OpenAI Wants to Own Its Power Supply: The Helion Fusion Deal and What It Means for Everyone Else

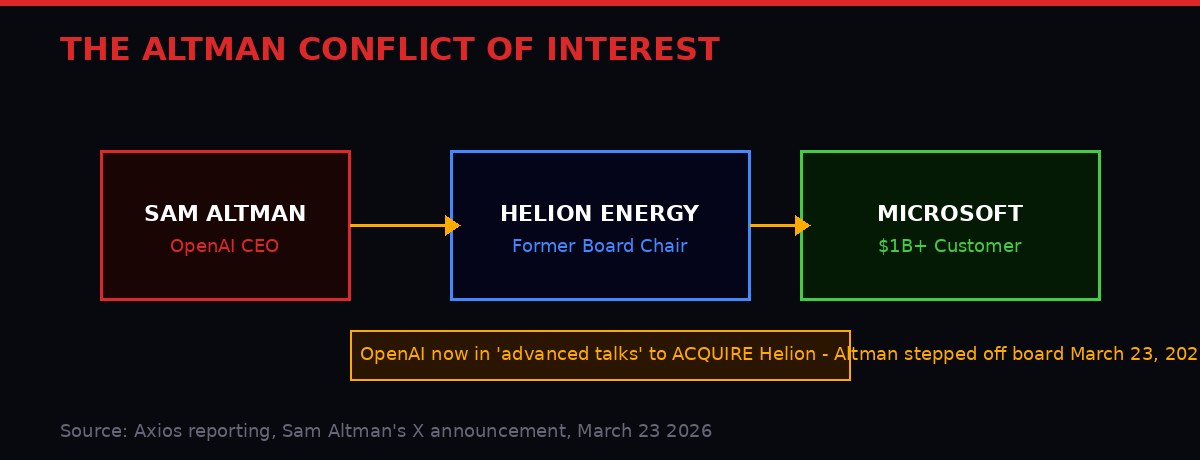

On March 23, 2026, Sam Altman posted on X that he was stepping down from the board of Helion Energy, the nuclear fusion startup he has been the most prominent public champion of for nearly a decade. The announcement was framed as a routine governance move - a chairman recusing himself from a business relationship.

It was not routine. Within hours, Axios reported that OpenAI - the company Altman leads as CEO - was in "advanced talks" to acquire Helion outright. (Source: Axios, March 23 2026)

Read those two facts together and the picture becomes clear: Altman stepped off the Helion board because his company is about to own it. The chess move was made. The announcement was the hand-waving that followed.

This is not just a big acquisition story. If it closes, OpenAI will control its own nuclear fusion energy source - a technology that, even in prototype form, produces clean electricity at a theoretical efficiency that makes every other power generation method look like burning wet wood. It is the single most significant vertical integration play in tech history, and it is happening while the rest of the industry argues about GPU allocations and electricity grid contracts.

The AI Energy Problem Nobody Wants to Quantify Out Loud

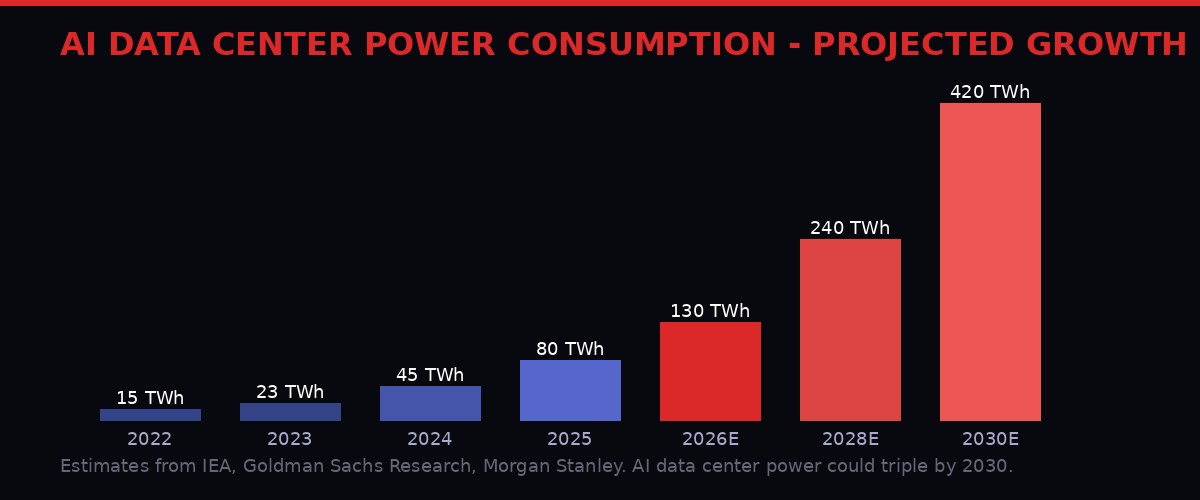

The AI industry has a power problem it has been managing through optimism for years. The basic math is brutal: training a frontier AI model now consumes more electricity than some small nations use in a year. Running inference - the process of actually answering questions, generating images, writing code - at scale is even more expensive in aggregate because it never stops.

Goldman Sachs estimated in late 2024 that AI data centers would need to triple their power capacity by 2030. Morgan Stanley put the number higher. The International Energy Agency, in its 2025 World Energy Outlook, named AI as the single largest new driver of global electricity demand growth - larger than electric vehicles, larger than industrial electrification, larger than any single sector transition in modern history. (Source: IEA World Energy Outlook 2025)

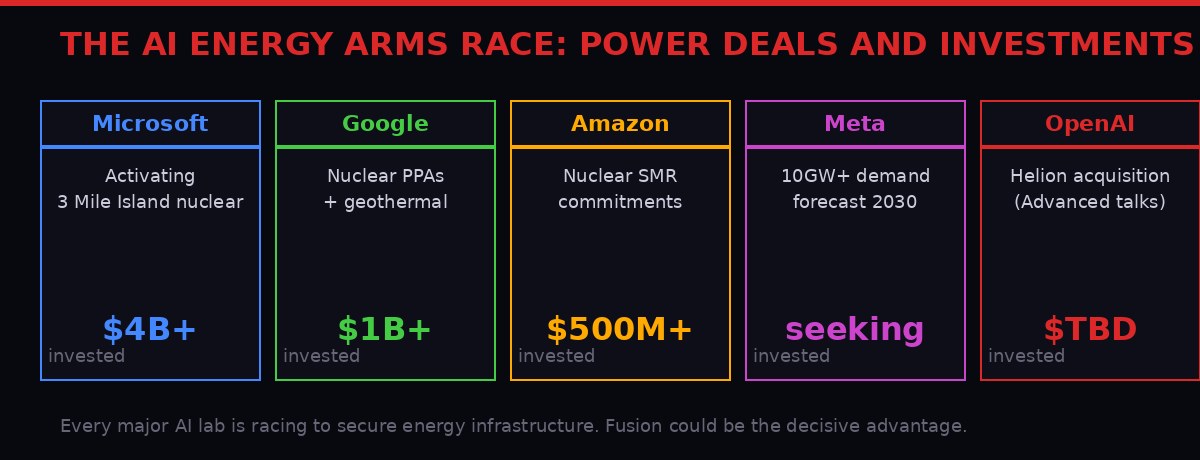

The responses from big tech have been predictable and, in the medium term, inadequate. Microsoft reactivated Three Mile Island - America's most infamous nuclear disaster site - to power its Azure AI infrastructure. Google signed power purchase agreements with next-generation nuclear startups. Amazon committed hundreds of millions to small modular reactor development. These are real investments, but they are essentially the same play: buy electricity from someone else on a long-term contract and hope the grid holds up.

OpenAI, if the Helion deal closes, is doing something structurally different. It is not buying electricity contracts. It is attempting to own the means of electricity production.

What Helion Actually Is - and Why It's Different

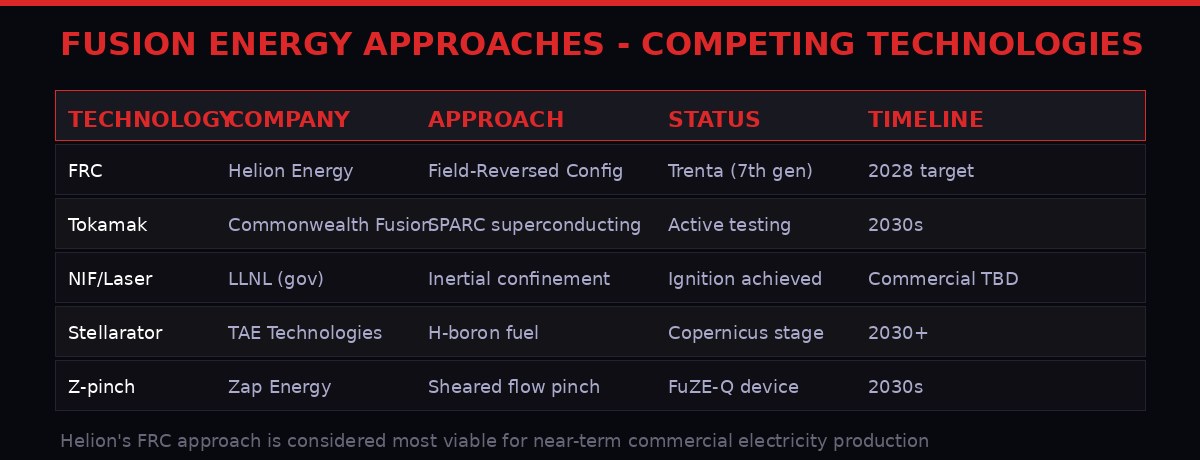

Most coverage of fusion energy treats every fusion company as interchangeable. They are not. The field is split between several fundamentally different physical approaches, and Helion's is the one that investors, physicists, and energy analysts have consistently ranked as most plausible for near-term commercial operation.

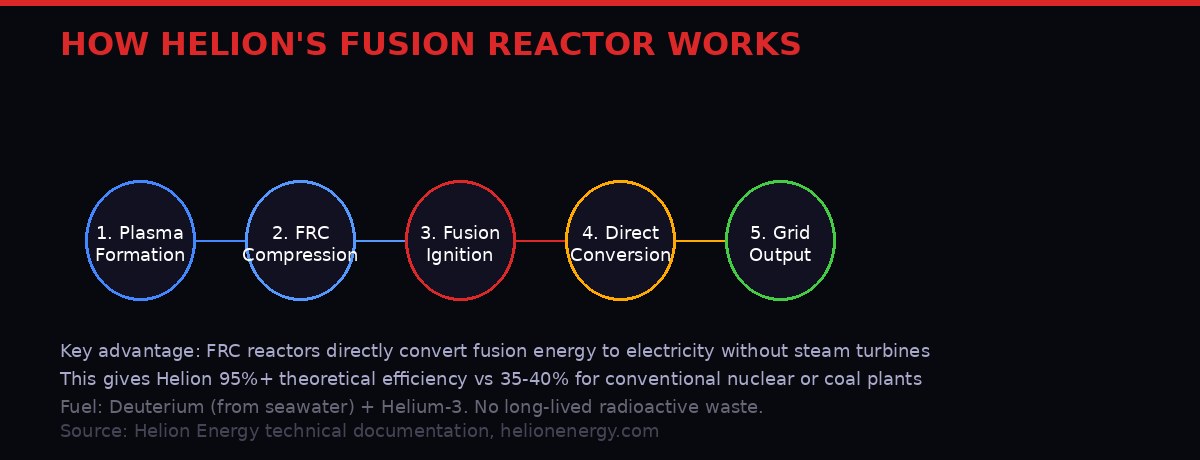

Helion uses a technology called Field-Reversed Configuration, or FRC. The basic principle: two "plasmoids" - blobs of superheated plasma - are accelerated toward each other from opposite ends of a cylindrical reactor. They collide and compress. At the moment of maximum compression, the plasma reaches fusion temperatures and the fusion reaction releases energy. The magnetic fields in the reactor capture that energy directly as electricity, without needing steam turbines or heat exchangers.

That last part matters more than people realize. Conventional nuclear power plants - and most other fusion reactor designs - generate heat, and then use that heat to boil water, and then use that steam to spin turbines, and then convert the turbine motion to electricity. Each conversion step loses efficiency. The theoretical ceiling for a conventional steam-cycle power plant, even a fusion one, is around 40 percent efficiency.

Helion's direct conversion approach sidesteps all of that. The company claims theoretical efficiency above 95 percent. Even accounting for real-world engineering losses and the energy needed to run the reactor itself, a commercial Helion plant would produce electricity at efficiencies far beyond anything currently on the grid.

Helion's seventh-generation device, called Trenta, became operational in 2023. The company has stated it reached plasma temperatures above 100 million degrees Celsius - hotter than the core of the sun, which is the threshold required for fusion. Trenta has not yet demonstrated net energy gain (producing more energy than it consumes), but Helion says its eighth-generation machine, Polaris, is designed to cross that threshold. (Source: Helion Energy company statements, helionenergy.com)

Microsoft had already signed a power purchase agreement with Helion in 2021 - a landmark deal committing Microsoft to buy Helion's electricity once it was commercially available, targeting 2028. The agreement included financial penalties if Helion missed the deadline. That contract is now potentially in the hands of Helion's acquirer, which would be OpenAI - Microsoft's biggest AI investment partner and, increasingly, its most direct AI competitor.

The Conflict Nobody Is Naming Clearly

Sam Altman's relationship with Helion has never been at arm's length. He personally invested in the company years before OpenAI had any interest in it. He was a founding backer. He became board chair. He has given interviews describing fusion energy as one of his most important personal bets - not as an OpenAI project, but as a thing Altman the person believes will define the next century.

Now his company is reportedly about to acquire the startup he founded, backed, chaired, and publicly championed. He stepped off the board the same day the acquisition talks were reported.

The sequence has a specific pattern: the board step-down is the standard legal prophylactic taken before a transaction is announced. You remove yourself from the board to remove the formal appearance of conflict before the deal is public. It happens all the time in M&A. It is also a fairly clean signal that a deal is close.

"OpenAI is in advanced talks with Helion Energy, the nuclear fusion startup that has a power purchase agreement with Microsoft, according to a person familiar with the matter." - Axios, reporting citing a person familiar with the matter, March 23 2026

Altman has recused himself from the discussions at OpenAI, according to reporting. But recusal at a company you lead as CEO is a governance formality, not an actual removal of influence. The board that will make this decision reports to a CEO who has had a decade of personal and financial commitment to Helion's success.

The second-order conflict is the Microsoft angle. Microsoft signed the Helion power agreement as an Azure customer, effectively subsidizing Helion's development in exchange for future cheap electricity. If OpenAI acquires Helion, Microsoft's power agreement now flows through a company that Microsoft nominally partners with but is actively competing against in AI services. The structural incentive to honor that agreement on favorable terms just changed. (Source: Microsoft-Helion PPA announcement 2021; Verge reporting March 23 2026)

Why This Matters Beyond OpenAI

The fusion acquisition story is not just about whether OpenAI gets cheaper electricity. It is about what happens to the AI industry if one company controls a potentially limitless clean energy source while competitors remain dependent on grid power that is increasingly constrained.

Computing power and energy are the two fundamental inputs of the AI race. Everything else - talent, data, algorithms - can be acquired or replicated. Electricity at scale, at a price that makes unlimited compute economically viable, is the actual binding constraint. The companies that secure cheap, abundant, reliable power will be able to run more inference, train larger models, iterate faster, and reduce the cost of AI services to the point where competitors cannot match them on price.

If Helion delivers commercial fusion electricity - a significant "if" that the physics community does not uniformly endorse - OpenAI with a captive fusion plant is in a structurally different competitive position than every other AI company on Earth. It would be the equivalent of one car manufacturer owning its own steel mill, rubber plantation, and oil refinery simultaneously.

If OpenAI acquires Helion and fusion power becomes commercially viable in the 2028-2030 window, the company will have solved the fundamental resource constraint of advanced AI at a time when regulators are still debating whether to treat OpenAI as a utility, a tech company, or something else entirely. The regulatory question suddenly becomes far more urgent.

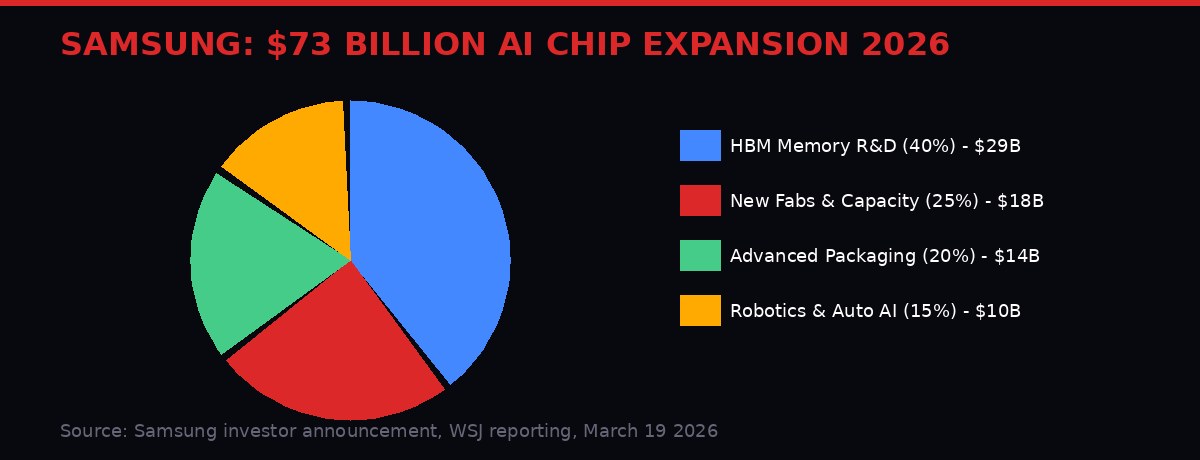

Samsung announced this same week it will spend $73 billion on AI chip expansion in 2026 - a 22 percent increase over its previous investment rate - specifically to compete with SK Hynix for Nvidia's memory business. (Source: Samsung investor announcement, WSJ, March 19 2026) The chip arms race is real and it is expensive. But chips are a commodity market; prices eventually fall. Energy, at the scale AI requires it, is not a commodity. It is constrained by physics, by land, by permitting, and by grid infrastructure that took decades to build.

The company that breaks the energy constraint breaks the race. That is what is actually at stake in the OpenAI-Helion talks.

OpenAI's Vertical Integration Playbook

The Helion deal, if it closes, is not an aberration. It is the logical endpoint of a strategy OpenAI has been executing for years, sometimes transparently and sometimes less so.

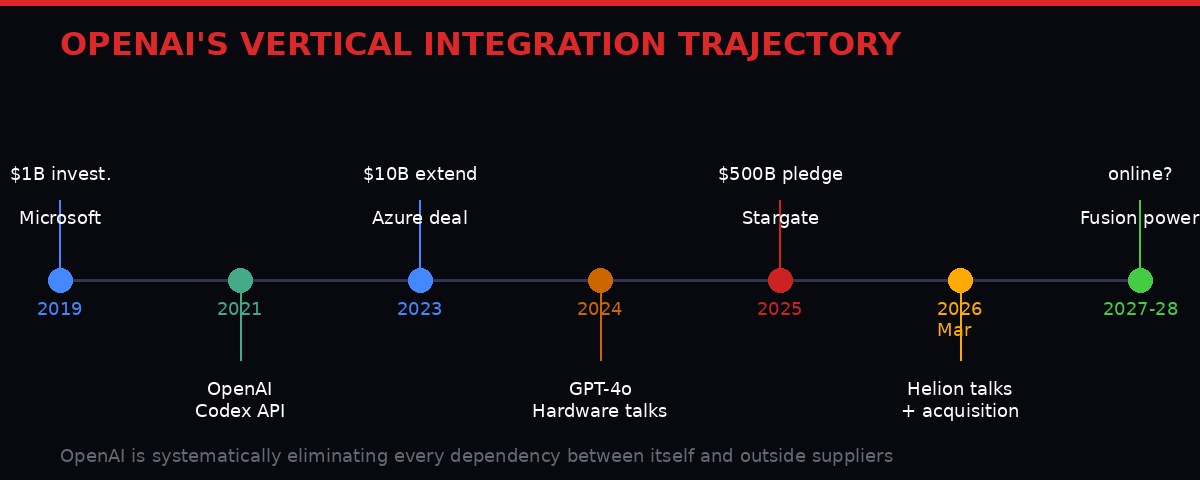

The pattern: identify every external dependency that constrains OpenAI's growth. Eliminate it. Microsoft was the first major dependency - solved through a partnership so deep that Azure became effectively an extension of OpenAI's infrastructure, with Microsoft's $13 billion investment functioning as a permanent cost-of-capital subsidy. The Stargate initiative announced in 2025, a $500 billion infrastructure commitment, was the next step: building out compute capacity at a scale no competitor can match in the short term. (Source: OpenAI Stargate announcement, January 2025)

The GitHub competitor announced earlier this year - a code repository platform - was interpreted by many as a product move. It was more accurately a supply chain move: eliminating the dependency on Microsoft's GitHub, which sits between OpenAI and its developer ecosystem. The acquisition of Promptfoo, the AI red-teaming company, was an attempt to bring security infrastructure in-house rather than relying on third-party testing that might constrain model deployment.

Helion is the energy version of this playbook. OpenAI's models currently run on power that is purchased from utilities and grid operators that have no particular reason to prioritize OpenAI's needs over any other customer. Grid power is subject to rate increases, supply disruptions, and political intervention. It is also constrained: in multiple US regions, new data center connections are backlogged by years because the grid simply does not have spare capacity.

A captive fusion plant, even a small one, changes the calculus. The first commercial Helion unit is expected to produce around 50 megawatts - enough to power a mid-sized data center. That is not enough to run OpenAI's entire operation. But it is a proof of concept, a template for scaling, and a negotiating position against every utility in the country that currently has OpenAI over a barrel on electricity pricing.

The Technical Realities the Hype Skips

Every honest account of the Helion acquisition has to include the physics caveats, because they are real and they matter.

Fusion has been "20 years away" for approximately 70 years. The joke predates the internet. The history of the field is littered with genuine breakthroughs that turned out to not be the breakthrough - moments where a laboratory result proved fusion was possible at some scale under some conditions, followed by years of engineering work that revealed new obstacles at every layer.

Helion's FRC approach has achieved fusion temperatures. That is a real result. What it has not achieved is net energy gain - putting more energy out of the reactor than goes in to run it. The company says Polaris, its eighth-generation machine, will cross that threshold. Polaris is under construction. Polaris has not been operated yet. The 2028 commercial deadline that Microsoft's contract is pegged to assumes Polaris works as designed, that the engineering challenges of scaling from a research machine to a power plant are solvable on schedule, and that the regulatory process for what is effectively a new category of nuclear facility proceeds smoothly in a political environment that is currently hostile to federal permitting timelines.

None of those assumptions are crazy. None of them are guaranteed. The scientific consensus is that Helion's approach is more credible than most fusion claims - but the scientific consensus also acknowledges that significant unsolved problems remain. (Note: Fusion energy assessments drawn from IEA, DOE publications, and academic fusion physics literature.)

"The field-reversed configuration approach is genuinely promising. The direct energy conversion concept is elegant and theoretically sound. The question is always whether the engineering can keep up with the physics, and at what cost." - Paraphrase of the general expert view in fusion energy assessment literature; no individual expert attribution claimed

For OpenAI, these risks are probably acceptable in the context of the acquisition price. Helion's last valuation was approximately $3.3 billion, set during its 2021 fundraising round. (Source: Helion Energy funding disclosures) OpenAI, with its current scale, could absorb that cost even if Polaris never achieves commercial viability. The option value of owning a fusion company that might work is worth more than the cost of the acquisition at that price, even if the probability of success is below 50 percent.

The real risk is the one nobody at OpenAI is publicly discussing: if Helion fails and the acquisition price is much higher than the 2021 valuation implies, OpenAI will have made a high-profile, expensive bet on fusion that did not pay off. In an environment where the company is also dealing with Pentagon lawsuits, governance controversies, and regulatory scrutiny, a failed fusion acquisition would be a significant reputational and financial wound.

Timeline: The Helion-OpenAI Connection

What Happens to the Rest of the Market

Assume the deal closes. Assume Helion, under OpenAI ownership, continues on its current development timeline. What does the competitive landscape look like in 2028 when the first commercial electricity comes online?

First, the Microsoft angle deserves more attention. The existing power purchase agreement between Microsoft and Helion was negotiated when both parties were at arm's length. If OpenAI owns Helion, Microsoft is buying electricity from a competitor. The incentive to honor the agreement generously, to prioritize Microsoft's power allocation, or to share Helion's technical advances with Microsoft's own AI infrastructure is zero. Microsoft's lawyers will have scrutinized this scenario when they got wind of the acquisition talks - and if the deal closes, expect either renegotiation of that contract or protracted legal disputes about its terms.

Second, every other AI company that is currently dependent on grid power should consider this development a fire alarm. Google, Amazon, Meta, and the second tier of AI startups are all building infrastructure that assumes energy will be purchased, not owned. If OpenAI solves the energy problem through vertical integration, the competitive moat it creates is not just about lower electricity bills - it is about the ability to run compute at a scale that grid-dependent competitors cannot match without regulatory intervention.

Third, the regulators. OpenAI is already under antitrust scrutiny in multiple jurisdictions for its relationship with Microsoft. Acquiring a nuclear energy company - even a pre-commercial fusion startup - puts OpenAI into a regulatory category it has not occupied before. Fusion power plants require licensing by the Nuclear Regulatory Commission. The intersection of AI safety concerns, energy infrastructure control, and antitrust is a new problem for every agency that has jurisdiction over any piece of it. (Source: NRC licensing requirements for fusion facilities, current regulatory framework)

The EU's AI Act, still being implemented, contains provisions about critical infrastructure. If Helion generates electricity that flows into European grids - a distant but possible scenario once the technology scales - OpenAI's AI regulatory obligations and its energy infrastructure obligations start to collide in ways that no regulatory framework currently anticipates.

Fourth, the talent and research spillover. Helion employs some of the best plasma physicists in the world. Many of them chose fusion research specifically because it is not Big Tech - it is slow-moving, technically rigorous, and oriented toward a decades-long scientific problem rather than a quarterly product cycle. Some of them will thrive under OpenAI ownership. Some will leave. The departure of Helion's core physics team would be the most serious risk to the technical roadmap, and it is not a risk that a term sheet can fully mitigate.

The Bigger Picture: Who Controls the Inputs of the Future

The Helion acquisition attempt is the clearest signal yet that the AI industry's real competition is not about models, interfaces, or benchmarks. Those are proxies. The real competition is about who controls the three fundamental inputs of artificial intelligence at scale: compute, data, and energy.

The compute fight is well understood. The chip shortage, the Nvidia dependency, the TSMC bottleneck - these are constant news. The data fight is increasingly understood - the ongoing legal battles over training data, the web scraping restrictions, the deals with publishers and academic institutions. The energy fight has been quieter, because energy as a constraint has felt abstract. Grid power is expensive, but it exists. The bottleneck was always chips, not watts.

That calculus is changing. The models being trained for the 2027-2030 window are projected to require energy inputs at a scale that grid-connected data centers in the current regulatory environment cannot support. The power purchase agreements being signed now are for capacity that will be delivered years late, at prices that will increase, from grids that were not designed for this load. The OpenAI-Helion bet, at its core, is a bet that this problem gets worse faster than anyone is publicly acknowledging, and that the company that solves it first wins something more valuable than a cost reduction.

Samsung's $73 billion chip bet, announced the same week, is the conventional response to AI's resource constraints - pour money into the established infrastructure, outcompete on cost and scale within the known framework. That will work. It will make Samsung more money and provide more chips to more AI companies at marginally better prices.

The Helion bet is asking a different question: what if the framework itself changes? What if clean, near-limitless electricity becomes available at a cost so low that the current chip economics collapse anyway, because you can run the chips you have continuously without worrying about the power bill? What if the company that owns that electricity source does not sell it to competitors?

The hearing for the Anthropic-Pentagon preliminary injunction was scheduled for this same week, March 24 in San Francisco. The AI industry's relationship with government, with energy, with compute suppliers, and with its own growth constraints is entering a new phase simultaneously on multiple fronts. The Helion acquisition attempt is the energy front opening. It will not be the last front, and it may be the most consequential one.

The fusion race and the AI race just merged into the same race. The finish line is whoever builds a model smart enough to run itself on power plants that did not exist five years ago. That is not a metaphor. That is the business plan.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram