$200 a Barrel: The Iran War's Economic Reckoning

Thirty days into the conflict, the damage has spread far beyond the battlefield. Oil markets are in shock. A fifth of the world's LNG is offline. Fertilizer prices are spiking. Wall Street has posted its worst five-week run in years. And strategists say it could get far worse before it gets better.

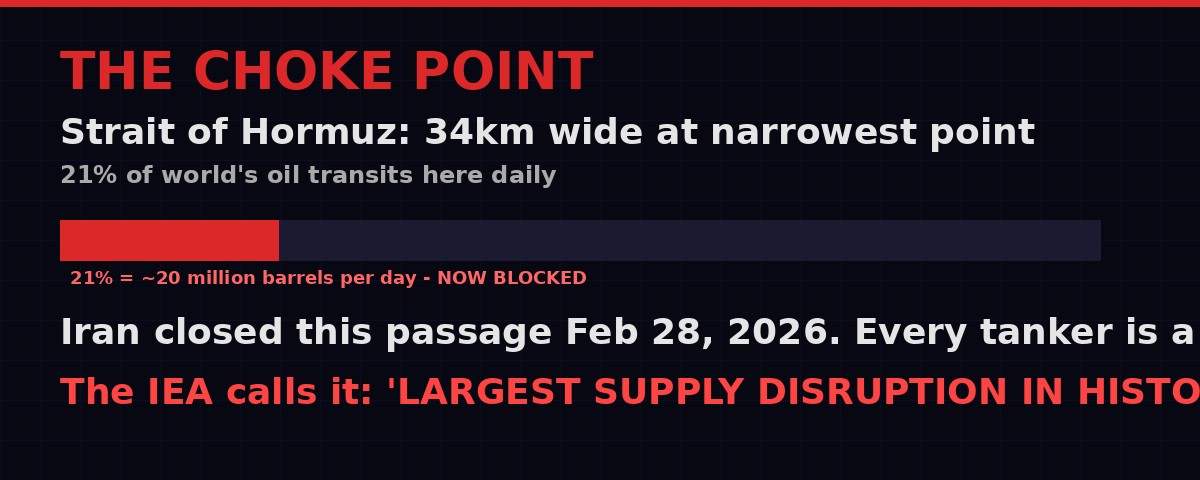

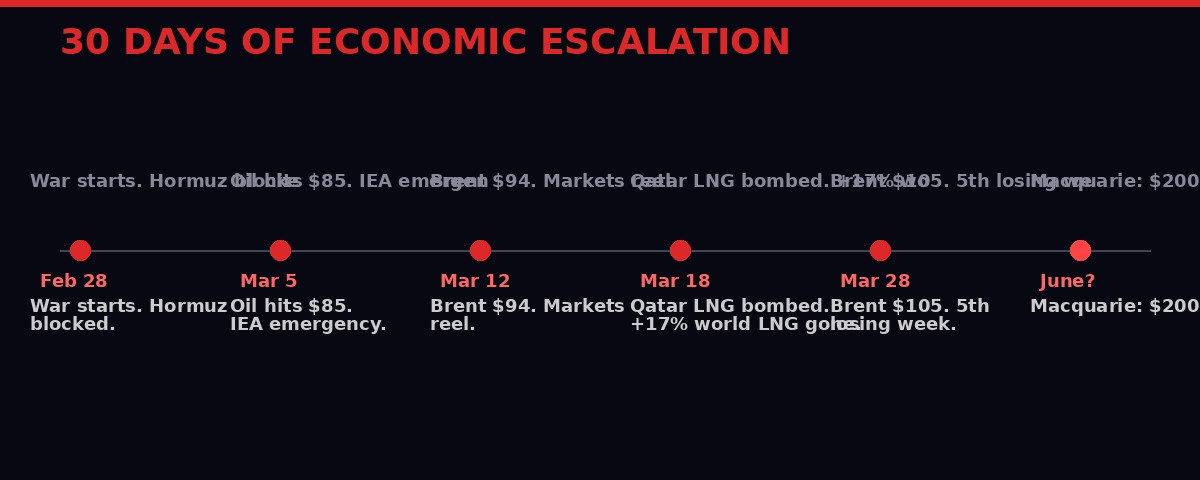

On February 28, the United States and Israel launched the opening strikes of what became the Iran war. Iran's response was swift, asymmetric, and devastating to the global economy: it effectively closed the Strait of Hormuz, the narrow waterway through which a fifth of the world's oil supply flows every day.

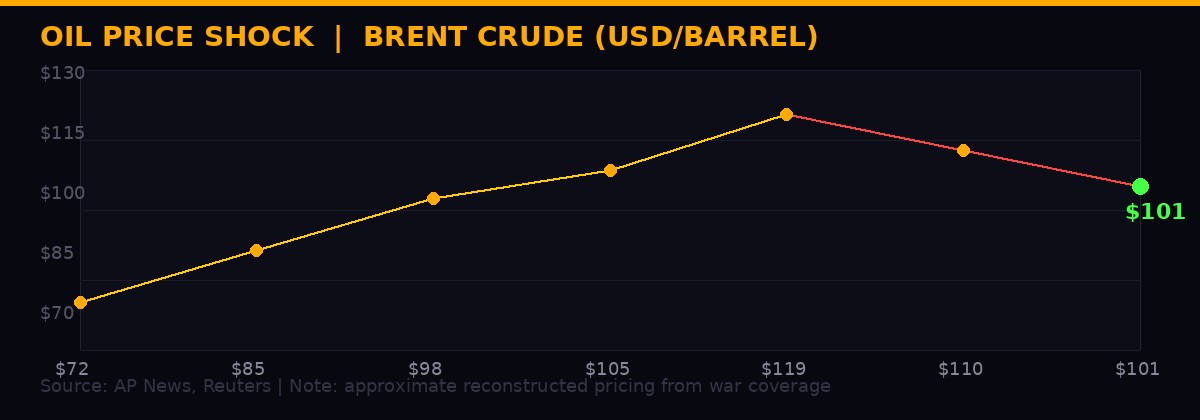

That single action - threatening tankers attempting to transit the 34-kilometer passage at its narrowest point - has set off a cascade of economic shocks that now dwarf the military engagements themselves. Brent crude has climbed 50% since the war began, settling at $105.32 a barrel on Friday. Analysts at Macquarie say $200 a barrel is possible by June if the war drags on. The all-time record for oil is $147.27, set in July 2008.

Thirty days in, the Iran war is no longer just a military conflict. It is a full-spectrum economic crisis with implications for every country on earth that drives a car, heats a building, grows food, or manufactures anything.

Snapshot: War Day 30 - Economic Damage

- Brent crude: $105.32 (+50% since Feb 28) - Source: AP/NYMEX

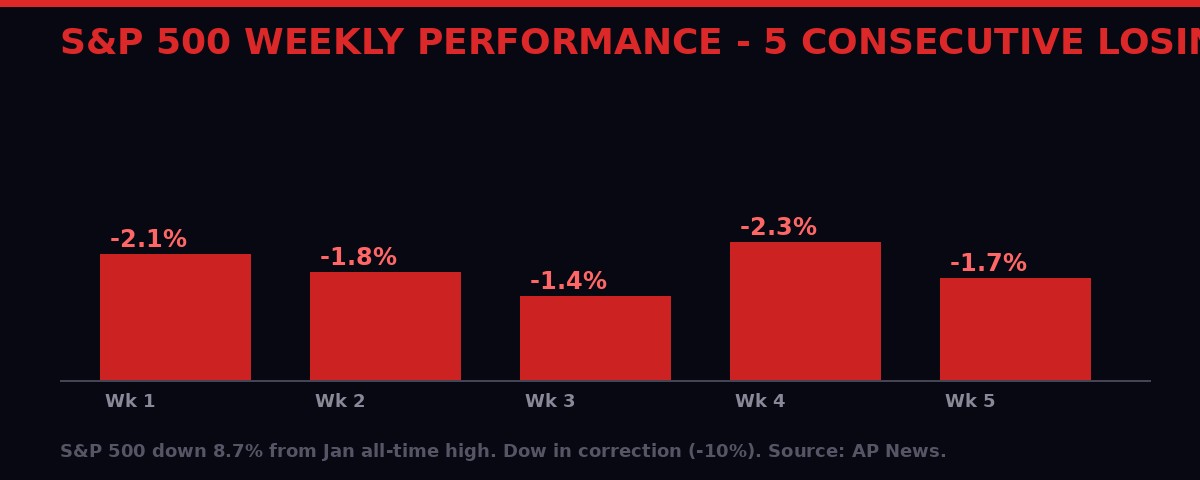

- S&P 500: -8.7% from January all-time high, 5th straight losing week

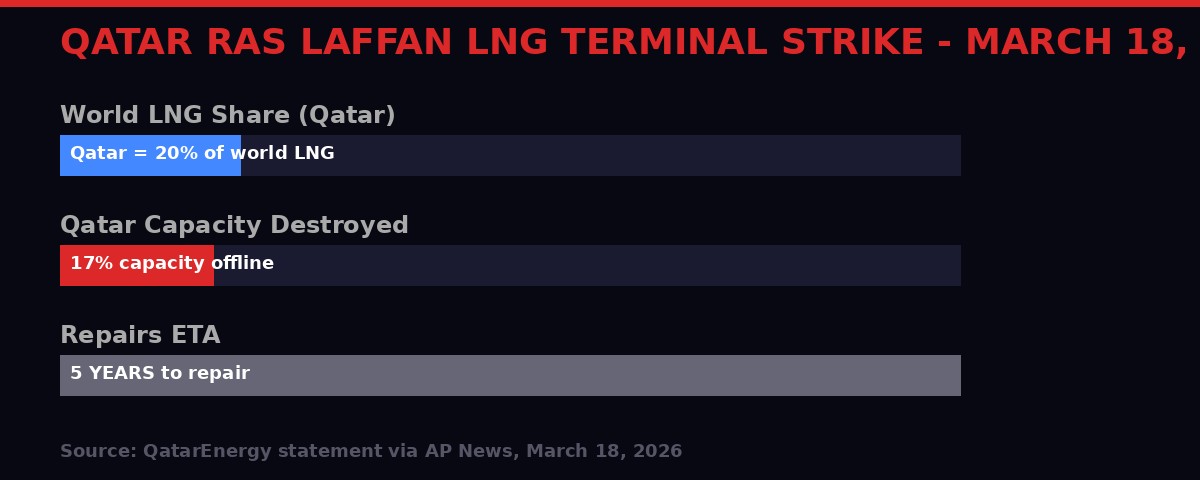

- Qatar LNG terminal: 17% of world LNG capacity offline, 5-year repair timeline

- Fertilizer (urea): +50% since war began

- Fertilizer (ammonia): +20% since war began

- IEA designation: "Largest supply disruption in the history of the global oil market"

- Macquarie oil forecast (June): $200/barrel if war continues

The Choke Point That Controls the World

The International Energy Agency does not use superlatives lightly. Its designation of the Hormuz closure as the "largest supply disruption in the history of the global oil market" is a number: roughly 20 million barrels a day removed from world supply, virtually overnight. (AP News, March 2026)

For context, the 1973 Arab oil embargo removed about 4.4 million barrels a day from Western markets - and it triggered a global recession, decade-long stagflation, and fundamentally reshaped the political economy of energy. The current disruption is nearly five times larger in raw volume, even accounting for today's slightly larger global consumption base.

The strait is 34 kilometers wide at its narrowest point - about the distance from central Paris to Charles de Gaulle airport. Two shipping lanes, each just three kilometers wide, connect the Persian Gulf to the open ocean. Through those lanes flows the oil exports of Saudi Arabia, Iraq, the UAE, Kuwait, Qatar, and Iran itself. No strait, no oil. It is that simple.

Iran has not fully cut the waterway. Instead, it has applied selective pressure - allowing some vessels through, threatening others, demonstrating that it holds the economic fate of oil-importing nations in its hands. Gulf producers including Kuwait and Iraq have cut output because there was nowhere for their oil to go without safe passage. (AP News/IEA data, March 2026)

"A week ago or certainly two weeks ago, I would have said: If the war stopped that day, the long-term implications would be pretty small. But what we're seeing is infrastructure actually being destroyed, which means the ramifications of this war are going to be long-lived." - Christopher Knittel, energy economist, Massachusetts Institute of Technology

That last sentence is the critical shift. Early in the war, markets priced the conflict as temporary - a short shock that would be resolved by diplomacy. That assumption has been shattered by a series of strikes on permanent infrastructure that will take years, not weeks, to repair.

Qatar's LNG: A Five-Year Wound

On March 18, Iranian missiles struck Qatar's Ras Laffan industrial complex - the largest LNG production facility on earth and the engine behind Qatar's vast oil wealth. The strike wiped out 17% of Qatar's LNG export capacity. QatarEnergy, the state oil company, said repairs will take up to five years. (AP News, QatarEnergy statement, March 18, 2026)

Qatar supplies approximately 20% of the world's liquefied natural gas. That means the Ras Laffan strike effectively removed roughly 3.4% of global LNG supply in a single afternoon - not temporarily, but for years. The timing could not have been worse. Europe, still rebuilding its gas buffer stocks after the Russia-Ukraine disruptions, was heavily reliant on Qatari LNG to diversify away from Russian pipeline gas.

The ripple effects were immediate. European gas futures spiked on news of the strike. Asian buyers - Japan, South Korea, Taiwan - who collectively import the largest share of Qatari LNG scrambled to find alternative supply. There is no simple alternative. Australian LNG exports are already running near capacity. American LNG export terminals are booked years in advance.

"No country will be immune to the effects of this crisis if it continues to go in this direction." - Fatih Birol, International Energy Agency Executive Director, March 23, 2026

The Ras Laffan strike also destroyed a significant share of global helium production. Helium is a byproduct of natural gas processing and a critical industrial input for semiconductor manufacturing, rocket propulsion systems, and medical MRI imaging. Qatar supplies roughly a third of the world's helium. With those production lines offline for years, chipmakers and hospitals face a slow-building shortage with no obvious fix. (AP News, March 2026)

The LNG strike was not incidental. It was strategic. Iran understands that Qatar hosts both the largest U.S. air base in the Middle East and a diplomatic infrastructure that has long served as a back-channel between Washington and Tehran. Striking Ras Laffan was a signal: no one in the region is untouchable, and economic pain can be distributed as precisely as military force.

Wall Street's Five-Week Collapse

American financial markets entered the war week with a familiar ritual: hope for a deal, followed by disappointment, followed by losses. The S&P 500 fell 1.7% on Friday alone - its worst day of the week - to close its fifth consecutive losing week. The index is now 8.7% below its all-time high set in January. The Dow Jones Industrial Average has fallen more than 10% from its record, entering correction territory. The Nasdaq has followed. (AP News, March 28, 2026)

The pattern during the war has been almost formulaic. When Trump signals willingness to delay deadlines or hints at negotiations, oil prices slip and stocks rally. When fighting continues and Iran rejects talks - as it has consistently done publicly - the market sells off. Investors have learned not to trust the rally.

"Any further statements by Trump about a deal are white noise to the markets. Only if the IRANIANS say the talks are going well will it impact markets." - Jim Bianco, president and macro strategist, Bianco Research

The week encapsulated the war's market paradox. Trump extended his self-imposed deadline to "obliterate" Iranian energy plants to April 6 - a move that briefly gave markets hope. Oil prices eased after the announcement. But by Friday, oil had climbed back to fresh highs as fighting continued and Iran gave no credible diplomatic signal. The deadline extension had bought hours of market relief, not a solution. (AP News, March 27-28, 2026)

Big Tech absorbed outsized losses. Amazon fell 4%, Meta Platforms shed 4%, Nvidia dropped 2.2%. The logic is straightforward: higher energy costs threaten the economics of massive data centers. Higher inflation expectations compress valuations. And if consumer spending contracts - as University of Michigan confidence surveys suggest it is beginning to do - the advertising and e-commerce revenues that underpin these companies shrink with it.

Consumer discretionary names were even harder hit. Norwegian Cruise Line lost 6.9%, Starbucks dropped 4.8%, Chipotle sank 4.1%. These are companies that depend on consumers feeling flush enough to spend on non-essentials. When gasoline is expensive and the news is dark, people cut back. The math is visible in the weekly consumer sentiment data.

Doug Beath, global equity strategist at Wells Fargo Investment Institute, put it plainly: "The diplomatic dissonance this week between the U.S. and Iran dismayed investors. By the end of the week, risk appetite could not withstand the fog of war." (AP News, March 28, 2026)

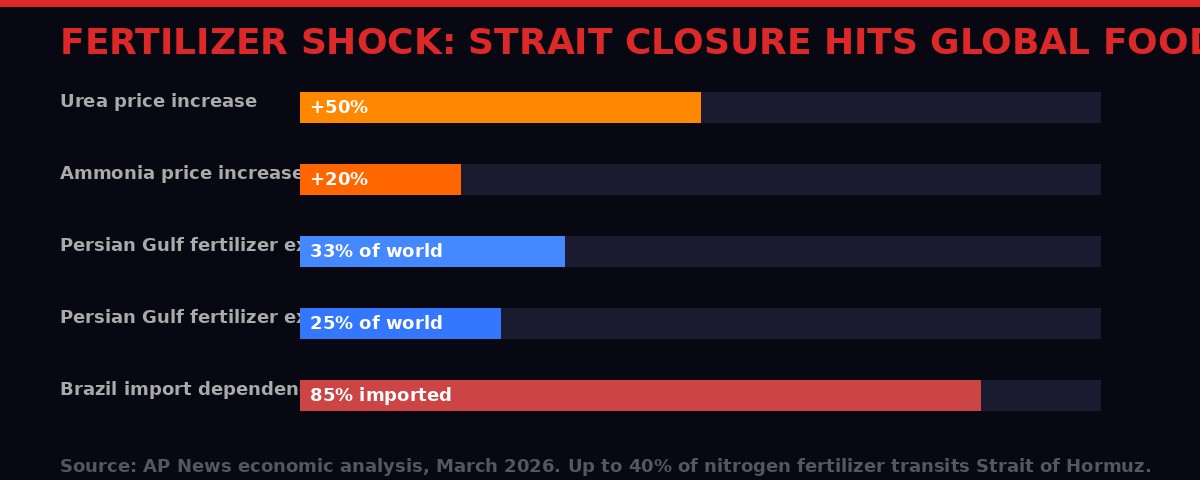

The Fertilizer Shock Nobody Is Talking About

While oil prices dominate the headlines, a slower and potentially more damaging shock is building in global agriculture. The Persian Gulf is one of the world's largest production regions for nitrogen fertilizers - specifically urea and ammonia - because of its access to cheap natural gas, the primary feedstock for these products. (AP News, March 2026)

The Persian Gulf accounts for roughly a third of world urea exports and a quarter of ammonia exports. Critically, up to 40% of all nitrogen fertilizer traded globally passes through the Strait of Hormuz. Since February 28, that flow has been strangled. Urea prices have risen 50% since the war began. Ammonia is up 20%.

For wealthy farmers in rich countries, higher fertilizer costs are an unpleasant line item. For farming economies in the developing world, they are existential. Brazil - one of the world's largest agricultural exporters and a country that feeds hundreds of millions of people globally - imports 85% of its fertilizers. Alpine Macro commodity strategist Kelly Xu has flagged Brazil's exposure as among the most acute in the world. (AP News, March 2026)

Egypt, a significant fertilizer producer in its own right, faces a different squeeze: it needs natural gas as a feedstock and has struggled to secure supplies since the Ras Laffan strike disrupted regional gas markets. When Egypt's fertilizer output falls, the effects ripple across sub-Saharan Africa and parts of the Middle East that depend on Egyptian agricultural exports.

The chain is simple but brutal: higher fertilizer costs lead farmers to use less of it, which leads to lower crop yields, which leads to less food in global markets, which leads to higher food prices, which falls hardest on the world's poorest families. This process takes months to play out - the 2026 planting season is already underway or beginning in many major agricultural regions, which means decisions made in the next few weeks will determine harvest volumes months from now.

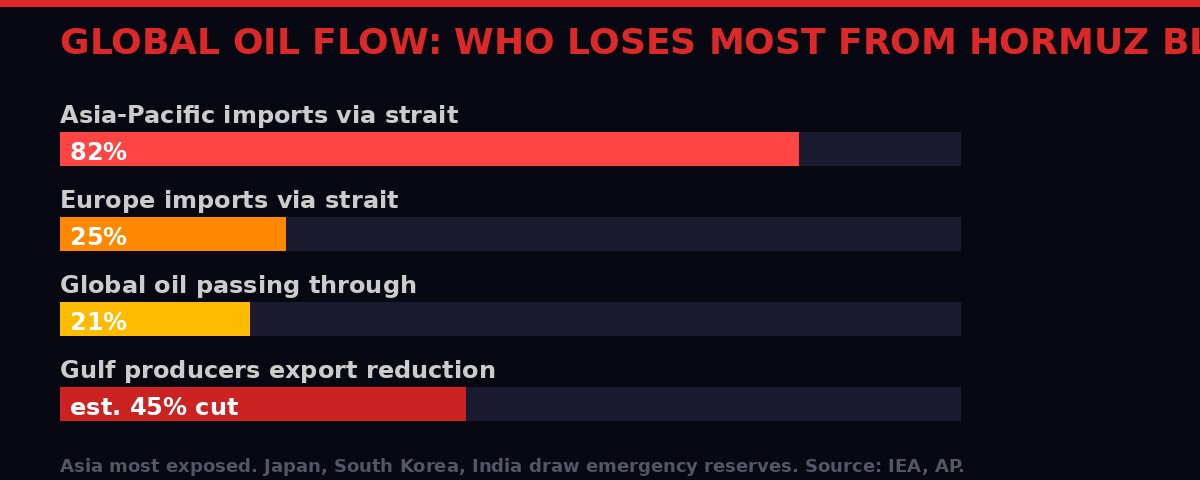

Asia's Exposure - and the Race for Emergency Reserves

No region is more exposed to the Hormuz closure than Asia-Pacific. More than 80% of the oil and LNG that flows to Japan, South Korea, Taiwan, India, and China transits the strait. These are manufacturing economies that run on energy. Their exposure is not marginal - it is structural, baked into decades of supply chain architecture built on the assumption that Persian Gulf oil would always flow. (AP News/IEA data, March 2026)

Japan and South Korea, both almost entirely dependent on imported energy, activated emergency petroleum reserve drawdowns within days of the war's start. India, which has been drawing down its own strategic reserves while simultaneously accelerating talks with Russia for discounted crude that avoids the strait entirely, is navigating one of its most complex energy crises since the 1970s. China, less publicly, has been doing the same - drawing reserves and accelerating pipeline shipments from Russia and Central Asia that bypass the Persian Gulf entirely.

The problem is that strategic reserves are finite. They were designed to buffer disruptions measured in weeks, not months. If the war continues through May or June - which appears increasingly likely given the diplomatic deadlock - several Asian nations will begin to exhaust their buffer capacity. At that point, the choice becomes stark: pay whatever price the market demands, ration supply, or shut down industrial production.

Lutz Kilian, director of the Center for Energy and the Economy at the Federal Reserve Bank of Dallas, is blunt about who loses worst: poorer countries "will be outbid when competing for the remaining oil and natural gas." (AP News, March 2026)

IEA head Fatih Birol laid out the hierarchy of pain in a March 23 statement: wealthy nations can absorb higher prices through subsidies and reserve drawdowns. Middle-income countries face genuine hardship. The poorest countries - those in sub-Saharan Africa, South Asia, parts of Southeast Asia - face rationing, blackouts, and collapsing agricultural output simultaneously. The war is effectively a regressive tax on global poverty.

Stagflation Returns - and the Fed Has No Good Answer

The last time oil prices spiked this sharply for this long, the word that economists reached for was stagflation - the toxic combination of high inflation and stagnating growth that plagued the 1970s and proved extraordinarily difficult to address with conventional monetary policy tools. Central banks can fight inflation by raising interest rates. They can fight recession by cutting them. They cannot do both at once.

Harvard Kennedy School's Carmen Reinhart, a former World Bank chief economist, has flagged exactly this risk: "You're raising the risk of higher inflation and lower growth." (AP News, March 2026)

The Federal Reserve is already walking a tightrope. Inflation data from February - before the full force of the oil shock fed through to consumer prices - came in above forecasts. March data, not yet released, will reflect a partial month of $90-plus oil. April and May data will reflect the sustained $100-plus environment. The Fed's 2% inflation target looks increasingly theoretical.

Meanwhile, the same oil shock that pushes inflation higher is also hitting the real economy. University of Michigan consumer sentiment for March came in below forecasts, with high gasoline prices and war anxiety dragging confidence down. Consumer spending makes up roughly 70% of U.S. GDP. If consumers pull back - as every historical oil shock episode suggests they do - growth will slow even as inflation accelerates. The conditions for stagflation are assembling methodically.

"Historically, oil price shocks like this have led to global recessions." - Christopher Knittel, MIT, to AP News

The grim arithmetic from Gita Gopinath, former IMF chief economist, gives a sense of the scale: if oil averages $85 per barrel for 2026, global growth would be 0.3 to 0.4 percentage points lower than the pre-war forecast of 3.3%. Oil is not averaging $85 - it is at $105 and the war is a month old. The growth hit, under any realistic scenario now, is considerably larger than that estimate. (AP News, March 2026)

For developing economies already carrying heavy debt loads from the COVID era and the earlier commodity shocks of the Russia-Ukraine conflict, a combined inflation-and-recession scenario is potentially destabilizing. Currency pressures, rising import costs, tightening external financing conditions - the cascading effects of a prolonged Persian Gulf war do not need to be managed only by economists. They become questions of political stability.

The $200 Scenario - How We Get There

The $200 barrel figure comes from Macquarie, one of the world's largest commodity trading banks, and it was not offered casually. Macquarie strategists modeled a scenario in which the war extends through late June, the Hormuz passage remains restricted, infrastructure damage accumulates, and no credible peace framework emerges. Under those conditions, they project Brent crude could reach $200 per barrel. (AP News, March 28, 2026)

The current all-time record for oil is just above $147, set during the summer of 2008 when a combination of Iranian missile tests, supply tightness, and surging Chinese demand briefly pushed prices to historic heights - even as the global financial crisis was already beginning to build. That record was set in a world where the Strait of Hormuz was fully open and Iranian exports were flowing. The current situation is categorically more severe.

The pathway to $200 runs through several compounding factors. First, continued Hormuz restriction. Iran has shown it can manage the chokepoint surgically - allowing selected vessels through (it recently agreed to allow 20 more Pakistani-flagged ships to transit), while maintaining enough threat to keep major tanker operators away. This keeps markets in a state of permanent anxiety without giving Washington a clean pretext for a full-scale port seizure operation. (AP News, March 29, 2026)

Second, continued infrastructure destruction. The Ras Laffan strike was the most economically significant single event of the war so far. If similar attacks hit Saudi Aramco's Abqaiq processing facility - as Houthi drones briefly did in 2019 - or Saudi export terminals at Ras Tanura, the supply shock would deepen dramatically. Iran has the missiles and the motivation. The restraint it has shown so far in avoiding maximum infrastructure damage may not last.

Third, Houthi escalation. On Saturday, the Houthis - who control significant portions of Yemen and who targeted Red Sea shipping extensively during the Israel-Hamas conflict - announced their entry into the Iran war proper, launching missiles toward Israeli military sites. If they follow their previous playbook and escalate to broad Red Sea shipping interdiction, the Bab el-Mandeb strait at the southern tip of the Arabian Peninsula would become a second choke point. Any tankers that found ways to exit the Persian Gulf through the Omani coast would face another gauntlet through the Red Sea. (AP News, March 29, 2026)

Ahmed Nagi, senior Yemen analyst at the International Crisis Group, flagged the consequence directly: "The impact would not be limited to the energy market." Disruption of Bab el-Mandeb affects all shipping heading to the Suez Canal - the shortcut that makes European-Asian trade economics viable. A prolonged closure of both choke points simultaneously would reroute virtually all tanker traffic around the Cape of Good Hope, adding weeks and significant cost to every cargo. (AP News, March 29, 2026)

Diplomacy Frozen, Deadline Extended, Markets Unconvinced

The political backdrop to this economic crisis is a diplomatic tableau of maximum confusion. President Trump says talks are "going very well" and that Iran wants to make a deal. Iran's parliament speaker says no negotiations are taking place and that Iran will set American troops "on fire" if ground forces enter the country. Both things cannot be true. Markets have concluded that Trump's version is the unreliable one. (AP News, March 29, 2026)

Trump has twice delayed his self-imposed deadline for Iran to reopen the strait - initially to the end of March, then again to April 6. Iran has not acknowledged any such framework. The pattern of deadline, extension, and continued fighting has convinced investors that the administration does not have a workable end-game strategy in hand. "The administration is winging it," said Rep. Gregory Meeks of New York, the senior Democrat on the House Foreign Affairs Committee. "So how can you trust what the president says?" (AP News, March 28, 2026)

The Islamabad talks on Sunday brought together Saudi, Turkish, and Egyptian foreign ministers in an attempt to open a "direct dialogue" between Washington and Tehran, which have largely communicated through intermediaries throughout the war. Iran agreed at the margins of those talks to allow 20 Pakistani-flagged commercial ships to transit the strait - a tactical concession that keeps pressure on without releasing it. The U.S. and Israel were not present at the Islamabad talks. (AP News, March 29, 2026)

The economic pressure for a resolution is immense. But so far, that pressure has not translated into a credible diplomatic track. The April 6 deadline Trump set for Iran to "fully allow oil tankers to exit the Persian Gulf" - under threat of attacking Iranian energy plants - is now nine days away. Iran's public position has not moved. The Revolutionary Guard is threatening to strike American universities in the UAE and Qatar if the U.S. does not condemn Israeli strikes on Iranian universities by noon Monday. Escalation, not de-escalation, is the operative direction. (AP News, March 29, 2026)

James Jeffrey, a former deputy national security adviser and U.S. ambassador to Iraq, offered a sobering assessment of what has actually been achieved militarily despite the economic cost: "We have not stopped Iran from its campaign against the Gulf. We have not eliminated all of their missiles. And of course, they still have the 400-plus kilograms of highly enriched uranium. It's buried, but still it's there." (AP News, March 29, 2026)

The war is one month old. The economic bill is already historic. The Macquarie $200 scenario is not a base case - it is a warning. But every day the diplomatic deadlock holds, and every missile that strikes another piece of permanent energy infrastructure, that warning becomes marginally more likely to become reality. The strait is still not fully open. The April 6 deadline is coming fast. And the global economy is watching every development with growing alarm.

Key Figures Cited in This Article

- Christopher Knittel - Energy economist, MIT. Quoted via AP News, March 2026.

- Fatih Birol - IEA Executive Director. Statement March 23, 2026, via AP News.

- Carmen Reinhart - Harvard Kennedy School, former World Bank chief economist. Via AP News.

- Gita Gopinath - Former IMF chief economist. Analysis via AP News, March 2026.

- Lutz Kilian - Director, Center for Energy and the Economy, Federal Reserve Bank of Dallas. Via AP News.

- Jim Bianco - President, Bianco Research. Social media post cited by AP News, March 28, 2026.

- Doug Beath - Global equity strategist, Wells Fargo Investment Institute. Via AP News, March 28, 2026.

- James Jeffrey - Former deputy NSA, U.S. ambassador to Iraq. Via AP News, March 29, 2026.

- Ahmed Nagi - Senior Yemen analyst, International Crisis Group. Via AP News, March 29, 2026.

- Rep. Gregory Meeks - Senior Democrat, House Foreign Affairs Committee. Via AP News, March 28, 2026.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram