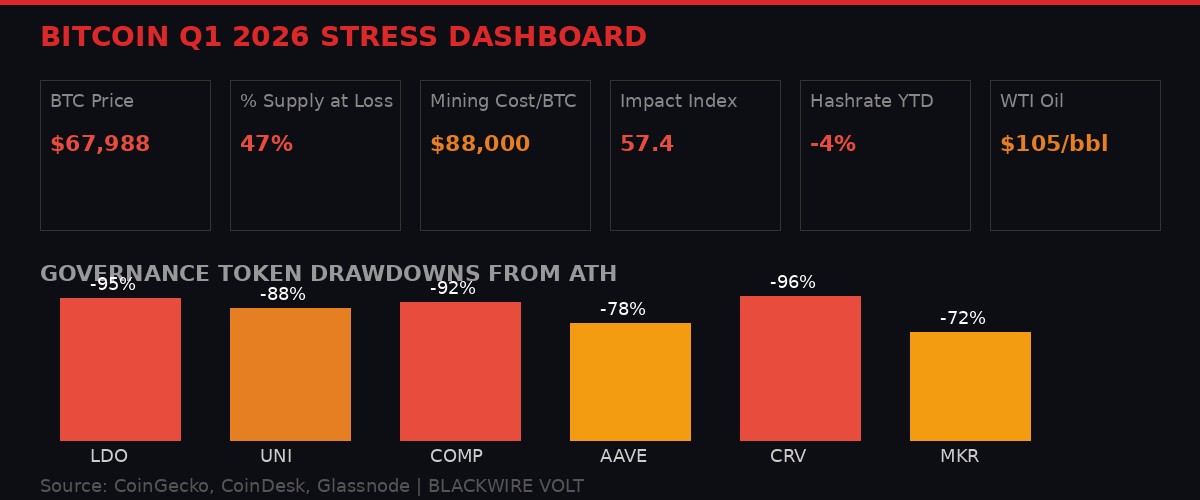

The numbers tell the story: 47% of all bitcoin supply is underwater, hashrate is declining for the first time in six years, and oil above $100 is crushing mining margins.

The first quarter of 2026 is over. It was supposed to be the year bitcoin consolidated above $100,000, institutions piled in through ETFs, and DeFi governance tokens finally got their repricing higher. None of that happened.

Instead, bitcoin is closing Q1 at roughly $68,000 - down more than 45% from its October 2025 all-time high of $126,000. Nearly half of all circulating supply is at a loss. The mining industry is hemorrhaging money at a rate of $19,000 per bitcoin produced and fleeing into artificial intelligence contracts. DeFi's largest staking protocol is proposing to buy back its own governance token because nobody else will. And the last major corporate bitcoin buyer just broke its purchasing streak.

This isn't a correction. This is a reckoning. Q1 2026 exposed every structural weakness in crypto's thesis - from mining economics to governance token value to the assumption that institutional capital only flows in one direction. What follows is the full autopsy.

The Mining Exodus: $70 Billion in AI Contracts and a Hashrate in Retreat

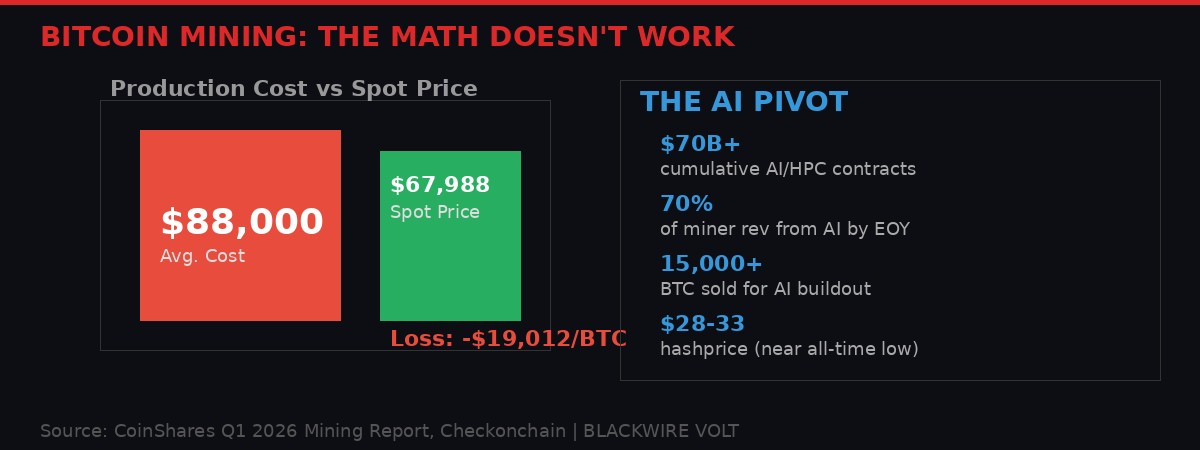

The math behind the mining exodus: production costs at $88,000 per BTC versus a $68,000 spot price, while AI infrastructure contracts offer 85%+ margins.

For the first time since 2020, bitcoin's hashrate declined during a first quarter. It's currently down roughly 4% year to date, hovering around 1 zettahash per second after peaking at approximately 1,160 exahashes per second in early October 2025, according to Glassnode data. Over the previous five years, hashrate had surged tenfold, rising every Q1 without exception and posting full-year growth above 10% annually.

The decline didn't happen because miners lost interest in bitcoin. It happened because the economics broke.

Checkonchain's difficulty regression model pegged the average production cost at $88,000 per bitcoin as of mid-March. With bitcoin trading near $68,000, that's a gap of roughly $20,000 per coin - a 23% loss on every block mined. The average publicly listed miner spent $79,995 to produce one BTC in Q4 2025, according to CoinShares' Q1 2026 mining report. The number has only gotten worse since.

Hashprice - the metric tracking expected miner revenue per unit of computing power - dropped to $28-33 per petahash per second per day in March, according to Luxor's Hashrate Index. That's near its all-time post-halving low, reached on February 23. At those levels, miners running mid-generation hardware need electricity below $0.05 per kilowatt-hour to stay cash-positive. Most don't have it.

The Iran war made everything worse. Oil above $100 per barrel feeds directly into electricity costs for mining operations, particularly the estimated 8-10% of global hashrate running in energy markets sensitive to Middle Eastern supply. The Strait of Hormuz, handling roughly 20% of global oil and gas flows, remains effectively closed to most commercial traffic. WTI crude hit $105 per barrel on Monday, closing above the $100 mark for the first time since 2022.

Network difficulty dropped 7.76% on March 22 to 133.79 trillion - the second-largest negative adjustment of 2026 after February's 11.16% plunge during Winter Storm Fern. Difficulty is now nearly 10% below where it started the year and well below November 2025's all-time high of 155 trillion. Average block times stretched to 12 minutes and 36 seconds during the last epoch, above the 10-minute target that signals healthy network participation.

The rational response for miners was obvious: pivot to something profitable. And they did, at a scale nobody predicted.

The AI Pivot: Bitcoin Miners Are Becoming Data Center Companies

The future of bitcoin mining companies isn't bitcoin - it's rows of GPUs serving AI workloads at margins mining can no longer touch.

Over $70 billion in cumulative AI and high-performance computing contracts have been announced across the public mining sector, according to CoinShares. This isn't a side experiment. This is a wholesale industry transformation happening in real time.

CoreWeave's expanded deal with Core Scientific alone is worth $10.2 billion over 12 years. TeraWulf has $12.8 billion in contracted HPC revenue. Hut 8 signed a $7 billion, 15-year lease for AI infrastructure at its River Bend campus. Cipher Digital has a multi-billion-dollar agreement with Google-backed Fluidstack. These aren't future promises. These are signed contracts with revenue visibility stretching a decade or more.

Listed miners could derive as much as 70% of their revenue from AI by the end of 2026, up from roughly 30% today. Core Scientific's AI colocation revenue already accounts for 39% of its total. TeraWulf is at 27%. IREN is at 9% and scaling rapidly with up to 200 megawatts of liquid-cooled GPU capacity under construction.

The cost differential explains the urgency. Bitcoin mining infrastructure runs $700,000 to $1 million per megawatt. AI infrastructure costs $8 million to $15 million per megawatt - but offers structurally higher and more stable returns. AI contracts promise margins above 85% with multi-year revenue visibility. Bitcoin mining margins are currently negative.

The transition is being financed two ways. First, debt. The sector's aggregate leverage has changed fundamentally. IREN now carries $3.7 billion in convertible notes across five series. TeraWulf has $5.7 billion in total debt, split between convertible notes and senior secured notes at its compute subsidiary. Cipher Digital issued $1.7 billion in senior secured notes in November, causing its quarterly interest expense to surge from $3.2 million for the first nine months to $33.4 million in Q4 alone.

Second, bitcoin sales. Publicly listed miners have collectively reduced their BTC treasuries by over 15,000 BTC from peak levels. Core Scientific sold roughly 1,900 BTC worth $175 million in January and is planning to liquidate substantially all remaining holdings in Q1 2026. Bitdeer reduced its treasury to zero in February. Riot Platforms sold 1,818 BTC worth $162 million in December.

Even Marathon Digital, the largest public holder at 53,822 BTC, quietly expanded its policy in its March 10-K filing to authorize sales from its entire balance sheet reserve. The pressure point: its $350 million bitcoin-backed credit facility saw its loan-to-value ratio climb to 87% as prices fell toward $68,000. A few more thousand dollars down and that facility triggers margin calls.

The valuation market has already priced the split. Miners with secured HPC contracts now trade at 12.3x next-twelve-month sales. Pure-play miners trade at 5.9x. The market is paying more than double for AI exposure, reinforcing the incentive to pivot further.

The implication for bitcoin's security model is real but nuanced. When the companies securing the network are selling their bitcoin to fund AI buildouts, the network's economic security budget shrinks. Three consecutive negative difficulty adjustments - the first such streak since July 2022 - confirm the stress. But a more geographically distributed hashrate, with publicly listed U.S. miners losing their 40%+ global share, could actually improve decentralization even as total hashpower declines.

Half of Bitcoin Is Underwater: The Impact Index Hits Red

The capital flow picture flipped entirely in late March: stablecoin inflows became outflows, ETFs moved to selling, and miners accelerated liquidation.

The Bitcoin Impact Index, which measures financial stress across user cohorts based on onchain behavior, ETF activity, derivatives positioning, and liquidity flows, surged 13 points to 57.4 during the week ended March 28. That's its steepest climb since January and places it in the "high impact" zone that historically preceded double-digit price drops in 2018, 2022, and earlier this year, according to CEX.IO's weekly analysis.

The headline number: 47% of all circulating bitcoin supply is now held at a loss. Not 20%. Not 30%. Nearly half.

Long-term holders - wallets that have held BTC for more than six months - were selling at a profit just a week ago when bitcoin traded above $70,000. Now, over 4.6 million BTC from these wallets, roughly 30% of their total holdings, are underwater. Their realized losses last week were the worst since 2023.

"This kind of divergence between price action and on-chain conviction has historically been a warning sign. Similar moves occurred in mid-2018 and mid-2022 before price drops of over 25%." - CEX.IO Bitcoin Impact Index Report, Week 13

Short-term holders aren't faring better. The data shows a classic distribution pattern: stress across every cohort simultaneously, with no clear subset of the market acting as a stabilizing buyer.

Capital flows that had supported the market earlier in March reversed sharply. Daily stablecoin net flows, which had averaged inflows of $250 million, flipped to outflows of $292 million. ETFs and miners moved from accumulation to selling. The buying power that had formed a floor at $66,000-$68,000 is thinning.

One metric remains intact as a guardrail against full capitulation: holders are not rushing to deposit BTC on exchanges en masse. That behavior - the flood of coins moving to exchange hot wallets - has historically marked the final wave of panic selling. It hasn't materialized yet. Whether that's conviction or inertia is the question nobody can answer with onchain data alone.

The broader crypto market value has declined by approximately $2 trillion from October 2025 peaks. Crypto-linked equities are down roughly 60% from highs. The correction isn't a blip on a chart. It's the kind of sustained drawdown that forces entire business models to change - which is exactly what's happening in mining, in DeFi, and in corporate treasury strategy.

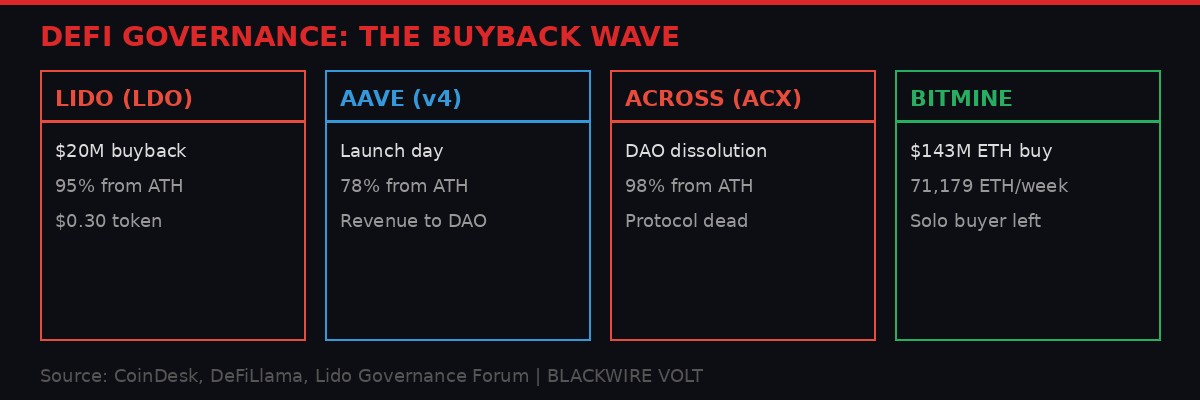

Lido's $20 Million Buyback: When the Biggest DeFi Protocol Can't Find Buyers

The DeFi governance token crisis in four cards: Lido buying back its own token, Aave launching v4 in survival mode, Across dissolving, and BitMine standing as the lone corporate buyer.

Lido DAO, the protocol controlling roughly 23% of all staked ether on Ethereum, proposed spending up to 10,000 stETH - approximately $20 million at current prices - to buy its own governance token. The proposal, posted by the Lido Ecosystem Operations team over the weekend on the Lido governance forum, reads less like a strategic capital allocation plan and more like an emergency intervention.

LDO hit an all-time low of $0.27 on March 7 and currently trades near $0.30, according to CoinGecko data, with a market capitalization of roughly $258 million. The token is down more than 95% from its 2021 peak of $7.30. At current prices, the proposed buyback could absorb roughly 65 million tokens - about 8% of the circulating supply.

The problem isn't that Lido wants to buy. It's that onchain LDO liquidity sits at about $90,000 of depth at plus-or-minus 2%. That means a single 1,000 stETH batch - roughly $2 million - executed onchain would blow through available liquidity multiple times over. Ethereum's largest liquid staking protocol has to go offchain to buy its own token at scale.

The proposal authorizes the Lido Growth Committee to route trades through centralized exchanges including Binance, OKX, Bybit, Gate, and Bitget, each of which currently offers more than $100,000 in depth. It also permits engaging market-maker partners on behalf of the Lido Ecosystem Foundation to facilitate execution. Slippage is capped at 3% below the reference price. Execution proceeds in 1,000 stETH batches, each requiring a separate Easy Track motion with a three-day objection period.

"This is not a routine fluctuation. It represents one of the most significant dislocations between LDO's market price and its underlying protocol fundamentals in the token's history." - Lido Ecosystem Operations Team, Governance Proposal

The DAO's argument rests on a gap between market price and fundamentals. The LDO-to-ETH ratio sits at approximately 0.00016, a 70% discount to levels that held for most of the past two years. Net protocol rewards have dropped only about 20% over the same period, while costs improved 13% year-over-year and the effective take rate rose to 6.11% from 5%. Lido still dominates liquid staking on Ethereum, per DefiLlama data.

But Lido's problem isn't unique. It's structural. LDO's 95% drawdown from peak is extreme but not an outlier in the governance token category. UNI is down 88%. COMP is down 92%. CRV is down 96%. These are protocols that generate fees, hold billions in TVL, and dominate their respective sectors. The market has collectively decided that governance tokens - even ones controlling fee switches over profitable protocols - are worth almost nothing when they distribute nothing.

The deeper question Lido's buyback surfaces is whether governance tokens can ever trade on fundamentals at all, or whether they're permanently stuck as speculative instruments disconnected from the protocols they nominally control. A buyback addresses supply. It doesn't address the category's existential problem: nobody knows what a governance token should be worth.

Aave v4: DeFi's Biggest Upgrade Lands in a Wasteland

Aave's v4 upgrade aims to bridge DeFi into real-world credit markets - but it's launching into the worst sentiment environment DeFi has ever faced.

Aave, one of the largest decentralized lending platforms, debuted its long-awaited v4 upgrade on Ethereum on Sunday. The timing - launching during the worst governance token bear market in DeFi history - is either terrible or exactly right, depending on your time horizon.

The upgrade, in development for approximately two years, fundamentally changes how Aave organizes its markets. Instead of grouping everything together, the new system allows different types of lending markets to operate separately while still sharing the same pool of funds. That means users could eventually borrow and lend against more than just crypto tokens - the architecture is designed to support real-world assets, institutional borrowing, and complex credit products.

"Lending is based on trust - you need lending conditions that reflect market conditions," Aave Labs founder Stani Kulechov told CoinDesk. "DeFi is stronger than ever. A lot of these opportunities will come from value outside of DeFi."

The v4 architecture also introduces technical improvements allowing idle float capital to be reinvested more efficiently, and it opens the protocol for third-party builders to extend the infrastructure. It went live with a limited set of markets and conservative settings, with more features likely to follow through governance decisions.

The launch follows months of internal turbulence at Aave. Disputes over interface fees, contributor roles, and proposals to redirect product revenue to the DAO highlighted tensions between decentralization and operational coordination. Two governance teams walked away from the protocol earlier this month, contributing to an 11% AAVE price drop. The "Aave Will Win" plan proposed in February - sending 100% of product revenue to the DAO - was an acknowledgment that the governance token model needs radical restructuring to survive.

Whether Aave v4 actually attracts real-world credit markets into DeFi depends on factors far beyond the protocol's technical capabilities. Regulatory clarity, institutional trust, and a market that isn't in freefall would help. But the upgrade is real, the code is live, and the architecture is the most advanced lending infrastructure DeFi has produced. It just landed in a market that's too beaten down to notice.

Strategy Breaks Its Streak: The Last Corporate Buyer Goes Quiet

Strategy's 13-week bitcoin buying streak ended last week - and with it, the market's most reliable source of institutional demand.

Strategy (MSTR), the largest corporate bitcoin holder, appears to have paused its bitcoin accumulation last week, ending a 13-week buying streak. The company, led by Michael Saylor, had been the market's most consistent large-scale buyer since December 2025, absorbing thousands of BTC per week through convertible note issuances and equity offerings.

The pause leaves BitMine Immersion Technologies (BMNR) as the only major corporate crypto buyer still actively accumulating at scale. BitMine purchased 71,179 ETH last week - its largest weekly buy of 2026 - bringing total holdings to over 4.73 million ETH, roughly 3.92% of the token's supply. The company, chaired by Tom Lee of Fundstrat, has increased its buying pace for four consecutive weeks.

BitMine's $143 million weekly purchase contrasts sharply with the rest of the market. Every other large digital asset treasury has either paused or reduced holdings during the downturn. The company's total crypto and cash holdings stand at $10.7 billion, including 197 BTC and $961 million in cash and equity stakes.

The Strategy-BitMine divergence illustrates a broader split in corporate crypto strategy. Strategy has been bitcoin-only since 2020, accumulating through a series of increasingly large debt issuances. BitMine went all-in on ether, betting on the Ethereum ecosystem's fee generation and staking yields. With ETH trading near $2,000 - down significantly from its 2024 highs - BitMine is buying into weakness while Strategy has pulled back.

For the broader market, Strategy's pause removes a key demand floor. The company's weekly purchases had become a structural bid that traders factored into their positioning. Without it, the market loses its most predictable source of non-speculative buying.

Trump-backed American Bitcoin reached 7,000 BTC in holdings, roughly tripling since its Nasdaq debut. Satoshis per share climbed past 660. But even that aggressive accumulation hasn't prevented the stock from sliding - shares fell even as reserves surged and bitcoin exposure per share increased. The market isn't rewarding bitcoin accumulation right now. It's punishing exposure to an asset that half the holders are losing money on.

Oil at $105, Powell Holds: The Macro Vise Tightens

WTI crude above $105 per barrel - the highest close since 2022 - is crushing risk assets while the Fed holds rates steady, creating a policy trap with no clean exit.

Federal Reserve Chairman Jerome Powell spoke at Harvard University on Monday and delivered what should have been reassuring commentary. The Fed, he said, is "looking past short-term oil price shocks" and focusing on inflation expectations that remain "well anchored." He gave no indication of imminent rate hikes.

The bond market liked it. The 10-year Treasury yield fell nine basis points to 4.35%. The 2-year yield slid eight basis points to 3.83%. Odds of one or more Fed rate hikes in 2026 collapsed to 5% from 25% on Friday, according to CME FedWatch.

Stocks didn't care. The Nasdaq closed down 0.75%. The S&P 500 fell 0.4%. Bitcoin gave up early gains and retreated to $66,500 before recovering slightly. The problem wasn't Powell. The problem was oil.

WTI crude rose 5.3% on Monday to just under $105 per barrel, closing above $100 for the first time since 2022. The Iran war has kept energy markets in a perpetual state of supply anxiety. Trump's weekend threats to "obliterate" Iran's power plants, oil wells, and Kharg Island if a deal isn't reached have added a war premium that isn't going away.

"We will eventually maybe face the question of what to do here," Powell said. "We're not really facing it yet because we don't know what the economic effects will be."

That's the trap. The Fed can hold rates steady while oil stays at $105. It cannot hold rates steady if oil pushes to $120 or $130 and that spike feeds into core inflation. The moment "transitory energy shock" becomes "embedded inflation expectations," the rate hike conversation restarts. And rate hike bets aren't just a Fed story - the Bank of Japan is also seeing mounting pressure for tightening, creating the risk of a carry trade unwind that would hit risk assets from both directions simultaneously.

For crypto specifically, the macro vise operates through two channels. First, energy costs directly impair mining economics, as detailed above. Second, tighter financial conditions reduce speculative appetite, compressing valuations on risk assets across the board. Bitcoin's correlation with traditional risk assets has increased during the downturn, undermining the "digital gold" narrative that was supposed to provide refuge in exactly this environment.

Bernstein Calls the Bottom: Crypto Stocks at "Big Discounts"

Bernstein's revised targets still imply massive upside - but the call requires faith that sentiment normalizes in Q2-Q3.

Wall Street broker Bernstein published the most bullish crypto equity note in months on Monday, arguing that the roughly 60% drawdown in crypto-linked stocks from 2025 highs has created "big businesses at big discounts."

"The combination of geopolitics and temporary crypto weak sentiment is offering big discounts on crypto stocks," analysts led by Gautam Chhugani wrote. The firm maintained outperform ratings on Coinbase (COIN), Robinhood (HOOD), and Figure (FIGR) while lowering price targets to account for near-term weakness.

Coinbase's target dropped to $330 from $440. The stock trades at $165.50 - a 100% implied upside. Robinhood's target fell to $130 from $160. It trades at $67.10 - a 94% implied upside. Figure's target was lowered to $67 from $72, versus a $31.14 trading price - a 115% implied upside.

The broader call: bitcoin has found its bottom and is primed for further gains, with a reiterated $150,000 year-end target. That implies a 121% rally from current levels in roughly nine months.

Bernstein's thesis rests on a few pillars. First, the selloff has been driven by macro pressure - primarily oil shocks and geopolitical risk - rather than deteriorating crypto fundamentals. Stablecoin adoption is accelerating. Tokenization is progressing. Prediction markets and derivatives volumes are growing. Second, crypto equities are approaching a valuation floor heading into weak Q1 earnings that the market has already priced. Third, the regulatory backdrop has improved materially, with stablecoin legislation advancing and 401(k) access opening up trillions in retirement capital to crypto assets.

The bearish case is equally simple: the macro environment hasn't stabilized. Oil is still rising. The Iran war could escalate further. Rate hike risk, while diminished after Powell's comments, hasn't disappeared. And 47% of bitcoin's supply sitting at a loss creates structural selling pressure whenever price rallies into resistance - holders who bought above $68,000 will sell to get back to breakeven, capping upside until sufficient time passes or a catalyst changes the calculus.

For now, the market is caught between Bernstein's "buy the blood" thesis and onchain data screaming caution. Q1 ends with that tension unresolved.

The Privacy Bet: Hoskinson's $200 Million Midnight Launch

Charles Hoskinson is betting $200 million that privacy - not speed, not scalability - is the missing piece that keeps crypto locked out of the real economy.

While the rest of the market bleeds, Charles Hoskinson shipped. Midnight, a blockchain the Cardano founder funded with roughly $200 million of his own capital, went live on Monday. The thesis: crypto failed to achieve mass adoption not because of regulation or volatility, but because of usability. Too complex, too public, too risky for normal people to use.

"The question I've been asking for eight years is: why didn't the revolution happen?" Hoskinson said in an interview with CoinDesk.

Midnight introduces what Hoskinson calls "selective disclosure" - a system allowing users to prove specific things about themselves without revealing underlying data. The network enables confidential financial products, identity systems, and enterprise data workflows. Users tap, authenticate, and transact without needing to understand the underlying blockchain mechanics.

The launch included one of the largest airdrops in industry history, reaching 37 million wallets across eight blockchains. London-based Monument Bank announced plans to tokenize up to 250 million pounds ($330 million) in retail deposits on Midnight - one of the first examples of a regulated bank bringing customer funds onto a public blockchain while maintaining privacy protections.

Whether Midnight matters depends entirely on execution. Privacy-focused blockchains have been promised before. Zcash, which Grayscale highlighted this week as a "mispriced bet on confidentiality" in an AI-driven surveillance world, holds a tiny market share despite real usage metrics. The privacy thesis is compelling. The market hasn't rewarded it yet.

But Hoskinson's timing - launching a privacy layer while every transaction on every public blockchain is increasingly tracked, analyzed, and taxed - might be the first genuinely contrarian move in a market full of people claiming to be contrarian.

What Q2 Looks Like From Here

Q2 opens with every structural support weakened: corporate buyers pausing, miners selling, capital flowing out, and macro risk unresolved.

Q1 2026 leaves the crypto market in a precarious equilibrium. The structural buyers that supported previous downturns - miners holding, corporate treasuries accumulating, ETFs absorbing supply - have all either reversed or paused. The macro environment is hostile and worsening. And the DeFi sector is in an identity crisis that governance buybacks and protocol upgrades can't resolve on their own.

The bullish case requires several things to go right simultaneously: the Iran situation de-escalating enough to pull oil back below $90, the Fed maintaining its dovish hold through summer, 401(k) crypto access converting from policy proposal to actual capital inflows, and bitcoin holding above $60,000 long enough for onchain cost basis to adjust downward.

The bearish case requires only one thing to go wrong: oil pushing to $120, triggering rate hike fears, compressing risk asset valuations further, forcing more miner capitulation, and creating a reflexive cycle where lower prices cause more selling which causes lower prices.

The numbers heading into Q2:

- BTC: ~$68,000, down 45% from ATH. 47% of supply at a loss. Impact Index at 57.4.

- Hashrate: ~920 EH/s, down 4% YTD. First Q1 decline in six years.

- Mining cost: $88,000/BTC. Negative margins for most operators.

- Oil: $105/bbl WTI. Highest close since 2022.

- Stablecoin flows: Flipped to -$292M/day from +$250M/day.

- Corporate buying: Strategy streak broken. BitMine sole active buyer.

- Governance tokens: LDO -95%, UNI -88%, COMP -92%, CRV -96% from ATH.

- Bernstein BTC target: $150,000 by year-end (121% upside from here).

The market priced for the worst isn't always wrong. But it isn't always right either. Q1 is over. The damage is documented. Now the question is whether anything changes, or whether Q2 becomes the quarter where the structural cracks become structural failures.

Watch oil. Watch miner selling. Watch stablecoin flows. Everything else is noise.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram