Liberation Day, One Year Later: The $3.2 Trillion Experiment That Broke American Manufacturing

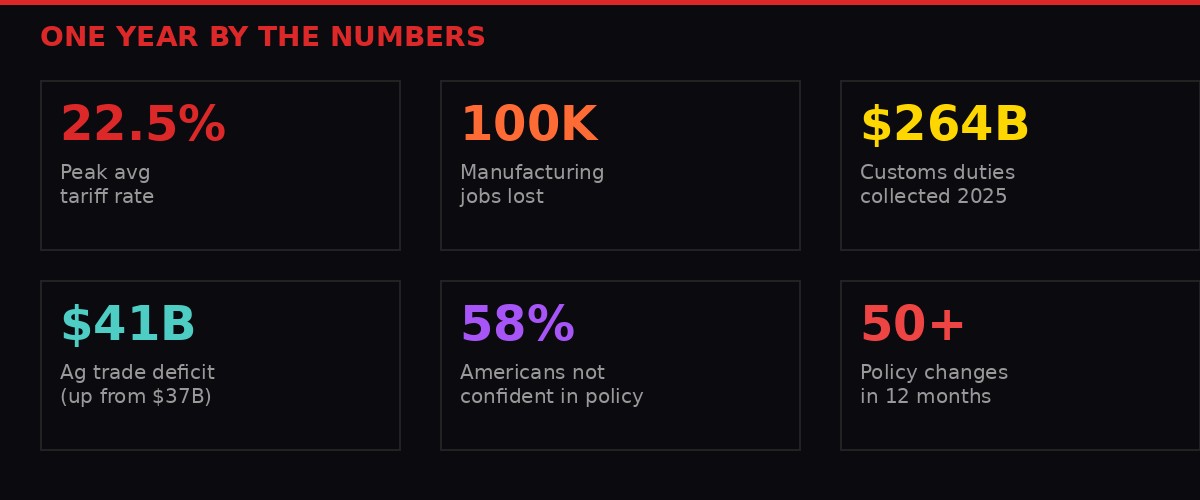

One year ago today, President Donald Trump stepped into the Rose Garden and declared April 2, 2025, a date that would "forever be remembered as the day American industry was reborn." He called it Liberation Day. He promised trillions in revenue, a manufacturing renaissance, cheaper consumer goods, and an end to the trade deficit that he framed as a national emergency. He signed an executive order imposing sweeping reciprocal tariffs on virtually every U.S. trading partner, raising the average tariff rate to 22.5% - the highest since before World War I.

Twelve months later, the data is in. The manufacturing sector shed 100,000 jobs. The trade deficit hit an all-time high. The Supreme Court struck down the tariffs in a 6-3 ruling. And American households paid an estimated $1,000 more for everyday goods, according to analysis from the Yale Budget Lab and other independent economists. The promises of Liberation Day did not just fall short. They inverted. Every major metric the administration cited as justification for the tariffs moved in the wrong direction.

This is the definitive accounting of what happened.

The Promise: What Trump Said Would Happen

The executive order that launched Liberation Day was titled "Regulating Imports with a Reciprocal Tariff to Rectify Trade Practices that Contribute to Large and Persistent Annual United States Goods Trade Deficits." The name alone telegraphed the theory: persistent trade deficits constituted a national emergency, and tariffs were the cure. Trump invoked the International Emergency Economic Powers Act (IEEPA) - a law designed for sanctions during genuine national emergencies - to impose tariffs without Congressional approval. It was the first time IEEPA had ever been used this way.

The president's promises were sweeping and specific. He claimed the tariffs would "make Americans wealthy." He predicted "trillions and trillions of dollars" flowing into the Treasury to pay down national debt. He said "jobs and factories will come roaring back." He asserted that increased domestic production would "lower prices for consumers." His trade advisor Peter Navarro estimated the tariffs would generate $600 billion annually. Trump himself cited between $6 trillion and $18 trillion in new foreign direct investment.

The plan appeared straightforward on the surface: charge each trading partner the same tariff rate they charged the United States. But the Tax Foundation's analysis revealed that the actual tariffs bore no resemblance to reciprocity. The U.S. Trade Representative's office didn't use observed foreign tariff schedules at all. Instead, they converted each country's bilateral goods trade balance into a synthetic tariff rate with a 10% floor. Because bilateral trade balances don't measure trade barriers, the resulting tariffs had, in the Tax Foundation's words, "no relationship with other countries' trade barriers" (source: Tax Foundation, April 2026).

Within days, an escalation with China sent the U.S. tariff rate on Chinese goods to 125%. Country-specific rates on other partners were paused for 90 days. In the months that followed, tariff policy changed more than 50 times - rate increases, decreases, product exemptions, product inclusions, and temporary carve-outs that created a moving target no business could plan around.

The Manufacturing Collapse Nobody Predicted

The stated purpose of Liberation Day was to revive American manufacturing. The executive order explicitly cited the "decline of U.S. manufacturing capacity" as a threat to the economy and national security. What followed was the opposite of revival.

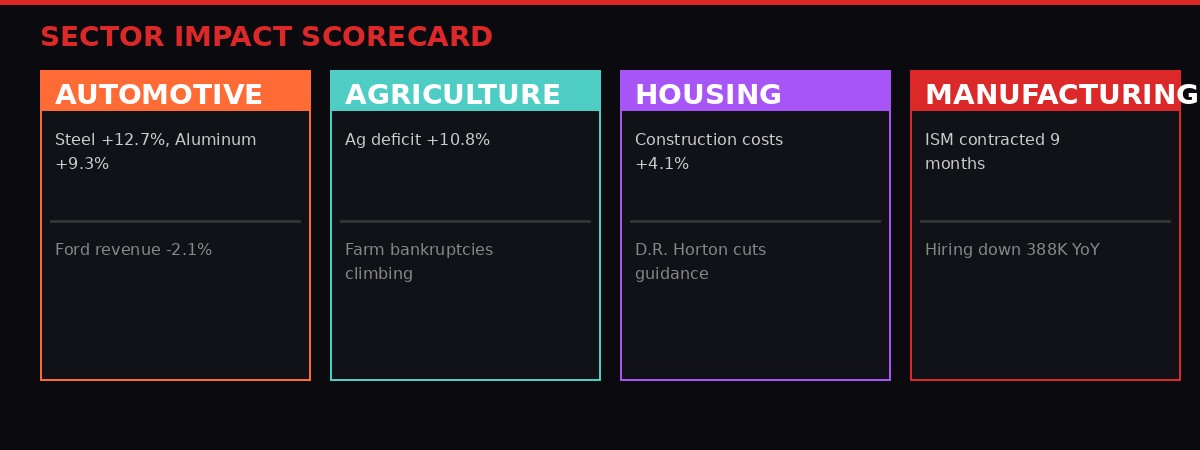

According to Bureau of Labor Statistics data, the U.S. manufacturing sector shed 100,000 jobs between January 2025 and April 2026 (source: FRED/BLS MANEMP series). The ratio of manufacturing workers to total nonfarm employment fell to its lowest point since 1939 - the earliest year the BLS tracks this metric. U.S. manufacturers hired 388,000 fewer workers in 2025 than in 2024. The ISM Manufacturing Index, a monthly survey of purchasing managers, showed manufacturing contracting for nine consecutive months after Liberation Day before a marginal rebound in January and February 2026 (source: National Taxpayers Union, April 2026).

The Hague Centre for Strategic Studies (HCSS) published a detailed analysis showing that construction spending on new industrial projects fell 11.1% between April and December 2025. Private fixed investment in manufacturing declined 4.6% over the same period. These are the two metrics that would rise first if tariffs were successfully redirecting capital toward domestic production. Both fell (source: HCSS, April 2026).

Why? Over half of U.S. imports in 2025 were industrial supplies or capital goods - the raw materials and components American factories need to operate. Tariffs on steel raised the average cost per vehicle by 12.7%. Aluminum costs climbed 9.3%. Ford reported a 2.5% increase in raw material costs in Q1 2026, directly attributable to tariffs, and warned that continued pressure could hurt U.S. auto sales. The tariffs designed to protect manufacturers instead taxed their inputs, making it harder and more expensive to build things in America.

"The tariffs are a classic example of unintended consequences. While the stated goal was to protect domestic industries, the reality is that they've increased costs for everyone, from businesses to consumers. The net effect is a drag on economic growth."- Dr. Anya Sharma, Chief Economist, Global Investment Strategies (via Archyde)

The automotive sector bore the heaviest burden. Ford's revenue declined 2.1% year-over-year in Q1 2026. Net income dropped 15.8%. The company's forward P/E ratio compressed to 8.2x as investors priced in continued margin erosion. D.R. Horton, the largest U.S. homebuilder, saw construction costs rise 4.1% and lowered its full-year guidance, citing "unforeseen cost pressures" from tariffs. The housing market - already strained by elevated interest rates - absorbed another layer of pain from tariffed lumber, drywall, and steel.

The Trade Deficit: Record Highs Instead of Decline

The trade deficit was the core justification. Trump's executive order literally described persistent goods trade deficits as a "national emergency." The tariffs were supposed to be the remedy. On March 25, 2026, the Bureau of Economic Analysis reported that the U.S. goods trade deficit increased to an all-time high in 2025 (source: NTU, April 2026).

This outcome was not a surprise to economists. Tariffs reduce the growth of both imports and exports, with no definitive impact on the overall trade balance. When you tax imports, you also make exports less competitive - your manufacturers pay more for inputs, your currency appreciates from reduced import demand, and retaliatory tariffs from trading partners close off export markets. The net effect on the deficit is typically negligible, or in this case, negative.

Agriculture was particularly devastated. The agricultural trade deficit climbed from $37 billion in 2024 to $41 billion in 2025 - a 10.8% increase despite tariffs supposedly protecting American producers. Farmers and ranchers faced a double hit: lower exports as retaliatory tariffs closed off foreign markets, and higher input costs as tariffed farm machinery and agricultural chemicals added $958 million in costs between February and October 2025 alone (source: USDA Foreign Agriculture Service).

The country's leading farm organizations sent Congress a letter warning: "America's farmers, ranchers, and growers are facing extreme economic pressures that threaten the long-term viability of the U.S. agriculture sector. An alarming number of farmers are financially underwater, farm bankruptcies continue to climb, and many farmers may have difficulty securing financing to grow their next crop" (source: American Farm Bureau Federation).

The Peterson Institute for International Economics estimated that tariffs contributed a 0.3% increase to core inflation, partially offsetting the Federal Reserve's aggressive rate-hiking campaign. Analysis published by Archyde cited a 0.8% increase in the Consumer Price Index directly attributable to tariffs. A separate Scripps News analysis found that the average American household paid approximately $1,000 more for goods in 2025 due to tariff-driven price increases (source: Scripps News).

The Supreme Court Smackdown

The legal challenge to Liberation Day began almost immediately. On May 28, 2025, the United States Court of International Trade ruled in Learning Resources, Inc. v. Trump that the president had overstepped his authority by using IEEPA to impose tariffs. The court found that the emergency powers statute was not designed to regulate international trade through import taxes and ordered the Liberation Day tariffs vacated.

The government appealed. On August 29, 2025, the Federal Circuit Court of Appeals upheld the lower court's ruling. The case moved to the Supreme Court, which heard oral arguments on November 5, 2025 - election day in a remarkable coincidence of timing.

On February 20, 2026, the Supreme Court handed down its decision: 6-3, the tariffs were unconstitutional. The court found that IEEPA did not authorize the imposition of tariffs, which fall under Congress's Article I power to regulate commerce. The ruling effectively nullified the Liberation Day tariffs and the 25% "Border Security" tariffs on goods from Mexico, Canada, and China (source: BBC News).

Hours after the ruling, the Trump administration pivoted. The president imposed a new global 10% tariff under the Trade Act of 1974, which has a 150-day statutory limit. Trump has suggested raising that tariff to 15%, but any extension beyond the 150-day window requires Congressional approval - something the administration has not secured and faces significant opposition to obtaining.

The immediate aftermath triggered the complex process of refunding tariffs already collected. The Court of International Trade ordered Customs and Border Protection to begin returning payments to importers. The first phase covers an estimated $120 billion in refunds. Kyle Peacock, principal at Peacock Tariff Consulting, noted the complications: "We may see a wave of litigation from consumers to retailers, but retailers haven't received the funds yet. Even if they were going to pass it back to consumers, it's this vicious cycle" (source: Telemundo/Scripps).

The Tax Foundation tallied the total revenue collected under the IEEPA tariffs before the court ruling: approximately $166 billion. All customs duties combined brought in $264 billion from January through December 2025, accounting for 4.9% of total tax receipts. That is a far cry from the $600 billion per year Navarro predicted, and federal debt continued growing throughout the period (source: Tax Foundation).

The Investment Mirage

Throughout the year, President Trump claimed eye-popping foreign investment figures - starting at $6 trillion and eventually reaching $18 trillion. The Tax Foundation tracked the actual data from the Bureau of Economic Analysis. In 2025, foreign direct investment into the United States totaled $288.4 billion. That figure is more than an order of magnitude below the president's claims, and it actually represents a decline from recent history: below the prior 10-year average of $320.7 billion, and lower than the annual totals in 2021 ($405.5 billion), 2022 ($338.4 billion), 2023 ($297.4 billion), and 2024 ($292.3 billion).

Various firms and countries did announce pledges to increase U.S. investment. But pledges and ribbon-cutting photo opportunities are not the same as capital flows. The macroeconomic data shows no dramatic spike, no inflection point, no evidence of a tariff-driven investment boom. The volatility itself - 50-plus policy changes in 12 months - likely suppressed investment rather than encouraging it.

"Uncertain tariff policy has been very paralyzing to some companies over the last year."- Matt Notowidigdo, University of Chicago economist (via Marketplace)

PYMNTS Intelligence, which tracked the impact on middle-market firms throughout the year through its Certainty Project, documented the progressive erosion of business confidence. In March 2025, 22% of CFOs reported operating in high uncertainty. By April, that figure rose to 33% among goods product leaders, and confidence in managing supply chain disruption collapsed from 40% to just 5% in a single month. By fall, 35% of goods CFOs still reported high operational uncertainty, and only 41% expected improvement over the following year (source: PYMNTS Intelligence, April 2026).

The data shows a clear behavioral shift. By November 2025, nearly three in four CFOs had changed their investment strategies. Goods firms were 46% more likely to prioritize caution over growth. Forty percent identified delaying planned investments as their primary response to tariffs. By year end, 35% of CFOs cited risk management and compliance as their top focus, while 30% prioritized supply chain resilience. Only a small minority still emphasized new products or market expansion. The tariffs did not cause businesses to invest more aggressively in America. They caused businesses to hunker down and wait.

The divergence between firms with domestic and international supply chains became stark. Only one in five firms with heavy reliance on international suppliers reported a good year, compared to nearly two-thirds of firms with limited foreign exposure. Among heavily exposed firms, 91% reported weaker B2B demand and 86% reported weaker B2C demand. Companies with international supply chains saw average revenue decline 6% over 12 months. The tariffs created a clear dividing line between winners and losers - and the losers were disproportionately the globally integrated manufacturers the policy was supposed to strengthen.

Public Opinion Turned Against It

As the economic costs accumulated, public opinion shifted measurably. Pew Research Center released a comprehensive survey on April 1, 2026, based on responses from 3,507 adults collected between March 23 and 29. The findings were stark: 58% of U.S. adults expressed little or no confidence that Trump could make good decisions about trade policy. A higher figure, 63%, expressed little or no confidence in his handling of tariff policy specifically (source: Pew Research Center, April 2026).

The partisan divide remains enormous. Among Republicans and Republican-leaning independents, 74% expressed confidence in Trump on trade. Among Democrats and Democratic leaners, just 12% did. But the more telling movement happened within Republican ranks regarding the specific question of which country benefits more from trade relationships. In 2025, 46% of Republicans said Canada benefited more from U.S.-Canada trade. By 2026, that number dropped to 36%. The same decline appeared for Mexico. Republicans themselves became less certain that the trade relationships were as one-sided as the administration claimed.

Across both parties, uncertainty itself grew. When asked about U.S.-Canada trade, the share of respondents who said they simply weren't sure which country benefits more rose from 16% to 22% among Republicans and from 16% to 25% among Democrats. The tariff debate did not clarify trade for the public. It confused people further.

Congresswoman Suzan DelBene of Washington's 1st District captured the opposition's framing in a statement marking the anniversary: the tariffs' one-year mark is defined by "higher prices and a weaker economy" (source: KOMO News). Democrats are increasingly weaponizing tariff backlash in campaigns heading into the 2026 midterms, framing the policy as a tax on consumers that enriched no one.

The Global Fallout and What Comes Next

The Liberation Day tariffs did not operate in isolation. They intersected with an active shooting war in the Middle East that sent oil prices surging, a Federal Reserve navigating persistent inflation, and a stock market already under pressure. The S&P 500 declined more than 7% in Q1 2026, its worst quarter since 2022. UK manufacturers reported the biggest jump in cost inflation since Black Wednesday in 1992. The global manufacturing ecosystem absorbed synchronized shocks from multiple directions, and Liberation Day was one of the largest.

The Supreme Court ruling resolved the constitutional question but not the economic damage. The 150-day Trade Act tariff creates a ticking clock. Congress must act to extend or replace it, and there is no consensus. The refund process will take months, possibly years, to complete. Supply chains reorganized during the tariff period will not snap back to their pre-2025 configurations. Relationships with trading partners - particularly China, Canada, and Mexico - carry scar tissue that no court ruling can remove.

The HCSS analysis offered a particularly sobering assessment for Europe: despite the tariffs' failure to revive American manufacturing, EU leaders are increasingly comfortable with their own tariff proposals. EU Trade Commissioner Sefcovic has argued for making it easier within the WTO to raise tariffs. A senior French government official floated a general European tariff of 30% on all Chinese products. The American experiment did not discourage imitators. If anything, it normalized the instrument.

For American businesses, the shift from growth to defense may prove the most lasting consequence. When nearly three-quarters of CFOs change their investment strategies in a single year, that does not reverse overnight. PYMNTS Intelligence found that by September 2025, 48% of product executives viewed tariffs as a long-term U.S. policy direction - not a temporary shock. By December, 88% still expected supply chain disruptions ahead. The uncertainty is baked in.

"We haven't seen a lot of relief. In fact, we saw tariffs drive up consumer goods' prices by another 2% or so over the last year, and estimates are that somewhere between 90 and 95% of the tariff actual cost is essentially being passed on to consumers."- Jonathan Ernest, Assistant Professor of Economics, Case Western Reserve University (via Telemundo/Scripps)

Rathna Sharad, CEO of shipping platform FlavorCloud, put the manufacturing question bluntly: "The expertise isn't there, number one. Number two, the labor costs are nowhere near trying to do that manufacturing in some of these other countries that they currently use." Tariffs cannot conjure a workforce, a supply chain, or an industrial ecosystem into existence through price signals alone. That requires decades of investment in education, infrastructure, and institutional capacity - none of which a tariff executive order can provide.

The National Taxpayers Union concluded its anniversary analysis with an epitaph: "One year after Liberation Day, the evidence is in: tariffs failed even by the Trump Administration's own terms. They did not shrink the trade deficit, did not revitalize manufacturing, and did not help farmers. It would be a mistake to replace one set of failed tariffs with another."

Yale professor Odd Arne Westad, a historian of great-power competition, offered the broader frame: the United States has faced enormous challenges over the past decade. In a multipolar world, the path forward runs through cooperation, not the kind of economic unilateralism that Liberation Day embodied (source: CGTN, April 2026).

Today, April 2, 2026, marks an anniversary. Markets are open. Futures are sliding - the Dow, S&P 500, and Nasdaq all pointing lower as the Iran war continues to roil energy prices and the tariff anniversary reminds investors of the policy whiplash that defined 2025. The 150-day clock on the current 10% tariff is ticking. Congress has made no move to extend it. No comprehensive trade legislation is on the floor. No manufacturing renaissance has materialized.

The experiment ran. The results are in. Liberation Day liberated nothing except American businesses from certainty, American farmers from profitability, and American consumers from their purchasing power.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram