$17 in 20 Minutes: The Full Market Anatomy of Trump's Hormuz Tweet

Brent crude swung from $113 to $96 in less than half an hour on a single Truth Social post. UK gilt yields hit their highest since 2008. Asia had already bled out. Here is every number that moved on Day 24 - and why none of it is over.

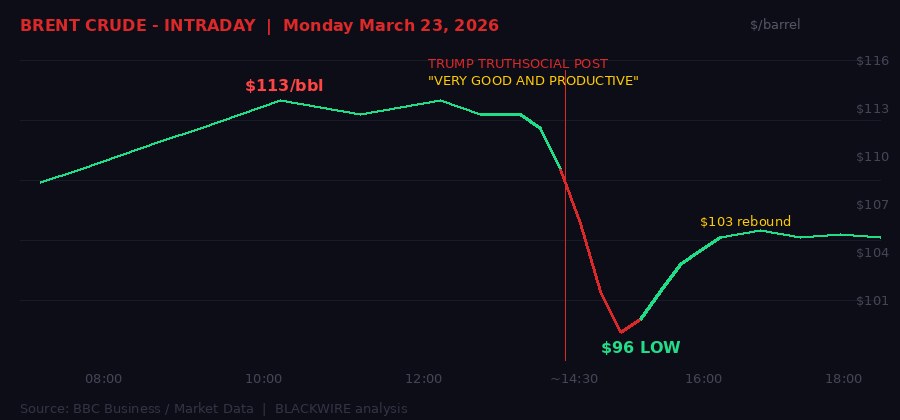

Brent crude's single-session swing on March 23 was one of the largest intraday moves in oil market history. BLACKWIRE graphic.

At approximately 14:20 UTC on Monday, Donald Trump posted four words on Truth Social that moved a commodity worth $7 trillion annually by fifteen percent. "VERY GOOD AND PRODUCTIVE." That was all it took.

Brent crude was trading at $113 a barrel when the post landed. Within twenty minutes, it crashed to $96 - a $17 swing in a market that normally moves by fifty cents on a busy day. By the time European markets closed, it had settled at approximately $103, still down sharply from the morning high but nowhere near its intraday bottom.

But the tweet had a problem. It was immediately denied by the other party. Iran's foreign ministry issued a flat contradiction within the hour: "We deny what US President Donald Trump said regarding negotiations taking place between the United States of America and the Islamic Republic of Iran." Tehran said there had been no talks. No calls. Nothing.

Markets had moved $17 on a claim that was flatly disputed by its subject. Welcome to Day 24 of the Iran War - where geopolitical risk has become a volatility generator unlike anything since 1973.

Brent crude intraday: From $108 open to $113 peak, then a $17 vertical drop to $96 on the Trump tweet, rebounding to $103. BLACKWIRE chart.

The Asia Session: Blood Before the Tweet

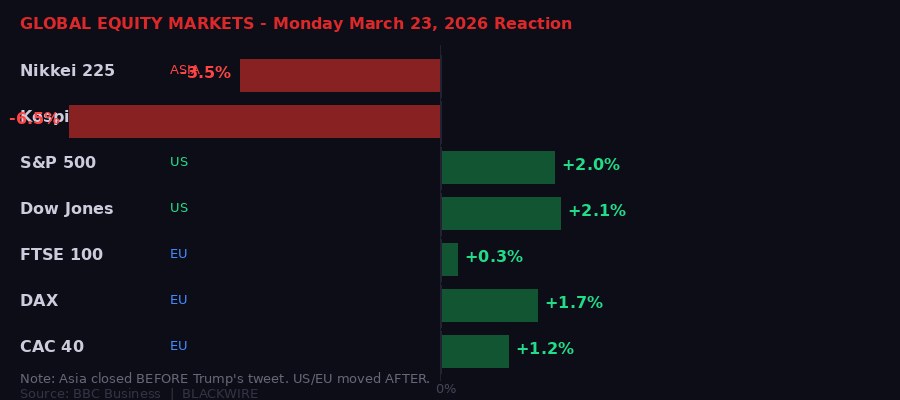

What made Monday's volatility so significant is that the worst of it happened before Trump's post - in Asian markets that closed hours before Wall Street opened.

Japan's Nikkei 225 dropped 3.5%. South Korea's Kospi fell 6.5%. Both indices closed before Trump's Truth Social post changed the narrative. Asian investors were pricing a war with no off-ramp - the version of reality where Trump threatened on Saturday to "obliterate" Iranian power plants if the Strait of Hormuz wasn't reopened within 48 hours, and Tehran responded by threatening to target US-linked energy sites across the Gulf region.

The Kospi's 6.5% single-day loss is staggering in context. South Korea is one of the most oil-import-dependent economies in the world, processing roughly 2.7 million barrels per day. The Strait of Hormuz is not an abstraction for Seoul - it is the artery that feeds their industrial economy. Every $10 increase in the price of oil costs South Korea approximately $4 billion per year in additional import bills. Brent has risen roughly $40 from pre-war levels. Do that math.

Before Trump's tweet arrived, London's FTSE 100 was down more than 2% on the day. European markets had opened in deep red, with energy-intensive industries - chemicals, airlines, logistics - taking the hardest hits. The DAX was down over 2%. The CAC was off similar amounts.

Then the post hit. And everything reversed.

Asia bled out before the tweet. US and EU reversed sharply after it. The divergence tells you everything about information asymmetry. BLACKWIRE chart.

The Tweet Anatomy: What Trump Actually Said

The full Truth Social post, published around 14:20 UTC Monday, read as follows: Trump said that over the past two days the US and Iran had held "VERY GOOD AND PRODUCTIVE" talks over "A COMPLETE AND TOTAL RESOLUTION OF OUR HOSTILITIES," and that he had instructed the Department of War to postpone any military strikes "AGAINST IRANIAN POWER PLANTS AND ENERGY INFRASTRUCTURE FOR A FIVE DAY PERIOD, SUBJECT TO THE SUCCESS OF THE ONGOING MEETINGS AND DISCUSSIONS."

"Any reports of productive talks are welcome. We have always said a swift resolution to the war is in the global interest and the Strait of Hormuz specifically needs to be re-opened."

- Downing Street spokesperson, Monday March 23

On its face: a de-escalation. Markets read it as a ceasefire preview and sold oil futures hard. The interpretation was rational given the stakes - if a deal was genuinely in progress, the Hormuz blockade could lift, unlocking roughly 20 million barrels per day of stranded supply back into global markets.

But Iran's foreign ministry statement - issued within the hour - created a fundamental credibility problem. Either Trump was lying about talks that never happened. Or Iran was lying to maintain domestic hardline credibility. Or there were back-channel communications that neither side is publicly acknowledging.

Markets chose to believe Trump, at least partially. Oil stayed below its morning peak. But the rebound from $96 to $103 showed traders were not fully buying the resolution narrative either. $103/barrel is not a "ceasefire premium." It is still crisis pricing. Before the war began on February 28, Brent was trading around $72.

Susannah Streeter, chief investment strategist at Wealth Club, told the BBC: "Clinging to President Trump's words is fraught with risks, given how hopes have already risen and then been dashed over the last four weeks." She noted that with oil still above $100 a barrel, "energy costs will remain super-painful for companies and consumers."

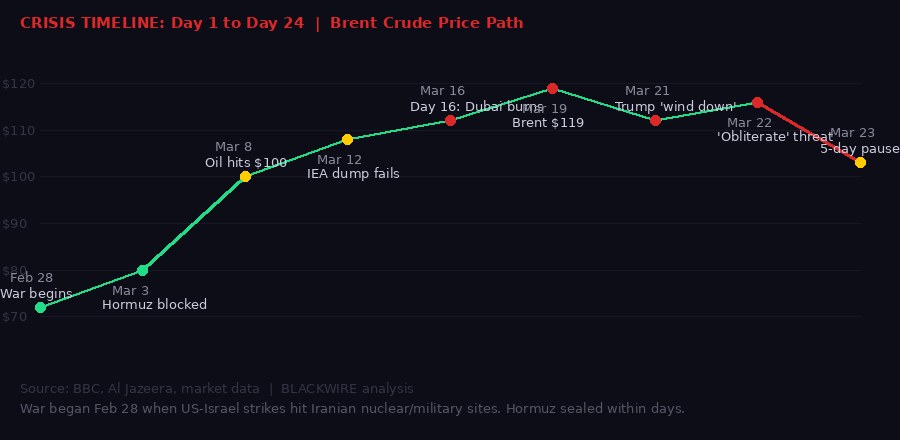

The 24-day path from $72 pre-war to $119 peak - with every major escalation and reversal marked. Today's $103 is not a resolution - it is barely a retracement. BLACKWIRE chart.

UK Gilt Yields: When the Bond Market Screams 2008

The headline that did not get enough attention on Monday: UK 10-year gilt yields touched 5.12% in early trading - the highest level since the 2008 financial crisis.

Government bond yields rising means investors are demanding more return to hold sovereign debt. When UK yields surge, it signals that markets view UK government finances as increasingly risky - which they are. The Iran war has created an energy price shock that is punching a hole through the UK fiscal position in real time.

The mechanics are direct. Higher oil and gas prices mean higher energy import bills for UK households and businesses. Higher energy bills mean lower consumer spending on everything else. Lower growth means lower tax receipts. Lower tax receipts mean higher deficits. Higher deficits mean the government needs to borrow more. More borrowing demand with nervous lenders means higher yields. Higher yields mean the cost of servicing existing debt increases. And so on.

This is not a theoretical spiral - it is happening in real time. UK Prime Minister Keir Starmer convened an emergency COBRA committee on Monday afternoon, with Bank of England governor Andrew Bailey and the chancellor both in attendance. Housing Minister Matthew Pennycook mentioned the government was assessing options including action on "profiteering that we're potentially seeing from fuel retailers."

"I am asking for every lever that's available to the government to deal with the cost of living to be discussed at Cobra, hence we've got the Bank of England and others there."

- UK Prime Minister Keir Starmer, Monday March 23

After Trump's tweet, gilt yields fell back to approximately 4.9%. The relief rally in bonds mirrored equities. But it is worth noting: 4.9% is still dramatically elevated compared to pre-war levels, and still well above the 4.5% threshold that most analysts flag as a potential trigger for renewed UK fiscal instability.

The comparison to 2008 is not just numerical. In 2008, gilt yields spiked as markets priced existential risk to the financial system. In 2026, they are spiking because an energy shock is threatening the fiscal sustainability of a government already running tight finances. Different mechanism, same fear signal.

UK 10-year gilt yields climbed steadily since the war began, touching 5.12% on Monday - their highest since the 2008 financial crisis. Post-tweet rebound brought them to 4.9%. BLACKWIRE chart.

The "Bananas" Move: Bessent's Iranian Oil Sanctions Reversal

Three days before the tweet drama, the US made a move that experts described - one word at a time - as "bananas."

Treasury Secretary Scott Bessent announced what he called a "narrowly tailored, short-term authorisation" permitting the sale of Iranian oil currently stranded at sea. The waiver, valid until April 19, covers crude oil and petroleum products of Iranian origin already loaded on vessels. Bessent claimed the move would quickly bring 140 million barrels of oil to global markets.

The numbers are the problem. The world consumes roughly 100 million barrels of oil per day. Bessent's 140-million-barrel release represents approximately 1.4 days of global consumption. The Hormuz blockade has been removing an estimated 10 million barrels per day from available supply since late February. Against a cumulative 240-million-barrel deficit, Bessent's measure is a bandage on a hemorrhage.

David Tannenbaum, director of Blackstone Compliance Services - a consultancy specializing in maritime sanctions - was direct: "Essentially we're allowing Iran to sell oil, which could then be used to fund the war effort." He called the idea "bananas."

Rachel Ziemba, an adjunct senior fellow at the Center for a New American Security, told the BBC: "I don't think it's a game changer and it raises a whole lot of questions." She acknowledged that the US was "definitely in an every-barrel-counts situation because of the scale of the supply shock."

The political logic is contorted. The US is simultaneously bombing Iran's military and energy infrastructure, threatening to "obliterate" its power plants, and lifting sanctions to allow Iran to sell oil - while claiming Iran cannot access the revenue. David Malpass, former World Bank president, called it "a narrow action that should cause downward pressure on oil prices outside China."

Before the war, China was buying Iranian oil at steep discounts because sanctions blocked other buyers. Bessent's explicit goal was to divert those barrels to India, Japan, and Malaysia instead - while "forcing China to pay market price." In practice, experts say it was near-impossible to prevent Iran from accessing at least some of that revenue regardless of US blocking mechanisms.

The waiver is also a stunning policy reversal. For years, US maximum-pressure sanctions on Iranian oil were a cornerstone of Washington's Iran strategy. Lifting them - even temporarily, even selectively - for a country the US is actively at war with is not a coherent policy position. It is desperation dressed up as strategy.

The math behind Bessent's 140M barrel move: 1.4 days of global supply against months of Hormuz disruption. Experts called it "bananas." BLACKWIRE data table.

What the Market Is Actually Pricing: Stagflation Risk

Step back from the day's intraday noise and the picture is grimmer than any single trading session suggests. Markets are not just pricing a war. They are pricing the structural consequences of a sustained oil supply shock - and the word that keeps appearing in analyst notes is one that has not been relevant since the 1970s: stagflation.

Stagflation is the combination of stagnant economic growth and persistent inflation. It is the hardest macroeconomic scenario for central banks to manage, because the tools for fighting inflation (raising interest rates) directly worsen economic stagnation, and the tools for fighting stagnation (cutting rates, stimulus) directly worsen inflation.

The energy price shock from the Iran war has the exact profile needed to create stagflation in oil-importing economies. Higher energy prices are directly inflationary - they raise the cost of production, transport, heating, and food across the entire economy. At the same time, higher energy costs squeeze household purchasing power and corporate margins, which reduces growth.

Fatih Birol, head of the International Energy Agency, put it bluntly on Monday: "This crisis as things stand is now two oil crises and one gas crash put all together." His reference was to the 1973 oil embargo and the 1979 Iranian revolution supply shock - the two most severe energy crises in modern history. Adding a simultaneous gas supply disruption (from attacks on Qatar's South Pars field and Iranian gas facilities) makes the current situation potentially more severe than either historical predecessor.

Market Intelligence Strategist Ed Moya told the BBC that the risk of stagflation was real "if energy prices are not contained." The IEA has been considering releasing additional emergency reserves - a move that would provide temporary relief but would not change the structural supply picture. As one analyst noted, reserves are designed for emergencies measured in weeks, not conflicts that have already lasted 24 days with no clear resolution in sight.

The S&P 500 and Dow Jones both opened up approximately 2% on Monday after the Trump tweet - but that needs context. Both indices remain sharply lower than pre-war levels as rising energy costs eat into corporate profit forecasts. The relief rally is a function of sentiment, not fundamentals. Oil at $103 is still nearly $31 above where it was before the first strike on Iran on February 28.

Market Snapshot - Monday March 23, 2026 (Close/Late Session)

| Brent Crude | ~$103/bbl (was $113 at session peak) |

| WTI Crude | ~$99/bbl |

| S&P 500 | +2.0% (from deeply red open) |

| Dow Jones | +2.1% |

| FTSE 100 | +0.3% (reversed -2%+ earlier) |

| DAX (Germany) | +1.7% |

| CAC 40 (France) | +1.2% |

| Nikkei 225 | -3.5% (closed before tweet) |

| Kospi (Korea) | -6.5% (closed before tweet) |

| UK 10Y Gilt Yield | 4.9% (peaked 5.12%, highest since 2008) |

| Intraday oil swing | $17 in approximately 20 minutes |

The Five-Day Clock: What Happens Next

Trump's TruthSocial post put a five-day pause on strikes against Iranian power plants and energy infrastructure, "subject to the success of the ongoing meetings and discussions." The clock started Monday, March 23. That puts the deadline at Saturday, March 28.

There are multiple scenarios from here - and only one of them is genuinely good for global markets.

Scenario 1 - Talks succeed, deal reached: Iran agrees to reopen the Strait of Hormuz in exchange for some combination of US withdrawal from active strikes, sanctions relief, and security guarantees. Oil falls sharply - potentially back below $90 as stranded supply returns to market. Global equities surge. UK gilt yields normalize. Probability: Markets are pricing this at perhaps 25-30% given the momentum from Trump's post.

Scenario 2 - Talks drag, fragile pause: The five-day window extends into further negotiations. Oil stays range-bound in the $95-110 zone. The global economy continues absorbing the energy shock, with stagflation pressure building gradually. UK, Germany, and South Korea enter technical recession by Q2 2026. Probability: The most likely base case, perhaps 45%.

Scenario 3 - Talks fail, Trump restarts strikes: If Saturday arrives with no deal and Iran remains defiant, Trump resumes the threat against power plants. Oil re-spikes toward $115-120. The IEA's worst-energy-crisis-in-decades scenario becomes official. UK COBRA emergency measures escalate. Global recession risk becomes consensus. Probability: 25-30%.

Scenario 4 - Escalation spiral: Either side makes a catastrophic miscalculation - a strike on civilian infrastructure that crosses a line, or an Iranian missile that hits a critical Gulf facility like Ras Tanura. Oil trades toward $140+. G7 emergency oil summit convened. Central banks face impossible choices. Probability: Low but non-zero - perhaps 5-10%.

The immediate question is whether Iran's denial of the talks is tactical (maintaining domestic hardline credibility while back-channels operate) or literal (there are no talks and Trump invented them). Susannah Streeter's warning applies at maximum force here: "Clinging to President Trump's words is fraught with risks, given how hopes have already risen and then been dashed over the last four weeks."

This is not the first time markets have rallied on ceasefire signals during the Iran conflict. On at least two previous occasions over the past 24 days, traders bought peace premiums that subsequently proved premature. Each disappointment has left a slightly more cautious market. The $17 swing was violent - but notice that oil did not fall to $85. It settled at $103. That rebound premium represents the market's learned skepticism about this war ever resolving cleanly.

The Bitcoin Factor: Digital Oil or Digital Nothing?

The cryptocurrency market's behavior during the Iran conflict has been one of the most watched narratives of the past month. Bitcoin was initially sold off hard alongside risk assets when the war began on February 28 - the "crypto is risk-on" playbook. But as the conflict has extended, BTC has gradually detached from that correlation and begun trading more like the digital safe-haven narrative its advocates have always claimed.

Bitcoin's intraday action on Monday reflected the same pattern as equities - selling off in morning Asian hours, then recovering partially after Trump's post. But the magnitude was notably muted compared to the equity swing. Where the Kospi fell 6.5% and the FTSE fell 2% before recovery, Bitcoin's volatility was compressed. Analysts at Unchained Crypto have noted that "Bitcoin finally acted like a hedge" in recent sessions - though they acknowledged the open question was whether this behavioral shift would prove durable.

The deeper crypto-market story is what the war has done to DeFi and on-chain activity. With traditional financial markets experiencing extreme volatility, on-chain perpetuals platforms - particularly Hyperliquid - have seen explosive volume in oil-related derivative proxies. Traders who cannot easily access WTI or Brent futures directly are routing through crypto-native instruments to express their macro views.

MicroStrategy's Michael Saylor has continued purchasing Bitcoin throughout the conflict, framing BTC as the only asset that exists entirely outside the physical infrastructure that wars can destroy. His thesis - that no military can bomb a blockchain - has found new resonance in an environment where physical oil infrastructure across the Gulf is being systematically targeted. Whether or not the long-term investment thesis holds, the short-term narrative has given institutional Bitcoin buyers a compelling story to tell their allocators.

The Stablecoin angle matters too. USDC and USDT demand in Gulf-adjacent markets has spiked as local residents and businesses seek dollar-denominated assets that don't require a functioning bank branch or an open shipping route. Circle - which processes USDC - has seen elevated on-chain transaction volumes in the UAE and Bahrain throughout the conflict. When physical infrastructure fails, digital dollar infrastructure becomes a genuine utility, not just a trading instrument.

Who Is Winning and Who Is Paying

In any market dislocation this severe, the question of winners and losers matters as much as the aggregate price moves.

Winners: US domestic oil producers are the most obvious beneficiaries. WTI at $99 is a windfall for shale operators who were breakeven at $45. Norwegian energy companies are experiencing record revenues as European buyers scramble for non-Gulf supply. Saudi Aramco - despite operating in a geopolitically precarious region - is benefiting from elevated prices on its non-Hormuz pipeline capacity. Russia, despite its own sanctions complications, is finding buyers for Urals crude at premiums that would have been unimaginable six months ago. And anyone who was long energy ETFs, long oil futures, or short airline and shipping stocks entering the conflict has made spectacular returns.

Losers: South Korea, Japan, and India are absorbing massive import cost increases with no domestic production to offset them. The Korean economy's 6.5% single-day equity drop is the market communicating that pain directly. European manufacturers facing both higher energy input costs and weaker consumer demand are being squeezed from both ends. UK households with mortgage resets coming in 2026 face the double pressure of elevated gilt yields (meaning higher fixed-rate mortgage costs) and higher energy bills. And the global airline industry - which was just recovering from post-COVID overcapacity - is facing jet fuel prices that make most routes unprofitable at current ticket prices.

The most exposed single asset: UK gilts. The combination of a cost-of-living crisis, a weakened fiscal position, and the Bank of England's inability to simply cut rates to stimulate growth (because inflation from energy costs would immediately worsen) puts UK sovereign debt in a uniquely uncomfortable position. The 5.12% yield seen on Monday morning was a warning shot. If the conflict extends and oil stays above $100, a UK gilt crisis - in the tradition of the 2022 Liz Truss LDI blowup - becomes a non-trivial risk.

Keir Starmer is sitting on an energy price crisis with fewer tools than he would like. The previous government's North Sea drilling restrictions are now being attacked from all sides of the political spectrum. Conservative leader Kemi Badenoch called for the COBRA meeting to "adopt our cheap power plan" and drill the North Sea. Green Party leader Zack Polanski called for windfall taxes and accelerated renewables. Neither solution is operative on a five-day timeline. There is no quick fix when 20% of the world's oil supply is stuck behind a military blockade.

The Winners and Losers Scoreboard

| US Shale Producers | Windfall - WTI at $99 |

| Norway Energy Sector | Record revenues |

| Russia (Urals crude) | Premium pricing on diverted barrels |

| Oil-long investors | +$30/bbl vs pre-war |

| South Korea economy | Kospi -6.5% Monday alone |

| Japan (net oil importer) | Nikkei -3.5%, rising import costs |

| UK households | Energy bills + mortgage rates rising |

| Global airlines | Jet fuel destroying route economics |

| European manufacturers | Energy + demand double squeeze |

| UK government (gilts) | Borrowing costs at 2008 crisis levels |

The IEA Warning and What "Worst Crisis in Decades" Actually Means

Fatih Birol did not use the phrase "worst energy crisis in decades" casually. The IEA head has a precise understanding of what that framing implies - and what it implies is serious.

The 1973 oil embargo, triggered by the Arab oil-producing states' response to US support for Israel in the Yom Kippur War, cut global oil supply by roughly 7% and caused a quadrupling of oil prices within months. It tipped the US and Europe into deep recession and permanently restructured global energy markets - driving the creation of the IEA itself, the strategic petroleum reserve system, and decades of energy diversification policy.

The 1979 Iranian Revolution oil shock cut supply by roughly 4% of global consumption and sent prices from $13 to $34 per barrel in less than a year. Combined with the 1980-88 Iran-Iraq War, it produced a decade of elevated oil prices and recession in oil-importing economies.

Birol's comparison - "two oil crises and one gas crash put together" - suggests the current disruption is quantitatively larger than either historical precedent. The Hormuz blockade is removing an estimated 10% of global daily oil supply, not 4-7%. The simultaneous damage to South Pars and other Iranian gas facilities has compressed global LNG supply at a moment when European gas storage was already below comfortable levels going into summer.

The historical record is unambiguous: sustained oil supply shocks of this magnitude cause recessions. The only variable is how deep and how long. Countries with strong domestic energy production (the US), diversified supply chains (Norway, Saudi Arabia via non-Hormuz routes), or high renewable penetration (Denmark, some German states) are more insulated. Countries dependent on Hormuz-routed hydrocarbons - South Korea, Japan, India, much of southern Europe - are not.

The five-day clock that Trump started Monday is not just a diplomatic deadline. It is a macroeconomic countdown. Every day the Hormuz blockade holds, the cumulative damage to global growth deepens. Supply shortfalls compound. Inventory drawdowns accelerate. Strategic petroleum reserves - being released in unprecedented quantities by the US, Japan, South Korea, and IEA member states - have finite capacity. They can cover weeks. They cannot cover months.

At 4:30 PM CET on Monday, March 23, the war is 24 days old. The Hormuz blockade is 23 days old. The question that every oil trader, every central banker, and every finance minister on Earth is asking tonight is whether the five-day pause is the beginning of an end - or the next chapter in a conflict that has already rewritten the economic assumptions of 2026.

The answer will arrive by Saturday.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on TelegramSources: BBC Business (Nick Edser, Peter Hoskins, Fiona Nimoni reporting); Donald Trump TruthSocial post March 23 2026; Iran Foreign Ministry statement March 23 2026; Susannah Streeter / Wealth Club; David Tannenbaum / Blackstone Compliance Services; Rachel Ziemba / Center for a New American Security; Fatih Birol / IEA speech Australia March 23 2026; David Malpass / X post; Matthew Pennycook / BBC interview; Keir Starmer COBRA press remarks. Market data via BBC Markets and trading sources.