The $4 Gallon Dividend: How Iran's War Is Accidentally Accelerating the EV Revolution

War rarely advances the green transition. This one might be the exception - not because anyone planned it that way, but because nothing changes consumer behavior like sticker shock at the pump. With US gas prices near $4 a gallon and jet fuel costs having doubled in a month, the Iran conflict has just done what years of climate summits, subsidy programs, and earnest op-eds couldn't quite pull off. The electric vehicle market is surging in ways that look less like a trend and more like a structural break.

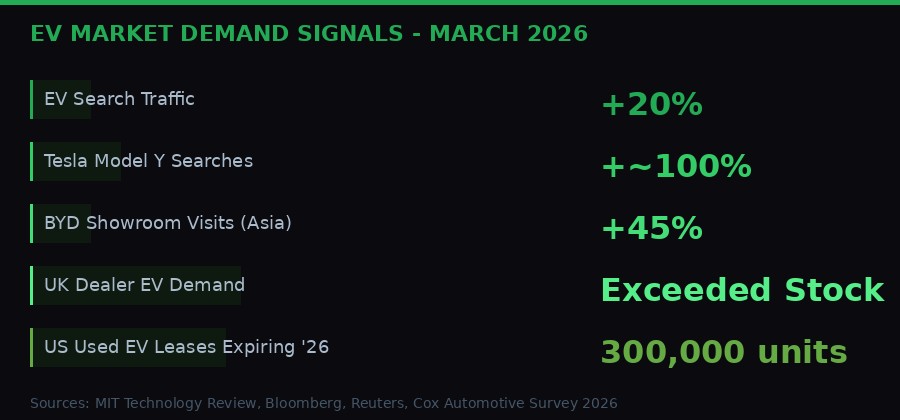

The numbers tell a story that would have seemed optimistic six months ago. Online car marketplaces report EV search traffic up 20% since the initial strikes on Iran in early March, according to reporting by MIT Technology Review. For high-demand models like the Tesla Model Y, traffic nearly doubled. A London car dealership told Reuters it was struggling to keep up with demand and had sent staff to buy vehicles at auction. A dealer outside Manila told Bloomberg it had received a month's worth of orders in two weeks.

This is not a coincidence. This is the price signal doing exactly what economists said it would - once it got high enough, and once people believed the disruption would last.

The Price Threshold Nobody Believed Would Arrive

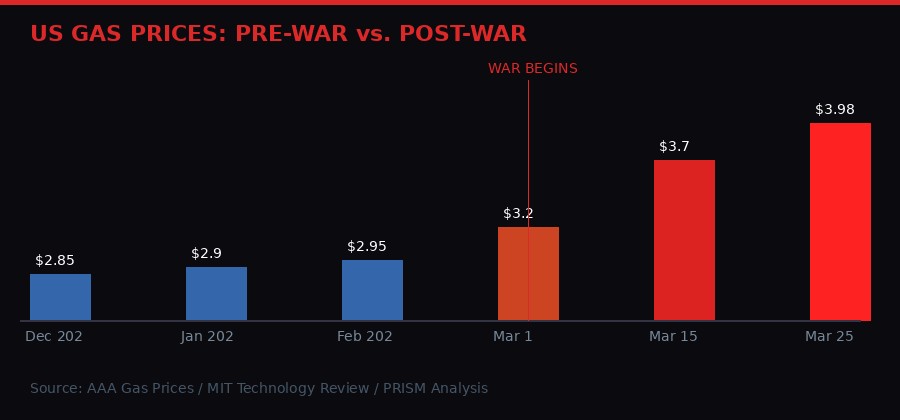

For years, EV advocates pointed to a number: $4 per gallon. That was the threshold at which, according to energy consultancy BloombergNEF data, the total cost of ownership for an electric vehicle becomes comfortably lower than for a comparable gas-powered car - even accounting for higher electricity prices and the upfront premium.

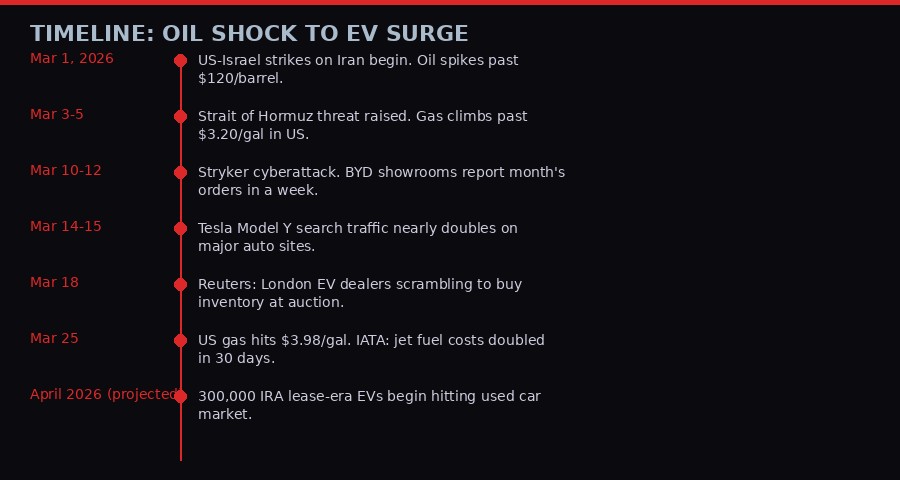

US gas was under $3 a gallon as recently as January 2026. As of March 25, the national average sat at $3.98 per gallon, according to AAA. The Iran conflict, now into its fourth week, has not resolved. If anything, the threat of a prolonged ground war and continued Strait of Hormuz tension makes sub-$3 gas seem like a memory from a calmer era.

A Cox Automotive survey found that most US consumers would seriously consider switching to an EV or hybrid if gas prices hit $6 per gallon. But $4 is clearly moving the needle - search traffic and dealer inquiry data suggest the shift is already underway at current prices, not waiting for a theoretical higher threshold.

The difference this time is durability. The 2022 gas price spike, triggered by Russia's invasion of Ukraine, was real but felt temporary. The Iran conflict involves a country that produces roughly 3% of global oil supply and controls geography that is central to the transit of roughly 20% of globally traded oil. This does not feel like something that resolves cleanly in six weeks.

"If you're in the market for a car, maybe this uncertainty is what you needed to consider electric. But this is also the second big incident of fossil-fuel volatility in the last five years, which could make consumers more ready to make the switch." - MIT Technology Review energy newsletter, March 2026

China Wins the Race It Was Already Winning

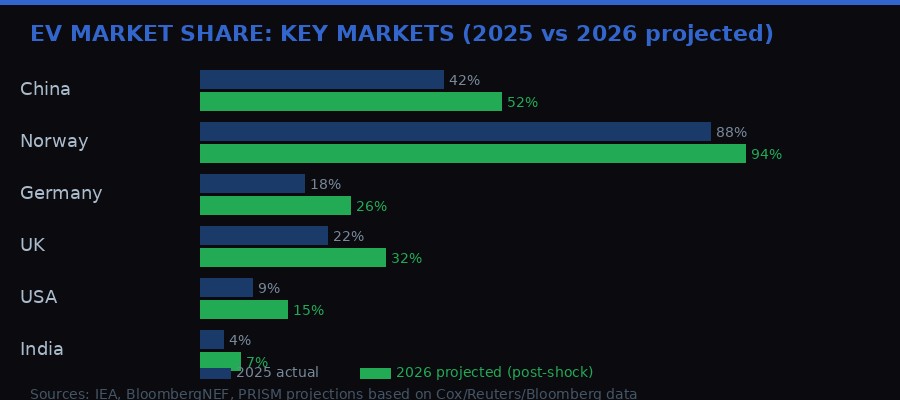

The geography of this surge matters more than any headline number. The countries most exposed to oil price volatility are not necessarily the ones where Tesla holds a commanding position. They are Southeast Asia, South Asia, and parts of Latin America - precisely the markets where Chinese automaker BYD has spent the past three years building distribution networks, service infrastructure, and price points that target the middle class.

Bloomberg reported that BYD showrooms are "bustling across Asia" following the Iran oil shock. One dealer in Manila told Bloomberg it received a month's worth of orders in two weeks. The pattern is repeating across Thailand, Vietnam, Malaysia, and Indonesia - markets where BYD has quietly displaced Japanese brands as the aspirational EV choice and where gasoline dependence is acute because public transit infrastructure is limited.

This matters for the long-term geopolitical map of energy technology. BYD is not just selling cars. It is building loyalty, service networks, and the implicit promise that Chinese battery supply chains are the reliable path to energy independence from Middle Eastern oil. That is a strategic positioning move that pays dividends long after any ceasefire.

Western automakers have a structural problem here. Tesla's dominance in the US and premium European markets does not translate cleanly to price-sensitive emerging markets. Ford, GM, Volkswagen, and Stellantis have all stumbled in their attempts to compete with BYD on cost. The Iran shock has compressed the timeline in which they need to solve this problem. It has also accelerated BYD's lead in markets where the purchasing decision is being made right now, in the next several months, by consumers who are looking at gas prices with genuine alarm.

The Used-EV Wave Nobody Is Talking About

Here is the second-order effect that most coverage of the EV surge is missing: the United States is about to be flooded with affordable used electric vehicles, and the Iran war is arriving exactly when that wave breaks.

In 2022 and 2023, the Inflation Reduction Act's tax incentives triggered a leasing boom. Roughly 300,000 EVs were leased during that period with IRA lease incentives. Those leases are now expiring. Over the course of 2026, those vehicles will come off lease and hit the used car market - many of them in excellent condition, with roughly 36,000 miles on the clock, and selling for significantly less than new models.

The timing is remarkable. A consumer who was on the fence about an EV in January - uncertain about range, uncertain about charging infrastructure, uncertain about the total cost equation - now faces a different set of facts in March. Gas is near $4 a gallon, the war shows no sign of ending, and there are affordable 2022-2023 EVs from reputable manufacturers available at used-car prices. The psychological and financial math has shifted.

This is not a small thing. Used car markets drive volume adoption in ways that new car markets do not. The median US car buyer is not purchasing a new vehicle - they are purchasing a 2-5 year old vehicle. The arrival of a large, affordable used EV cohort at precisely the moment when fuel costs are elevated is an inflection point that is likely to show up clearly in US EV ownership statistics by the end of 2026.

The Used EV Market: Key Numbers

- ~300,000 IRA-era leased EVs set to expire in 2026 (MIT Technology Review)

- Used EV prices down 25-30% from 2022-23 peaks as inventory rises

- 20% spike in overall EV search traffic post-Iran-war-onset (auto marketplace data)

- Tesla Model Y search traffic: nearly doubled after initial strikes on Iran

- UK dealer: scrambling to buy EVs at auction to meet new inquiries (Reuters)

- Manila dealer: month's worth of orders in two weeks (Bloomberg)

The Sectors Bleeding While EVs Surge

The Iran oil shock does not sort neatly into a story about clean energy winners. For every EV buyer celebrating $4 gas as validation of their earlier purchase, there are sectors absorbing punishment that will ripple through supply chains in ways that most consumers will not see coming.

Aviation is the most immediately visible. Jet fuel costs have roughly doubled in the past month, according to the International Air Transport Association. Jet fuel accounts for approximately 25% of an airline's operating costs. The math is brutal: a doubling of fuel costs, even partially offset by hedging, means significant fare increases are coming. Airlines that hedged their fuel costs at pre-war prices have a temporary buffer. Those that didn't are in genuine distress.

Shipping carries a similar problem at larger scale. Fuel accounts for 50-60% of the cost of ocean freight, according to PBS NewsHour reporting. Container shipping rates were already elevated in early 2026 due to Houthi disruptions in the Red Sea. The Iran conflict has added another layer of uncertainty and cost. This passes through to the price of essentially everything that moves by ship - which is most physical goods.

Agricultural supply chains face a compounding problem. Modern fertilizer production requires natural gas as a feedstock for ammonia synthesis. Natural gas prices in Europe have climbed significantly since the war began - the continent is particularly exposed because its transition away from Russian gas left it dependent on LNG imports that price off global oil market movements. Higher natural gas prices mean higher fertilizer prices, which means higher food production costs. That signal will not appear in supermarket prices immediately, but it will appear by late 2026 or early 2027.

The counterintuitive risk for EVs themselves: if the oil shock causes a significant recession, it becomes harder to finance major purchases including new electric vehicles. Interest rates that are already elevated in the US act as a headwind for any financed purchase. The transition to electric vehicles is much easier in a growing economy than in a contracting one. The enthusiasm in showrooms today may face a more complicated backdrop six months from now if global growth forecasts continue to be revised downward.

The Battery Supply Chain Bottleneck

A demand spike is only as good as the supply chain behind it. The EV surge triggered by the Iran oil shock runs directly into the structural limitation that has constrained EV scaling for the past three years: battery supply.

The global lithium-ion battery supply chain is heavily concentrated. China's CATL produces roughly 37% of the world's EV batteries. Add in LG Energy Solution, Panasonic, and Samsung SDI, and the top four manufacturers account for roughly 70% of global supply. BYD manufactures its own batteries, giving it a vertical integration advantage that most Western automakers lack entirely.

A sudden 20-40% increase in EV demand cannot be absorbed by the existing supply chain without creating shortages, lead time extensions, and price increases for battery packs. This is not a new problem - it surfaced during the 2022 EV boom - but the Iran shock has arrived before Western automakers completed their planned battery supply buildout.

The US government's push to develop domestic battery manufacturing through the IRA's cell production tax credits has produced real results: new factories in Georgia, Michigan, and Tennessee from companies like SK On, Panasonic, and a joint venture between GM and LG Energy Solution. But these facilities are still ramping up, and their combined output does not yet match what would be needed to service a sustained demand surge of the scale that oil price economics might generate.

Lithium, cobalt, and nickel prices - which had stabilized or declined after the 2022 peak - are already beginning to reflect renewed demand pressure. Lithium carbonate prices on the Shanghai Futures Exchange have begun climbing from lows reached in late 2025. If the Iran conflict persists for months, battery input costs will add to the complexity of an EV market that was only just beginning to reach genuine mass-market price parity.

The Charging Infrastructure Race

Every time a consumer considers switching to an EV, the mental model runs through the same checklist: range, charging availability, charging speed, and the question of whether they can charge at home. The oil shock accelerates the demand side of this equation. The charging infrastructure side moves at its own pace.

The United States had approximately 170,000 public charging ports as of early 2026, according to the Department of Energy's Alternative Fuels Station data. Tesla's Supercharger network remains the gold standard for reliability and speed. The CCS (Combined Charging System) standard, adopted by most non-Tesla manufacturers following Ford and GM's decision to switch to NACS connectors, has improved interoperability but has not uniformly improved the experience of charging at non-Tesla stations.

The tension is acute for people who cannot charge at home - apartment dwellers, renters without dedicated parking, urban residents in dense housing. These are not edge cases. According to the US Census Bureau, roughly 36% of Americans rent their homes. A significant portion of renters live in multi-unit buildings where home charging installation is complicated or impossible. For these consumers, public charging infrastructure is not a convenience - it is the deciding factor.

The Biden administration allocated $7.5 billion for EV charging infrastructure through the Infrastructure Investment and Jobs Act. As of early 2026, roughly $2.1 billion of that had been deployed, building out a National Electric Vehicle Infrastructure corridor program. The funding exists. The buildout has been slower than advocates hoped, hampered by permitting delays, utility interconnection queues, and the plain difficulty of installing high-power electrical equipment at scale across a country the size of the United States.

"The interest is there, but what would it really take for more drivers to make the switch? Nice, round numbers do tend to get people's attention." - MIT Technology Review, March 2026, on the $4/gallon threshold

The Iran shock accelerates the demand signal but does not automatically unlock the charging infrastructure supply. This mismatch - more people wanting EVs than there is charging infrastructure to serve them comfortably - is the friction point that could moderate the conversion rate even as price economics strongly favor the switch.

The Second Space Race, The Second Oil Crisis

The 1970s oil crisis - triggered by the Arab oil embargo of 1973 - left a structural mark on the global economy that lasted decades. It ended the era of cheap American gasoline, triggered a recession, and eventually produced a shift toward more fuel-efficient vehicles. Japanese automakers, whose smaller, more fuel-efficient cars were better suited to the new reality, gained a market share advantage over US manufacturers that they never fully relinquished.

MIT Technology Review drew this parallel explicitly in its March 2026 coverage: "Historically, this is exactly the sort of moment that's pushed people to reevaluate how they get around." The 1973 crisis did not kill oil dependency - it took another fifty years and a genuine technology shift to get to this point. But it did reshape consumer preferences and competitive positioning in ways that became visible only in retrospect.

The current moment has a different character than 1973. The alternative - electric vehicles - is actually available at scale, at competitive prices, with functioning infrastructure. In 1973, there was no viable alternative. Consumers who wanted to reduce gasoline dependence could buy a more fuel-efficient car, or they could drive less. Now they can switch to a fundamentally different technology platform.

The second-order effect on the broader energy transition may be even more significant than the direct EV surge. The Iran conflict has demonstrated, in the starkest possible terms, the geopolitical risk premium embedded in fossil fuel dependency. Governments across Europe, Asia, and North America are watching oil prices, watching energy security calculations, and updating their assessments of how quickly they need to accelerate the transition away from oil imports. That recalibration happens at the level of national policy, corporate strategy, and individual consumer behavior simultaneously.

Grid-scale battery storage, offshore wind, solar farms - all of these are seeing renewed investment interest as the cost of the fossil-fuel alternative becomes dramatically more visible. The International Energy Agency had projected that fossil fuel demand would peak before 2030 under base-case scenarios. The Iran conflict has not changed that projection numerically, but it has changed the confidence with which investors, policymakers, and consumers believe the projection. Events that seemed probabilistic now feel more certain.

What Comes Next: The Three Scenarios

The trajectory of the EV surge depends heavily on how the Iran conflict resolves - or fails to resolve. Three scenarios are worth mapping.

Scenario One: Rapid Ceasefire, Oil Normalizes

If the Iran conflict ends within weeks and oil prices return to pre-war levels, the current EV search surge will likely moderate. Consumer behavior follows price signals, and if the immediate pain dissipates, so does some of the urgency. However, the 300,000 used EVs coming off lease will still hit the market, and the awareness that this disruption is possible will not fully fade. Some conversion rate acceleration persists, but the burst moment passes.

Scenario Two: Prolonged Conflict, $4-5 Gas for Six Months

This scenario, which looks increasingly likely given the trajectory of the conflict as of late March, produces a significant structural shift. Consumers who were planning a 2027 car purchase accelerate the decision. Fleet operators - commercial vehicles, delivery trucks, ride-share - make EV transitions based on operating cost math that now clearly favors electric. Charging infrastructure investment accelerates because the business case strengthens with every week gas stays expensive. This is the scenario in which 2026 becomes a genuine inflection year for US EV market share.

Scenario Three: Escalation, $6+ Gas and Economic Contraction

The most disruptive scenario. Gas above $6 would likely push a significant share of marginal buyers toward EVs, but simultaneously trigger the economic conditions that make financing a major purchase difficult. This is the paradox of extreme price signals: they clarify the case for switching even as they undermine the financial conditions that enable the switch. This scenario likely produces a more chaotic EV market - high demand, constrained supply, significant battery price pressure, and an uneven adoption that favors wealthier buyers with home charging capability.

What all three scenarios share: the Iran conflict has compressed the timeline. Choices that consumers and companies were planning to make in 2027-2029 are being forced into 2026. That compression has real economic and geopolitical consequences regardless of how oil prices settle.

The clean energy transition has always been a race between technology cost curves and the political will to move fast enough. The Iran conflict has injected something different: the raw urgency of a price signal that everyone can read at a glance every time they stop for gas. That is a crude instrument. But crude instruments, applied with sufficient force, move mountains.

The $4 gallon dividend is real. Whether it compounds into something permanent depends on whether the infrastructure, the supply chains, and the financial conditions can catch up to the demand signal that a war has accidentally created.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram