's largest producer of silicon wafers - faces similar questions about supply chain resilience. China, despite political tensions with the West, actually imports less of its helium from Qatar as a proportion of total demand, partly because it has developed some domestic production and partly because its semiconductor industry, while large, focuses on older process nodes that have slightly different gas consumption profiles.

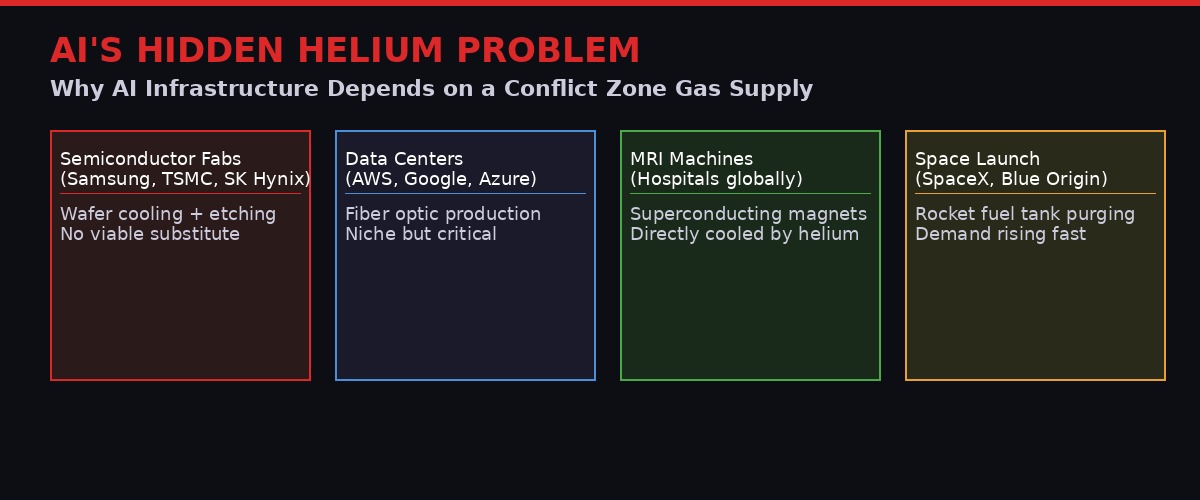

AI's Hidden Helium Problem

The helium dependency extends beyond chip fabs into fiber optic production for data centers, MRI machines at hospitals, and rocket fuel systems at SpaceX and Blue Origin. The shortage will not respect sector boundaries.

The AI investment boom of 2023 through 2026 has been powered by an enormous surge in demand for advanced semiconductors - specifically Nvidia's H100 and H200 GPUs, AMD's MI300X, and the custom AI accelerators built by Google (TPUs), Amazon (Trainium, Inferentia), and Microsoft (Maia). Every one of those chips was manufactured in a fab that uses helium.

The irony is that the AI industry's aggressive capital expenditure has, in a sense, tightened helium markets even before the Iran war. Samsung and TSMC have been running their most advanced nodes at near-maximum utilization to keep up with AI chip demand. High utilization means higher helium consumption per unit of time. The buffers that might absorb a supply shock during a period of slower production have been partially depleted by the very demand surge the AI industry represents.

Data centers themselves have a less direct but real helium dependency. Fiber optic cables - the infrastructure that connects data centers to each other and to the internet - require helium during the manufacturing process. Modified Chemical Vapor Deposition, the process used to make optical fiber preforms, uses helium as a cooling medium. A prolonged helium shortage would eventually constrain the rate at which new fiber optic capacity could be built - exactly the opposite of what a world trying to expand AI infrastructure needs.

The medical sector will compete with chip fabs for whatever helium remains available. MRI machines - roughly 40,000 of which are in operation globally, according to medical imaging industry estimates - rely on liquid helium to cool the superconducting magnets that create the magnetic fields used to image soft tissue. There is no alternative. Current MRI technology is based on superconducting magnets that require cooling to temperatures only achievable with liquid helium. In an allocation scenario, chipmakers and medical facilities will both be arguing for priority access to diminishing supply.

SpaceX and Blue Origin use helium to purge fuel tanks before and during launches - removing oxygen and moisture that could cause explosions or contamination. Both companies have been dramatically ramping launch cadence over the past two years. SpaceX completed over 130 missions in 2025 alone. That launch volume represents a meaningful and growing helium demand, competing with fabs and hospitals from the same shrinking pool.

The Consumer Electronics Feedback Loop

The price cascade has already begun. Sony's PS5 increase is the visible signal. The chip contract price renegotiations that follow a prolonged shortage will be the invisible but larger hit to consumer electronics economics. Source: AP News, Sony, Kornbluth Helium Consulting.

Sony's PlayStation price hike, announced this week, is a preview of a broader trend that's just getting started. The PS5 will cost $649.99 from next Thursday - a $100 increase. The PS5 Pro will hit $899.99, a $150 jump. The digital edition rises by $100 to $599.99. Sony cited "continued pressures in the global economic landscape." The company did not specifically mention helium or semiconductor input costs. It mentioned the Iran war's effect on global energy and manufacturing supply chains in general terms.

The second-order connection is not difficult to trace. Sony manufactures its PlayStation hardware using chips sourced from TSMC and other foundries. Those foundries operate in countries now staring down a helium supply crisis. Even if the immediate helium shortage doesn't shut down production lines - fabs will pay premium prices before they halt - it raises input costs throughout the semiconductor supply chain. Those costs ultimately land on the consumer.

Microsoft had already raised Xbox prices in September 2025, citing "changes in the macroeconomic environment," before the Iran war started. Both console makers were responding to the same underlying pressures: tariffs, supply chain fragmentation, higher energy costs, and semiconductor input inflation. The helium crisis layering onto these existing pressures is not a separate event - it's an acceleration of forces already in motion.

The question analysts are now asking is whether the helium crisis reaches GPU markets. Nvidia's AI chips - already in short supply due to manufacturing constraints and overwhelming demand - are produced at TSMC's leading-edge nodes. Any disruption to TSMC's fabrication throughput, even a partial one, would further tighten a market that has been capacity-constrained for two years. Cloud providers have been arguing publicly that AI infrastructure deployment is limited by GPU availability. A helium-driven slowdown in TSMC output would validate that concern at the worst possible moment.

Can the World Substitute Its Way Out?

No alternative supplier can plug the Qatar gap quickly. Russia is under sanctions. Algeria lacks scale-up capacity. US production is mostly consumed domestically. Australia is still developing. The market must tighten before it rebalances.

The honest answer is: not quickly, and not completely.

The United States holds enormous helium reserves and produces significant volumes. But U.S. production is not simply pluggable into the gap left by Qatar. The issue is logistics. Helium export terminals, specialized shipping infrastructure, and the global network of cryogenic containers are calibrated around existing supply patterns. Redirecting supply at scale takes months, not weeks.

Algeria has meaningful production capacity and has been increasing exports. But Algeria also faces its own infrastructure constraints and cannot rapidly scale output to cover Qatar's share of the market. No single alternative supplier can close the gap.

At the fab level, chipmakers have some ability to optimize helium usage. Feldgoise noted that because helium is a small fraction of overall production costs, fabs "would be willing to pay a higher price" to secure supplies rather than halt production. This is economically rational - a fab that costs billions of dollars to build and generates hundreds of millions in revenue per month will pay almost any input price premium before it shuts down a process line. But paying more doesn't solve a physical shortage; it just determines which buyers survive the allocation.

Research into alternative cooling approaches for semiconductor manufacturing does exist. Some fabs have experimented with alternative gases for specific process steps. But the etching stage dependency on helium backside cooling - identified by both Feldgoise and Lee as the critical constraint - has no near-term substitute. Years of research and qualification testing would be required to change the manufacturing process at scale, even if a viable alternative were identified tomorrow.

The Korea Semiconductor Industry Association issued a measured public statement saying short-term supplies are sufficient and companies have been diversifying supply routes. Both Samsung and SK Hynix declined to answer specific questions about inventory levels or diversification plans. That silence is its own kind of signal. Companies don't go quiet about their strategic resource positions when they're confident. They go quiet when the answer would worry investors or competitors.

The War Nobody Was Watching as a Tech Story

The Iran war has been covered primarily through the lens of oil prices, military strategy, regional geopolitics, and humanitarian costs. All of those framings are important. But the technology supply chain angle has been almost entirely absent from mainstream coverage, despite the fact that its consequences will ultimately reach more people than the direct military conflict - reaching into hospitals, computing infrastructure, and consumer electronics pricing in every country on earth.

This is a pattern in how technology coverage misses cascading effects. When Russia invaded Ukraine in 2022, the semiconductor industry scrambled to understand its exposure to neon gas - a byproduct of Ukraine's steel industry used in chipmaking laser systems. Prices spiked dramatically before alternative sources were secured. That near-miss taught the industry something about its invisible dependencies. But knowledge of a vulnerability and full resilience to it are different things. Ukraine-neon was a wake-up call that led to some supply diversification but not complete decoupling.

Qatar-helium is a harder problem. Neon has multiple production points globally and can be manufactured as a byproduct of air separation plants anywhere there's steel production. Helium is geologically concentrated. It forms from the alpha decay of uranium and thorium in the earth's crust over millions of years and collects in natural gas reservoirs. You cannot manufacture it. You can only find it where geology put it.

The three years of peak AI investment from 2023 to 2026 created global dependencies on chip manufacturing at a scale without precedent in computing history. Nvidia's data center revenue alone exceeded $100 billion in fiscal 2026. The cloud providers - AWS, Microsoft Azure, Google Cloud - collectively committed hundreds of billions to AI infrastructure. All of that investment sits downstream of the semiconductor fabrication process. All of that fabrication process requires helium.

When analysts run scenarios about what could slow the AI infrastructure buildout, they model GPU supply constraints, power grid limitations, data center permitting timelines, and talent shortages. Almost none of them were modeling "Iran bombs Qatar's gas facility and the world's helium supply drops 30% in a month."

That scenario is no longer hypothetical. It's the current situation as of the last week of March 2026. The shortage, per Kornbluth's assessment, is "a few weeks out" from becoming real in chip fab supply chains. The Ras Laffan facility faces years-long repair timelines. The war shows no signs of ending.

The party balloon gas is about to become the most strategically important substance in global technology supply chains. Most of the world isn't paying attention yet. It will be soon.

Monitor TSMC and Samsung earnings calls for any mention of "process gas" supply or input cost pressures. Watch for GPU pricing changes in spot markets (secondhand H100/H200 prices will be an early signal). Track the Korea Semiconductor Industry Association statements weekly - their language will shift from "sufficient" to "monitoring closely" to "contingency measures" as the shortage deepens. The signal will come before most media coverage does.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on TelegramSOURCES

- AP News - "Why the Iran war matters for the world's helium supply" (March 2026)

- AP News - "Sony raises PlayStation prices by $100" (March 2026)

- Phil Kornbluth, Kornbluth Helium Consulting - expert analysis cited by AP

- Jacob Feldgoise, Georgetown University Center for Security and Emerging Technology

- Jong-hwan Lee, Professor of Semiconductor Devices, Sangmyung University, South Korea

- Fitch Ratings - South Korea semiconductor sector helium vulnerability report, March 2026

- U.S. Geological Survey - Global Helium Production Data

- QatarGas - Force majeure declaration, March 4, 2026 / Export cut announcement March 2026

- Korea Semiconductor Industry Association - Public statement, March 2026

- Taiwan Semiconductor Manufacturing Company - Public statement, March 2026