$122 Billion and a Body Count: OpenAI Kills Sora, Dumps Disney, and Bets Everything on a Superapp

The largest private funding round in history just closed. The price of admission was a dead video product, a blindsided media giant, and a bet-the-company pivot toward a unified AI operating system. This is the story of what OpenAI destroyed to survive.

The most expensive bet in the history of private technology just closed. Photo: Unsplash

One hundred and twenty-two billion dollars. That is not a typo. That is not a government stimulus. That is the amount of private capital that just flowed into a single company that has never turned a profit - a company that, in the same breath, killed its flagship creative product, torched a billion-dollar partnership with the Walt Disney Company, and announced plans to merge everything it makes into a single desktop application it calls a "superapp."

The funding round closed on March 31, 2026, with participation from Amazon, NVIDIA, SoftBank, Microsoft, and a constellation of institutional investors that reads like a who's-who of global capital markets. It values OpenAI at $852 billion post-money - more than the GDP of Switzerland, more than the market cap of most Fortune 100 companies, and roughly eight times what the company was worth eighteen months ago.

But the headline number obscures the real story. To get here, OpenAI had to execute one of the most dramatic strategic pivots in the history of technology. In the span of a single week in late March, the company killed Sora, its video generation platform; wound down a $1 billion licensing deal with Disney that was barely three months old; reshuffled its executive leadership; declared war on its own product sprawl; and announced plans for an "agent-first" superapp that would absorb ChatGPT, Codex, and a new AI browser called Atlas into one unified interface.

The message from San Francisco was clear: the era of experimentation is over. The era of extraction has begun.

01 // The Money: Anatomy of a $122 Billion Round

The round drew every major player in global finance. Photo: Unsplash

The final close of OpenAI's latest funding round represents not just the largest private capital raise in history, but a structural shift in how capital markets relate to artificial intelligence. The round began in February 2026 with $110 billion and grew by an additional $10 billion in late March after CFO Sarah Friar told CNBC that investor demand remained overwhelming even as the company was busy killing products and reshuffling executives.

The anchor investors tell their own story. Amazon - which is simultaneously building its own AI infrastructure through Bedrock and Trainium chips - committed significant capital. NVIDIA, whose GPUs form the backbone of every serious AI training cluster on earth, deepened what is already the most strategically important vendor relationship in the industry. SoftBank, whose Vision Fund strategy has ping-ponged between genius and catastrophe for years, co-led the round alongside Andreessen Horowitz (a16z), D.E. Shaw Ventures, MGX, TPG, and accounts advised by T. Rowe Price Associates.

Microsoft, the company's oldest and most entangled partner, participated again - though its position is increasingly complicated. Microsoft invested $10 billion in OpenAI in January 2023, securing a 49% economic interest and exclusive cloud hosting rights. Three years later, it is investing more money into a company that is actively diversifying away from Azure exclusivity toward Oracle, AWS, Google Cloud, and CoreWeave.

For the first time, OpenAI extended participation to individual investors through bank channels, raising over $3 billion from non-institutional participants. The company also announced inclusion in several exchange-traded funds managed by ARK Invest, a move that effectively gives retail investors indirect exposure to a private company - an unusual step that signals IPO preparation more than anything Sam Altman has actually said about going public.

The credit facility expansion is equally telling. OpenAI's revolving credit line now stands at approximately $4.7 billion, supported by a global syndicate that includes JPMorgan Chase, Citi, Goldman Sachs, Morgan Stanley, Wells Fargo, Mizuho, Royal Bank of Canada, SMBC, UBS, HSBC, and Santander. The facility remains undrawn, which means OpenAI has $4.7 billion in immediately accessible liquidity on top of the $122 billion raise. For a company that has never been profitable, the amount of financial firepower on the table is staggering.

The $852 billion valuation deserves scrutiny. In February 2025, OpenAI raised $6.6 billion at a $157 billion valuation. In twelve months, the valuation has increased by more than five times. By comparison, it took Apple roughly fifteen years to go from $157 billion to $852 billion. OpenAI did it in a year, without generating a single quarter of profit.

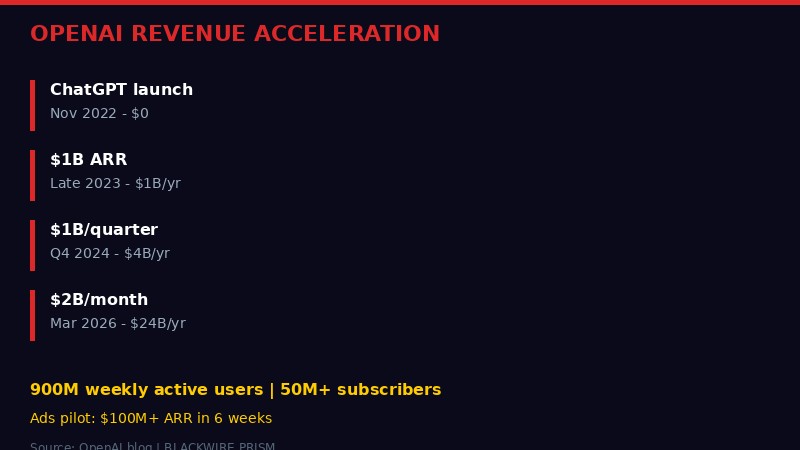

The valuation math works only if you believe OpenAI's revenue trajectory is not just real but accelerating. And to be fair, the numbers are remarkable. According to OpenAI's own announcement, the company is now generating $2 billion in revenue per month - a $24 billion annual run rate. That is up from $1 billion per quarter at the end of 2024 and $1 billion per year in late 2023. The company claims it is growing revenue "four times faster than the companies who defined the Internet and mobile eras, including Alphabet and Meta."

Those numbers, if accurate, put OpenAI's revenue growth on a trajectory unlike anything in the history of enterprise technology. But revenue is not profit. And at the burn rates required to train and serve frontier models - the company's compute infrastructure spans NVIDIA, AMD, AWS Trainium, Cerebras, and a custom chip partnership with Broadcom - the gap between top-line revenue and bottom-line profitability remains a yawning chasm that nobody in the investment memo is eager to discuss in detail.

02 // The Kill Shot: Sora's Rise and Collapse

Sora went from breakthrough demo to discontinued product in eighteen months. Photo: Unsplash

On March 24, 2026 - a Tuesday - OpenAI announced it was killing Sora, its AI video generation platform. The timing was deliberately efficient. In a single day, the company disclosed the Sora shutdown, confirmed the unwinding of the Disney licensing deal, announced the additional $10 billion in funding, and reshuffled Fidji Simo's title from "CEO of Applications" to "CEO of AGI Deployment."

The day before, OpenAI had published a blog post about Sora's safety standards, describing ongoing improvements to its guardrails. Reuters reported that employees were blindsided by the announcement, which came less than an hour after teams were actively working on a Sora-related project with Disney.

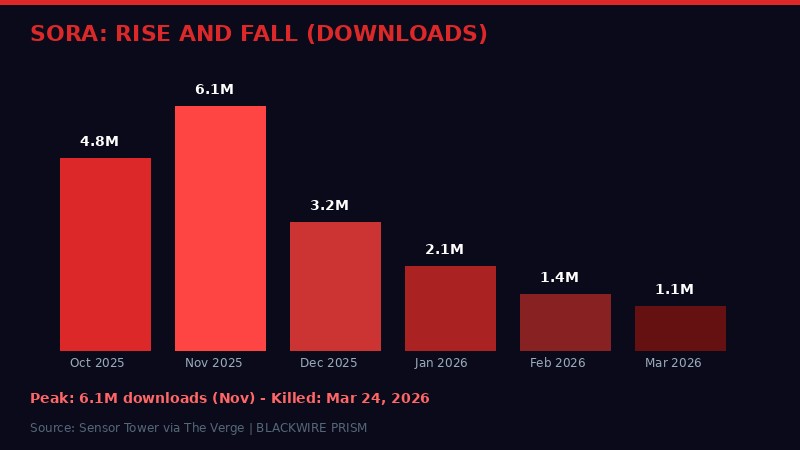

The numbers tell the story of a product that burned hot and collapsed fast. According to Sensor Tower data reported by The Verge, Sora launched with approximately 4.8 million worldwide downloads in October 2025, peaked at 6.1 million in November, and then fell off a cliff: 3.2 million in December, 2.1 million in January, 1.4 million in February, and just 1.1 million month-to-date when the plug was pulled in March.

"What's most notable about it is dropping off while they're expanding into new markets - that should be driving growth," Seema Shah, VP of insights at Sensor Tower, told The Verge. "You should've seen an uptick in that. Even if nobody else in the US downloaded it again, there should be some growth, presumably."

The competitive landscape had shifted beneath Sora's feet. Google's video generation capabilities, along with Kling, Runway, Luma, Moonvalley, and Seedance, had collectively eroded whatever first-mover advantage Sora might have had. Trevor Harries-Jones, a board member at the Render Network Foundation, told The Verge that "the state of innovation and the plethora of choice means there's just little to no moat and it's very simple to switch between" video generation tools.

"For us, there wasn't anything that they were winning, in terms of one of the use cases. It had fallen off from really a very strong start, to be eclipsed by some of the other competitive players in the space." - Trevor Harries-Jones, Render Network Foundation, to The Verge

But the real issue was compute. At OpenAI's DevDay event in October 2025, executives repeatedly expressed anxiety about computational constraints. "Obviously someday, we have to be very profitable," Altman said at the time. Company president Greg Brockman put it bluntly: "Asking, 'How much compute do you want?' is a little bit like asking, 'How much of the workforce do you want?' The answer is you can always get more out of more."

Sora was a compute hog in a company that was running out of compute for everything else. Reuters reported that running Sora required so much computational power that it left other teams working with less. When you are spending billions of dollars on GPUs to train the next generation of language models, and a video generation app that peaked at six million downloads is burning through your precious inference capacity, the math becomes obvious even if the optics do not.

The gap between Sora's buzzy launch demos and its actual product reality never closed. Harries-Jones noted that the marketing videos seemed "groundbreaking" but that there was a "gap" between the demo and the real launch, particularly around cost, generation timeframes, and quality consistency. It is a familiar pattern in AI: stunning controlled demonstrations that create expectations the shipping product cannot match.

03 // The Disney Wreckage: $1 Billion That Never Changed Hands

The Disney-OpenAI partnership lasted barely 90 days. No money ever changed hands. Photo: Unsplash

In December 2025, Disney announced a $1 billion equity investment in OpenAI with option rights for additional equity. The deal was comprehensive: Disney would become a "major customer" of OpenAI, integrating the company's tools across Disney+ and other properties. Sora would gain access to hundreds of Disney, Pixar, Star Wars, and Marvel characters, with a selection of AI-generated content slated to stream on Disney+ itself. ChatGPT would be made available to Disney employees.

Less than ninety days later, none of it exists.

Reuters reported that no money ever changed hands between OpenAI and Disney. The licensing agreement - described as a three-year deal - was terminated roughly three months in. According to The Hollywood Reporter, Disney was blindsided by the announcement, learning about the Sora shutdown on the same day as everyone else despite being one of the platform's marquee partners.

The incident reveals something important about how OpenAI operates under pressure. This is a company that, when it decides to pivot, does not telegraph or negotiate with partners. It moves fast and deals with the fallout later. The Disney relationship was not a minor collaboration - it was a billion-dollar strategic partnership with one of the most powerful media companies on earth, announced with considerable fanfare just weeks earlier. To unwind it on a Tuesday afternoon alongside a press release about more funding suggests either remarkable decisiveness or remarkable dysfunction, depending on your perspective.

Dave Davis, chief content officer at Protege - a company that licenses content to AI firms for model training - told The Verge that Disney remained "wide open for business" for character licensing with other video generation companies. Google, Runway, Luma, Moonvalley, Kling, and Seedance were all potential replacement partners. The message from Disney's side was clear: AI-generated entertainment is still on the table, just not with OpenAI.

For OpenAI, the Disney collapse carries reputational risk that extends beyond the immediate financial non-event. Enterprise customers making multi-year commitments to OpenAI's platform now have a fresh example of what happens when the company decides a product line is not strategically aligned. If Sora can be killed three months into a billion-dollar deal, what happens to the enterprise API integrations that 40% of OpenAI's revenue now depends on? The answer - "those are different, those are core to our strategy" - is the kind of reassurance that sounds compelling until it doesn't.

04 // The Superapp Gambit: One App to Rule Them All

OpenAI's answer to product sprawl: absorb everything into one unified interface. Photo: Unsplash

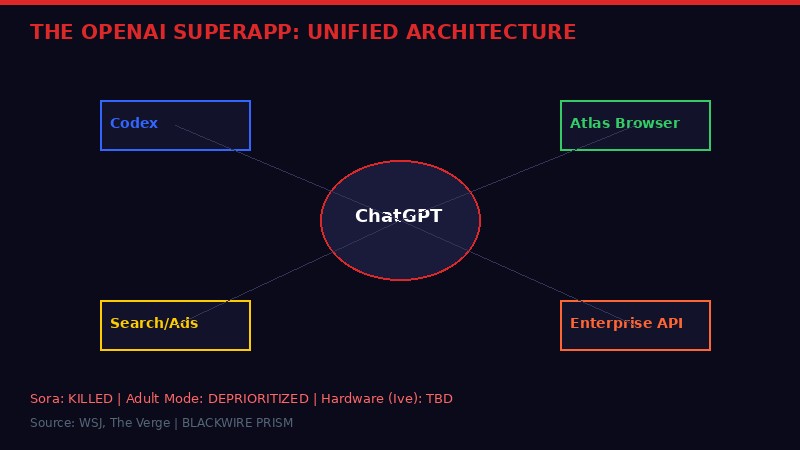

The strategic replacement for Sora, adult mode, and the rest of OpenAI's "side quests" is what the company now calls a "unified AI superapp." According to The Wall Street Journal, the desktop application will merge ChatGPT, the Codex AI coding agent, and a new AI-powered browser called Atlas into a single interface. The mobile version of ChatGPT is reportedly unaffected.

The internal logic is straightforward. Fidji Simo, in a memo cited by the WSJ, wrote that fragmentation across multiple products and interfaces "has been slowing us down and making it harder to hit the quality bar we want." In a follow-up post on X, she added: "Companies go through phases of exploration and phases of refocus; both are critical. But when new bets start to work, like we're seeing now with Codex, it's very important to double down on them and avoid distractions."

The superapp concept is not new in technology. WeChat in China, Grab in Southeast Asia, and Paytm in India all built massive businesses by consolidating multiple services into a single interface. What is new is the ambition to do this with artificial intelligence as the substrate rather than payments or messaging. OpenAI's bet is that "agent-first" computing - where an AI system understands intent, takes action across applications and data, and operates autonomously on behalf of users - is the next platform shift after mobile.

In their funding announcement, OpenAI laid out the thesis explicitly: "As models become more capable, the limiting factor shifts from intelligence to usability. Users do not want disconnected tools. They want a single system that can understand intent, take action, and operate across applications, data, and workflows."

The timing coincides with Codex's breakout moment. OpenAI says Codex now serves over 2 million weekly users, up 5x in the past three months, with usage growing more than 70% month over month. This surge directly mirrors the competitive threat from Anthropic's Claude Code, which has been experiencing its own extraordinary growth period. Claude Code passed $1 billion in revenue in November 2025 and, according to Anthropic, writes between 70% to 90% of code across the company's own engineering teams.

"We cannot miss this moment because we are distracted by side quests. We really have to nail productivity in general and particularly productivity on the business front." - Fidji Simo, OpenAI CEO of AGI Deployment, internal memo reported by WSJ

The superapp strategy also serves a distribution function. OpenAI's funding announcement described a "reinforcing flywheel" where consumer adoption creates a distribution channel for enterprise products, developer usage expands the platform, and compute investment improves everything simultaneously. By consolidating surfaces, the company can "translate advances in model capability directly into user adoption and engagement" without requiring users to discover and adopt separate applications.

There is a darker reading of the superapp pivot, however. Consolidating everything into one interface is also a way to make it harder for users to leave. If your coding agent, browser, search engine, and chat assistant all live in the same application, switching costs increase dramatically. It is the same lock-in strategy that Microsoft perfected with Office and that Apple perfected with iOS - bundling as a competitive moat. The question is whether users will accept an AI company as the unified interface layer for their digital lives the way they accepted operating system vendors in previous computing eras.

05 // The Anthropic Problem: Why OpenAI Is Running Scared

The real threat is not from startups - it is from the former employees who built the original models. Photo: Unsplash

You cannot understand OpenAI's March 2026 pivot without understanding what happened at Anthropic between November 2025 and February 2026. That three-month period transformed the competitive landscape of the AI industry more dramatically than anything since ChatGPT's original launch.

It started with Claude Code. Anthropic's coding platform, first released in February 2025, experienced an extraordinary surge in adoption over the 2025 holiday season. Engineers and developers who had extra time during the break discovered that Claude - particularly the Opus 4.5 model released just before Thanksgiving - could complete complex software engineering tasks with a level of competence that felt qualitatively different from previous AI coding tools.

The results were viral. People built MRI result viewers, Goodreads alternatives, and complex judged T-shirt design contests - all using Claude Code. X posts in January proclaimed "we are witnessing an irreversible trend" of Anthropic "taking the lead" from OpenAI. Between December 29 and January 26, Anthropic's word-of-mouth exposure spiked by 13 points on Caliber's 100-point system while OpenAI's slightly declined.

Boris Cherny, the creator and head of Claude Code, became something of a celebrity in engineering circles. He shipped more than 300 pull requests in December alone, using Claude Code to build Claude Code. Across Anthropic's engineering organization, Claude Code writes between 70% and 90% of all code, according to the company. Cherny himself now uses it for 100% of his programming work.

The financial impact was immediate. Anthropic is reportedly in talks to double its latest funding round to $20 billion at a $350 billion valuation - still less than half of OpenAI's but accelerating. Claude Code passed $1 billion in revenue. Anthropic won more categories than any competitor in Scale AI's "Model of the Year" awards, including "best agentic model."

"I think we'll remember December 2025 as this inflection point where all of a sudden everything changed," Mike Brevoort, principal architect at warehouse automation startup Mytra, told The Verge. He described testing Claude Code over the holidays and having a "water in the face" moment: "Wait a minute, that's possible?"

Maggie Basta, a partner at Scale Venture Partners, put it more directly: "The move from different agentic coding interfaces to Claude Code has been pretty astonishing."

This is the context in which Altman's "code red" declaration, Simo's anti-side-quest memo, the Sora kill, and the superapp pivot all make sense. OpenAI is not making these moves from a position of comfort. It is making them because the company that was founded by people who left OpenAI - Anthropic's founders Dario and Daniela Amodei were OpenAI's VP of Research and VP of Operations respectively - is eating its lunch on the product that matters most for enterprise revenue: AI-assisted coding.

Anthropic recently released Opus 4.6, which it describes as a "direct upgrade" with improved speed and precision for agentic work. The race is not slowing down. It is accelerating. And for OpenAI, that acceleration explains why killing Sora to free up compute for language model training and coding agent development was not just strategically logical but existentially necessary.

06 // The Compute Arms Race: Infrastructure as Destiny

In the AI era, compute capacity is the strategic advantage that determines everything else. Photo: Unsplash

OpenAI's funding announcement devoted more words to compute infrastructure than to any product or feature. That was not accidental. The company's thesis - articulated with unusual clarity - is that computational capacity is the single variable that determines everything: research capability, product quality, revenue growth, and competitive position.

"Durable access to compute is the strategic advantage that compounds across the entire system," the announcement stated. "It advances research, improves products, expands access, and structurally lowers the cost of delivery at scale."

The infrastructure strategy is now explicitly multi-vendor, a significant departure from the Microsoft-centric approach of the past three years. OpenAI's compute stack spans cloud partnerships with Microsoft Azure, Oracle, AWS, CoreWeave, and Google Cloud. Silicon comes from NVIDIA (still the foundation), AMD, AWS Trainium, Cerebras, and a custom chip being co-designed with Broadcom. Data center partnerships extend through Oracle, SBE, and SoftBank.

This diversification is strategically sound but relationally complicated. Microsoft invested $10 billion for exclusive cloud hosting rights. Now it is watching its investment target build on AWS, Oracle, and Google Cloud. NVIDIA is both an investor and the dominant hardware supplier, but OpenAI is simultaneously working with AMD, Cerebras, and developing its own chip. Every major relationship in OpenAI's infrastructure stack involves at least two simultaneous dynamics: investment partnership and competitive threat.

The flywheel description in the announcement reads like a textbook on platform economics: "More compute drives more intelligent models. More intelligent models drive better products. Better products drive faster adoption, more revenue and more cashflow. That gives us the ability to reinvest and deliver intelligence more efficiently to consumers, enterprises, and builders around the world." Each new generation of infrastructure trains more capable models while algorithmic and hardware improvements reduce the cost per token, lowering the cost per unit of intelligence.

The APIs now process more than 15 billion tokens per minute. That number, more than any funding total or valuation multiple, captures the raw scale of what OpenAI has built. Fifteen billion tokens per minute means the AI is processing roughly the equivalent of 11 million standard-length books every sixty seconds. The inference compute required to sustain that throughput is extraordinary - and growing.

The compute arms race has a geopolitical dimension as well. OpenAI's announcement framed the moment in historical terms: "In past generations, capital markets helped build the systems that defined modern economies, from electricity to highways to the internet. This is that kind of moment again." Whether $122 billion in private capital flowing into a single American AI company represents wise infrastructure investment or speculative excess depends entirely on whether the intelligence flywheel actually works as described - or whether it turns out to be a very expensive treadmill.

07 // The 900 Million Question: Scale Without Profit

The numbers are enormous. The question is whether they add up. Photo: Unsplash

ChatGPT now has more than 900 million weekly active users and over 50 million subscribers. It has 6x the monthly web visits and mobile sessions of the next largest AI application. Total AI time spent is 4x the next largest AI app and 4x all others combined. Search usage has nearly tripled in a year. The ads pilot reached more than $100 million in annual recurring revenue in under six weeks.

Enterprise revenue now makes up more than 40% of the total and is on track to reach parity with consumer revenue by the end of 2026. The company has increased eightfold its number of business customers representing more than $1 million in revenue run rate. GPT-5.4, described as the "most capable model yet," is driving record engagement across agentic workflows.

These are genuinely impressive metrics. But they exist in tension with a fundamental reality: OpenAI has never reported a profit. The $24 billion annual revenue run rate sounds transformative until you consider that training a frontier model can cost upward of $500 million, that serving 900 million weekly users at scale requires enormous inference infrastructure, and that the company is simultaneously building custom chips, operating multiple cloud partnerships, and funding a research organization that employs some of the most expensive talent on the planet.

The comparison to previous technology platforms - Alphabet and Meta - is instructive but potentially misleading. Google and Meta both achieved profitability relatively early in their growth curves because advertising is fundamentally a high-margin business. Once the user base existed, converting attention into revenue was straightforward and cheap. AI inference is not cheap. Every query costs real money in GPU time. Every token processed is a unit of compute burned. The marginal cost of serving an additional user on an AI platform is meaningfully higher than the marginal cost of serving an additional user on a search engine or social network.

This is the central question that $122 billion of investor capital is betting on: can OpenAI drive the cost of intelligence low enough, fast enough, that the margins eventually look like a software company rather than a compute utility? The "compounding effect" described in the announcement - where better infrastructure and models lower delivery costs while improved products increase revenue per unit of compute - is theoretically elegant. Whether it materializes in practice, at the scale required to justify an $852 billion valuation, remains an open question that no amount of funding can answer by itself.

08 // What Comes Next: The Road to IPO

The superapp, the IPO, the pivot to profit - it all has to work simultaneously. Photo: Unsplash

The inclusion in ARK Invest ETFs, the $3 billion from individual investors, the revolving credit facility, the multi-bank syndicate - every financial move OpenAI made in March 2026 points toward an initial public offering. The question is not whether it will happen but when, and at what price.

The company's transition from nonprofit research lab to for-profit corporation is now effectively complete, though the legal mechanics continue to generate controversy. The original nonprofit entity that controlled OpenAI has been progressively sidelined, and the for-profit subsidiary - in which investors hold economic interests - is the entity raising money and making strategic decisions. Altman reportedly said the security and safety teams no longer report directly to him, a structural change that could signal either improved governance or decreased safety priority depending on your level of cynicism.

For the IPO to work at anything close to the current private valuation, several things have to happen simultaneously. The superapp has to ship and gain adoption. Codex has to maintain its growth trajectory against Anthropic's Claude Code. Enterprise revenue has to keep compounding at 40%+ of total and trending toward 50%. The compute infrastructure has to deliver the cost improvements that make the flywheel spin. And the company has to demonstrate a credible path to profitability - not actual profit, necessarily, but a trajectory that public market investors can model and believe in.

The risks are non-trivial. Anthropic is gaining ground. Google has virtually unlimited compute and distribution. Meta is open-sourcing competitive models that compress margins across the industry. Regulatory scrutiny is intensifying globally. The "adult mode" exploration, reportedly deprioritized alongside Sora, suggests internal disagreements about product direction that consolidation does not necessarily resolve.

The Sora kill and Disney fallout also create a precedent problem. Public companies are held to higher standards of partner reliability and product commitment than private ones. If OpenAI can kill a billion-dollar partnership with three months' notice while private, what happens when it is answering to quarterly earnings calls and shareholder lawsuits?

There is also the Sam Altman factor. The CEO who was fired and reinstated in November 2023, who has been progressively converting a nonprofit AI safety lab into the most valuable private technology company on earth, who is simultaneously investing in nuclear energy, longevity research, and cryptocurrency - Altman is the kind of founder who inspires either fervent loyalty or deep suspicion, and rarely anything in between. An IPO would expose him to a level of ongoing public scrutiny that the private fundraising circuit has largely shielded him from.

09 // The Second-Order Effects Nobody Is Discussing

The most consequential implications of OpenAI's March 2026 moves are the ones that received the least coverage.

The AI video market just got more competitive, not less. With Sora gone, Disney and other major content companies are actively shopping for replacement partners. Google, Runway, Luma, Moonvalley, Kling, and Seedance all have open lanes. The paradox: OpenAI killing Sora might accelerate AI video generation adoption industry-wide by forcing content companies to diversify their AI partnerships rather than consolidating with a single provider.

The superapp creates a new attack surface for regulation. If ChatGPT, Codex, search, browsing, and agentic AI all live in one application, regulators in the EU, UK, and US now have a single target to point antitrust and AI governance frameworks at. The bundling strategy that drives lock-in also drives regulatory attention. Microsoft learned this with Internet Explorer. Google learned it with Search and Android. OpenAI may be about to learn it with an AI superapp.

The developer ecosystem faces consolidation pressure. Independent AI tools, coding assistants, browser extensions, and productivity apps that currently coexist with ChatGPT face extinction if the superapp successfully absorbs their functionality. The same developer ecosystem that OpenAI depends on for API revenue could find itself competing with OpenAI's own unified product. This is the platform paradox that Google, Apple, and Amazon have all navigated - and none of them navigated it cleanly.

The compute diversification strategy weakens Microsoft's leverage. Microsoft's $10 billion investment bought exclusive cloud hosting rights. The diversification to Oracle, AWS, Google Cloud, and CoreWeave dilutes that exclusivity. Microsoft can either accept the dilution and maintain its financial relationship, or push back and risk alienating its most strategically important AI partner. Neither option is comfortable.

The precedent for AI company governance is being set in real time. OpenAI's transition from nonprofit to for-profit, its progressive sidelining of safety teams, its willingness to kill products and partners with minimal notice, and its accumulation of unprecedented private capital are all establishing precedents that the next generation of AI companies will either follow or explicitly reject. The norms being set now will shape how AI companies operate for the next decade.

10 // The Verdict: Is This the Peak or the Beginning?

One hundred and twenty-two billion dollars is a number so large that it distorts perspective. It is more money than most countries raise in a year of sovereign bond issuance. It is more than the total venture capital invested in the entire United States in 2022. It is, by any historical standard, a breathtaking concentration of private capital in a single entity that has existed for barely a decade and has never reported a quarterly profit.

The optimistic case is that OpenAI is building the infrastructure layer for intelligence itself - the electricity grid of the cognitive era - and that the revenue trajectory, the scale of adoption, and the compounding effects of the compute flywheel will eventually generate returns that make $122 billion look like a bargain. The 900 million weekly users, the $2 billion monthly revenue, the 15 billion tokens per minute - these are not fake metrics. They represent real usage by real people doing real work.

The skeptical case is that we have seen this movie before. That "growing four times faster than Alphabet and Meta" is a meaningless comparison when those companies were profitable during their growth phases and OpenAI is not. That the compute flywheel looks elegant on a slide but depends on cost curves that are not guaranteed to materialize. That killing Sora and Disney in a single afternoon is not bold leadership but organizational chaos dressed up as strategic clarity. That $852 billion is not a valuation but a wish.

The truth is probably somewhere in the middle, and it depends on time horizons. In the short term, OpenAI has more capital, more users, and more momentum than any AI company has ever had. In the medium term, the superapp either works or it does not, Codex either outcompetes Claude Code or it does not, and the path to profitability either materializes or it does not. In the long term, the question is whether general artificial intelligence - the thing OpenAI was originally created to build safely - turns out to be possible, beneficial, and monetizable all at once.

What is certain is that March 2026 will be remembered as the month OpenAI stopped trying to be everything and started trying to be one thing extremely well. Whether that one thing is the future of computing or the most expensive bet in the history of technology remains, as of this writing, genuinely unclear.

The money is in. The bodies are buried. The app is coming. Everything else is execution.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram