SpaceX Files for the Largest IPO in History - $1.75 Trillion Valuation, $75 Billion Raise, and the 21-Bank Army Behind Project Apex

SpaceX filed confidentially with the Securities and Exchange Commission on Wednesday, formally beginning the process for what will be the largest initial public offering in recorded financial history. The company, founded by Elon Musk in 2002 to build reusable rockets, is targeting a valuation of $1.75 trillion and hopes to raise as much as $75 billion in fresh capital. That figure alone would triple the previous record for an IPO raise. Bloomberg broke the news first, citing anonymous sources familiar with the matter. CNBC's David Faber independently confirmed the filing within minutes. Reuters followed with its own sourcing.

The filing landed on a day when global markets were already on edge. The Nasdaq is coming off its steepest weekly decline in nearly a year. Oil prices remain elevated from the ongoing U.S.-Iran conflict. And the man behind this offering - Elon Musk, the world's richest person with a net worth approaching $840 billion according to Forbes - is simultaneously running Tesla, overseeing X, building xAI, and advising the White House on government efficiency. The SpaceX IPO is not merely a financial event. It is a stress test for modern capital markets.

Project Apex - Inside the Codename and the 21-Bank Syndicate

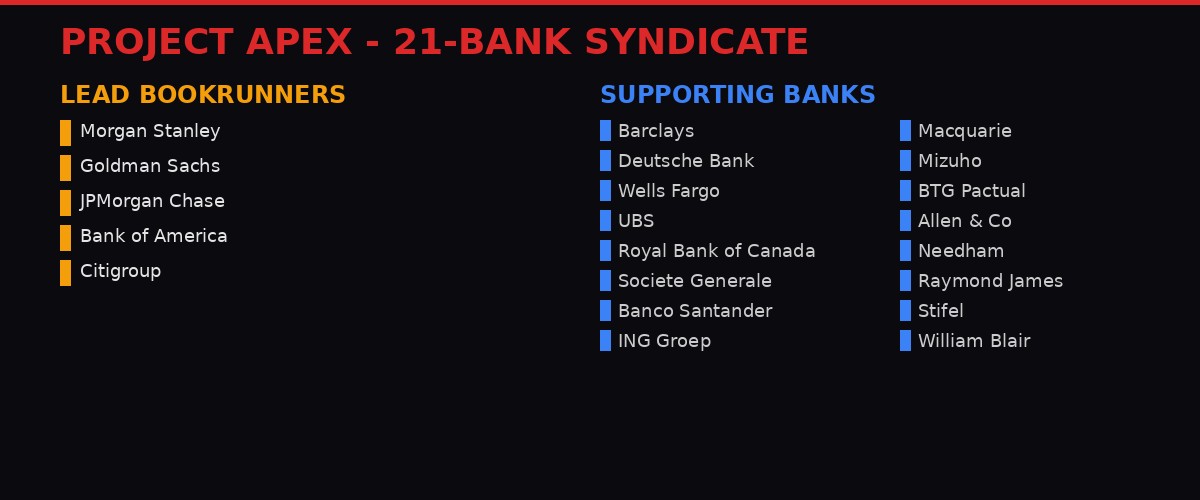

Internally, SpaceX has codenamed the IPO "Project Apex." The name fits. This is not a routine listing. Reuters reported on March 31 that SpaceX has assembled an unusually large syndicate of 21 banks to manage the offering, one of the biggest underwriting groups assembled in recent memory. For comparison, when Arm Holdings went public in 2023, it used nearly 30 banks, and Alibaba assembled a similarly large group for its 2014 debut. But neither of those were attempting a $75 billion raise.

Five banks are serving as lead bookrunners on the deal. Morgan Stanley, Goldman Sachs, JPMorgan Chase, Bank of America, and Citigroup will manage the core of the transaction. These are Wall Street's heaviest hitters, the firms that handle the most consequential listings on Earth. They will divide responsibilities across institutional investors, sovereign wealth funds, high-net-worth individuals, and retail participants spanning multiple continents.

The supporting cast includes another 16 banks in smaller roles: Barclays, Deutsche Bank, Wells Fargo, UBS, Royal Bank of Canada, Societe Generale, Banco Santander, ING Groep, Macquarie, Mizuho, BTG Pactual, Allen & Co, Needham & Company, Raymond James, Stifel, and William Blair. The geographic spread of the syndicate signals that SpaceX is not just courting American buyers. This offering is designed to attract capital from Europe, Asia, Latin America, and the Middle East.

Under SEC rules, a private company can file its IPO registration statement confidentially at least 15 days before it begins marketing shares to public investors. This allows SpaceX to receive regulatory feedback in private, adjust its filings if needed, and control the narrative before the roadshow begins. The confidential filing window means public investors will not see SpaceX's detailed S-1 financials until the company is ready to hit the road. That roadshow is expected to launch in late May, with a target listing date of June 2026.

Several banks including Goldman Sachs, JPMorgan, and Wells Fargo declined to comment when contacted by journalists. SpaceX itself has not responded to requests for comment. Musk has reportedly scheduled an investor briefing for later in April to address questions about the offering's structure, financial details, and forward plans.

The Numbers - $16 Billion in Revenue, $8 Billion in Profit, and a 38x Multiplier

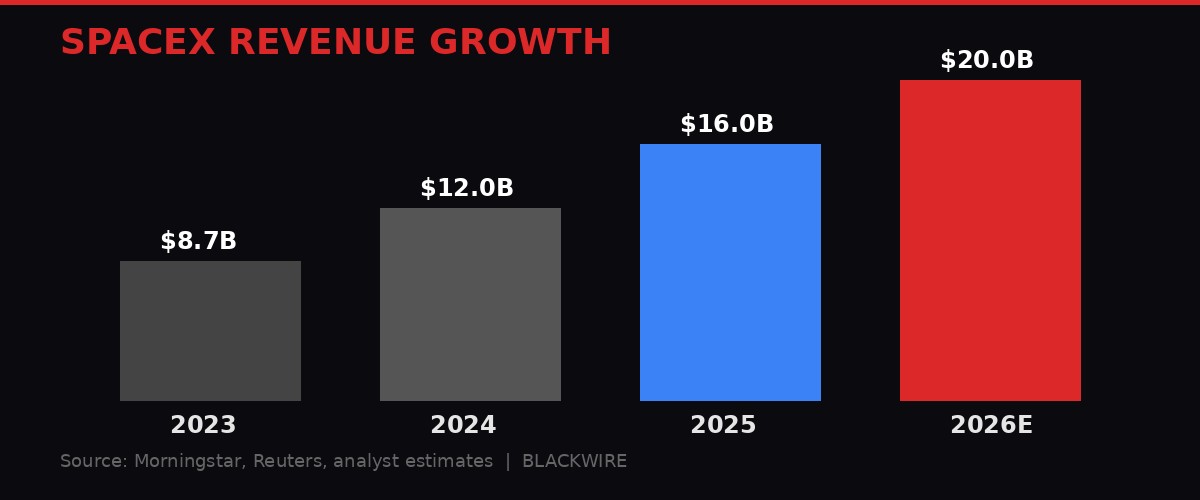

SpaceX is not a speculative pre-revenue startup going public on hype. The company generated approximately $16 billion in revenue and $7.5 billion in EBITDA during 2025, according to estimates from Morningstar. Reuters independently reported that SpaceX earned about $8 billion in profit on $15-16 billion in revenue, with Starlink contributing roughly 50-80% of total revenue depending on the accounting methodology.

Revenue is projected to reach $20 billion in 2026, according to analyst estimates compiled by CoinCentral and multiple financial outlets. That projection factors in continued Starlink subscriber growth, an accelerating launch cadence, and the first partial-year contributions from xAI following its February merger with SpaceX.

But the valuation math tells a different story than the revenue growth. At $1.75 trillion, SpaceX would be trading at roughly 110 times its 2025 revenue of $16 billion. Even against the optimistic 2026 projection of $20 billion, that is an 87x revenue multiple. For context, Tesla trades at roughly 15x revenue. Nvidia, the market's most celebrated growth story, trades at about 30x. Amazon trades at approximately 3.5x. SpaceX's asking price is in a league of its own.

The bull case hinges on three things: Starlink's subscriber trajectory and its potential to become the dominant global internet provider, the government contract pipeline that keeps growing with every new defense initiative, and the xAI merger which adds an AI infrastructure play to the mix. The bear case is simpler - even extraordinary companies can be priced too richly at their debut, and IPO-day buyers often suffer for years as reality catches up to the multiple.

Brett Schafer at The Motley Fool put it plainly in analysis published March 31: "Even if you think SpaceX is a promising business, the stock is likely to trade at a very steep valuation if its market cap reaches $1.75 trillion. That would give the stock an extreme valuation and likely mean poor forward returns over the next decade, even if the business experiences rapid growth." His advice: stay patient and keep it on the watchlist.

Starlink - The Cash Engine Powering the Machine

Starlink is the primary reason SpaceX can demand a $1.75 trillion valuation with a straight face. The satellite internet service, which operates on a constellation of approximately 10,000 low-Earth orbit satellites, has experienced subscriber growth that few telecom ventures in history can match. Wikipedia's latest data, sourcing SpaceX's own announcements, shows the trajectory: 1 million subscribers in December 2022, 4 million in September 2024, and 9 million by December 2025. Some recent reports suggest the subscriber count has already crossed 10 million as of early 2026.

Starlink generated an estimated $10-10.6 billion in revenue during 2025, according to analysis from RevenueMemo, up from $7.7-8.2 billion in 2024 and $4.2-4.4 billion in 2023. The growth rate is staggering - Starlink roughly doubled revenue in two years while maintaining margins that most satellite operators would consider impossible. SpaceX reportedly earned $8 billion or more in profit from Starlink alone in 2025, making it one of the most profitable satellite operations ever built.

The service has expanded well beyond residential internet. Starlink now provides connectivity to maritime vessels, commercial aircraft, government agencies, and military operations worldwide. Its customers include major satellite operators like EchoStar, Viasat, Intelsat, and Telesat, who ironically rely on SpaceX's Falcon 9 rockets to launch their own competing satellites. SpaceX controls both the launch vehicle and the dominant satellite internet service - a vertical integration play that would make John D. Rockefeller nod approvingly.

Future plans for Starlink include expansion to approximately 12,000 satellites in the near term, with a possible later extension to 34,400. In recent months, Musk has floated an even more ambitious concept: building a network of up to one million data center satellites in orbit, launched from facilities on the Moon. Whether that vision is engineering roadmap or science fiction remains debatable, but it speaks to the ambition that investors are being asked to price in.

Starlink constitutes approximately 65% of all active satellites currently in orbit. That market position is difficult to overstate. No competitor - not Amazon's Project Kuiper, not OneWeb, not any government-backed constellation - comes close to matching Starlink's scale, subscriber base, or launch cadence. The question for IPO investors is whether that dominance translates into a durable moat or whether regulatory backlash, spectrum conflicts, and orbital debris concerns eventually slow the machine.

The xAI Merger - How a $250 Billion AI Lab Got Bolted Onto a Rocket Company

In February 2026, SpaceX completed what may have been the most consequential corporate merger of the decade: the all-stock acquisition of xAI, Musk's artificial intelligence company. The deal valued SpaceX at approximately $1 trillion and xAI at $250 billion, creating a combined entity worth $1.25 trillion at the time of closing. The merger also brought X (formerly Twitter) under the SpaceX umbrella, since xAI had previously absorbed the social network.

The speed of the transaction raised eyebrows. Both companies are controlled by Musk and his inner circle, which meant the merger could proceed without the typical months of due diligence, shareholder negotiations, and regulatory review that characterize deals of this magnitude. Critics have noted that the valuation assigned to xAI - $250 billion for a company generating less than $1 billion in revenue - was aggressive by any standard. Supporters counter that xAI's Grok model, its growing compute infrastructure, and its access to X's data firehose justify the price tag as a bet on future value.

The merger created a conglomerate that spans rocketry, satellite internet, artificial intelligence, social media, and defense contracting. It is arguably the most vertically integrated technology company on Earth. SpaceX launches the satellites. Starlink provides the connectivity. xAI builds the models. X provides the data and distribution. Government contracts tie it all together with the most powerful customer on the planet.

But the merger also brought baggage. xAI carried approximately $17.5 billion in debt at the time of the acquisition, according to CoinCentral's reporting. That debt was accumulated through aggressive spending on data center construction and compute procurement as xAI raced to compete with OpenAI, Anthropic, and Google DeepMind. SpaceX has indicated that the xAI debt will be fully repaid before the IPO closes, which means a significant portion of the $75 billion raise may go toward cleaning up the balance sheet rather than funding new operations.

The merger also raises governance questions. Musk will emerge from the IPO as the first person in history to helm two separate trillion-dollar publicly traded companies simultaneously (SpaceX and Tesla). He already splits his time across more ventures than most CEOs manage in a lifetime. Investors buying SpaceX shares are making a bet not just on the business, but on one man's ability to maintain focus across an empire that includes electric vehicles, rockets, satellites, AI models, social media, brain-computer interfaces (Neuralink), and underground tunnels (The Boring Company). The question is whether that is a feature or a risk.

How SpaceX Stacks Up Against History's Biggest IPOs

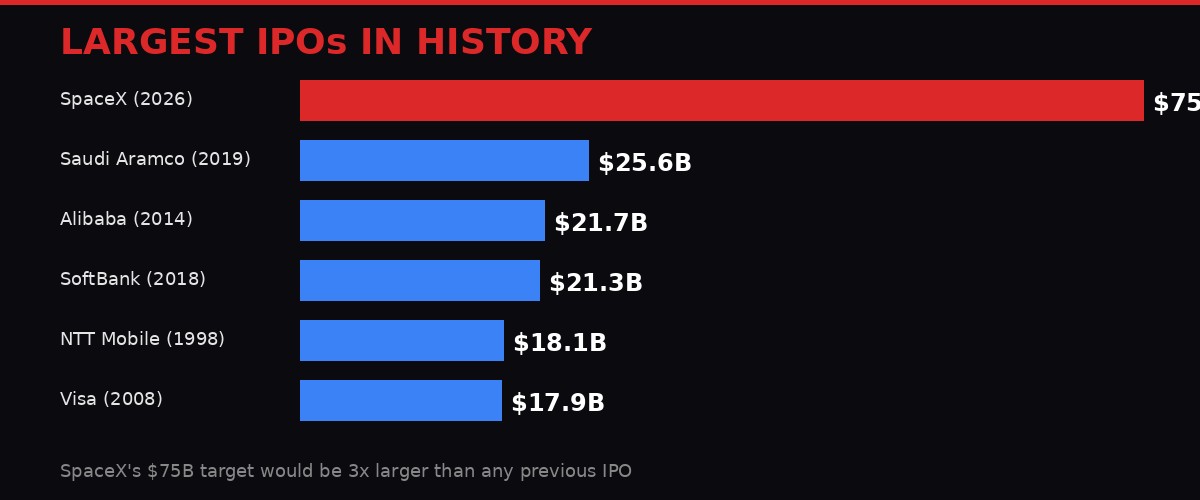

If SpaceX raises $75 billion, it would obliterate every previous IPO record by a factor that makes comparisons almost absurd. The current record holder is Saudi Aramco, which raised $25.6 billion when it listed in Riyadh in December 2019. Before that, Alibaba held the crown with $21.7 billion in 2014. SoftBank raised $21.3 billion in 2018. NTT Mobile raised $18.1 billion in Japan back in 1998. Visa raised $17.9 billion in 2008. SpaceX's target is roughly three times the entire Aramco raise.

The comparison breaks in SpaceX's favor on one dimension: investor appetite. Reena Aggarwal, a professor of finance at Georgetown and an IPO expert quoted by CNBC, noted that the demand dynamics for SpaceX are unlike anything the market has seen. "It's not like five other companies like this will go public in the next five years," she said. "Anyone who wants more exposure to Elon Musk - this is their opportunity to get in."

Musk has reportedly indicated that he wants to allocate up to 30% of IPO shares directly to retail investors. That would be roughly three times the Wall Street standard of 5-10% retail allocation. If the number holds, it means individual investors could have access to approximately $22.5 billion worth of SpaceX shares at the IPO price - an extraordinary opportunity, or an extraordinary risk, depending on where the stock goes after listing.

But the comparison also breaks against SpaceX. Saudi Aramco went public with a business generating over $300 billion in annual revenue and net income exceeding $100 billion. SpaceX has $16 billion in revenue and $8 billion in profit. Aramco's IPO valued the company at roughly 6x revenue. SpaceX is asking for 110x. The delta between those multiples tells you exactly how much of SpaceX's price is based on growth expectations rather than current fundamentals.

Aggarwal also flagged the timing risk. "You can have a great company, with great fundamentals and a lot of investor interest - and an IPO can still flop if the markets have turned south, if there's too much volatility in the market," she told CNBC. The Nasdaq's recent selloff, driven partly by the Iran conflict and partly by a federal antitrust verdict against Meta, has rattled tech investors. If geopolitical tensions escalate before June, SpaceX may need to reprice or delay.

The Valuation Leap - From $46 Billion to $1.75 Trillion in Six Years

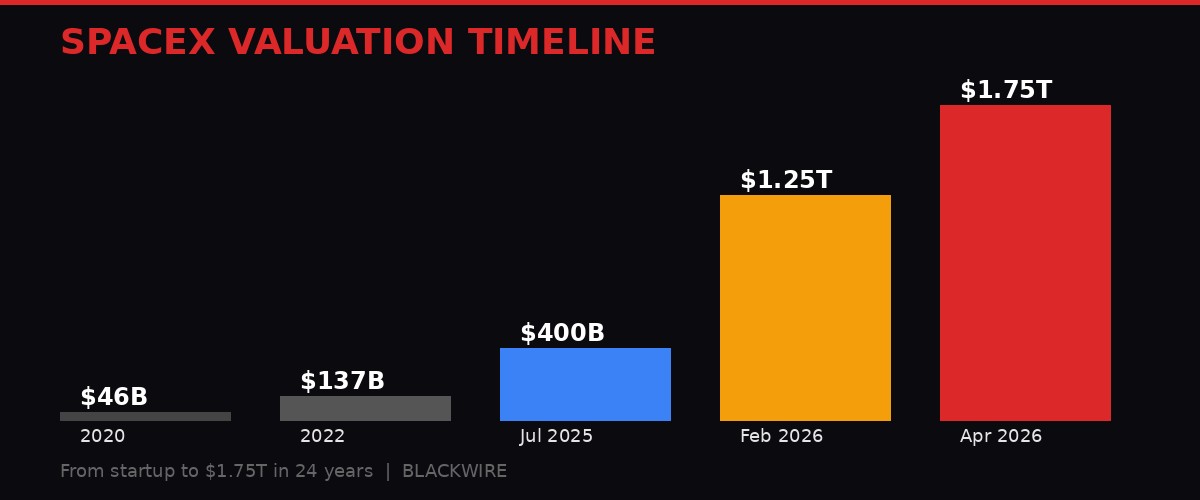

The velocity of SpaceX's valuation growth deserves its own analysis because it reveals something important about how private markets now operate. In 2020, SpaceX was valued at approximately $46 billion during a private funding round. By 2022, that number had climbed to $137 billion. In July 2025, SpaceX completed a private share sale that valued the company at $400 billion - already making it the most valuable private company in history.

Then came the xAI merger in February 2026, which instantly revalued the combined entity at $1.25 trillion. Now, less than two months later, SpaceX is asking public market investors to buy in at $1.75 trillion - a 40% markup from the merger valuation and a staggering 38x increase from its 2020 valuation.

That trajectory has no historical precedent among companies of this scale. The closest parallel might be Nvidia, which went from a market cap of roughly $300 billion in early 2023 to over $3 trillion by mid-2025, driven by the AI boom. But Nvidia was already public, with quarterly earnings reports providing investors a continuous reality check. SpaceX made its ascent entirely in private markets, where valuation discipline is notoriously looser and price discovery relies on a small number of sophisticated buyers rather than the collective judgment of millions of public market participants.

The jump from $1.25 trillion to $1.75 trillion - a $500 billion increase in eight weeks - was driven primarily by the SpaceX-xAI integration story. Analysts at US Reporter described the merger as "a fundamental shift in SpaceX's architecture - pivoting toward a vertically integrated aerospace-AI conglomerate." The argument is that SpaceX plus xAI is worth more than the sum of its parts because the companies share infrastructure (Starlink connectivity for AI training), customers (the U.S. government), and a founder who can direct resources across the portfolio without bureaucratic friction.

Whether that $500 billion markup survives contact with public market scrutiny is the central question of this IPO. Private investors setting valuations in closed-door negotiations operate under different incentive structures than public markets. When the S-1 drops and analysts at every major bank start building their own models, the number that matters will not be what Musk thinks SpaceX is worth. It will be what the market is willing to pay.

Government Contracts - $24.4 Billion and Counting

SpaceX's relationship with the U.S. government is simultaneously its greatest asset and a potential source of regulatory friction as it enters public markets. According to FedScout, which tracks federal spending, SpaceX has received over $24.4 billion from its work with the federal government since 2008. That figure encompasses contracts from NASA, the Air Force, the Space Force, the National Reconnaissance Office (NRO), and the Space Development Agency (SDA), among other agencies.

Fed-Spend, another federal contract tracking service, puts cumulative SpaceX government contract value at approximately $22 billion, with the difference likely attributable to methodology and timing of contract modifications. Either way, the U.S. government is SpaceX's single largest customer by a wide margin. NASA alone has awarded SpaceX the Artemis human lunar lander contract - the vehicle designed to return American astronauts to the Moon - along with dozens of cargo and crew missions to the International Space Station.

On the defense side, SpaceX operates Starshield, a classified satellite constellation purpose-built for military and intelligence applications. Details are sparse by design, but the program represents SpaceX's deepest penetration into the national security apparatus. The company also holds contracts with the Space Development Agency for transport and tracking layer satellites, providing missile warning and communications capabilities that the Pentagon considers critical infrastructure.

In 2025, SpaceX conducted 165 orbital flights, an unprecedented cadence that no other launch provider on Earth can match. Those launches delivered payloads for commercial customers, government agencies, and SpaceX's own Starlink constellation. The company also continued test flights of its Starship Super Heavy vehicle, the fully reusable heavy-lift rocket that is central to NASA's lunar ambitions and SpaceX's long-term plans for Mars.

The government revenue stream provides stability and predictability that pure commercial businesses lack. Government contracts are typically multi-year, cost-plus or fixed-price arrangements that provide revenue visibility years in advance. But that dependency also creates vulnerability. SpaceX's heavy reliance on government spending means that changes in administration priorities, defense budgets, or regulatory posture could materially affect the business. National security reviews and export controls may also influence the IPO process itself, particularly given the classified nature of some SpaceX programs and the geopolitical sensitivity of Starlink's global operations.

Market Conditions - Can a $75 Billion Raise Survive the Current Volatility?

The timing of SpaceX's filing is bold, bordering on audacious. The company is filing during one of the most turbulent periods for equity markets in recent memory. The U.S.-Iran war, which began earlier this year, continues to weigh on global markets. Oil prices remain elevated. The Nasdaq just posted its steepest weekly decline in nearly a year, driven partly by geopolitical uncertainty and partly by a landmark antitrust verdict against Meta. Inflation expectations are ticking higher. Consumer confidence is shaky.

And yet, SpaceX is pressing forward. The calculus appears to be that the company's brand, its monopolistic market position in launch services, and the sheer magnetism of the Musk brand will generate enough demand to overcome macro headwinds. Georgetown's Aggarwal captured the duality: great company, great fundamentals, massive investor interest - but IPOs can still flop in hostile markets.

Reuters reported that Wall Street is betting 2026 will be a breakout year for U.S. IPOs after years of drought. Rising interest rates, inflation concerns, and geopolitical tensions kept issuers waiting through much of 2023, 2024, and 2025, even as the pipeline of companies ready to go public grew larger. The industry is hoping SpaceX will be the dam-breaker - the deal that proves the market can absorb mega-offerings again and opens the floodgates for other long-awaited listings.

SpaceX is not the only massive tech company eyeing a 2026 listing. Reports suggest that both OpenAI and Anthropic are exploring public market options, though neither has filed. If SpaceX succeeds, it could pave the way for a summer and fall packed with AI-adjacent IPOs. If it stumbles, the entire pipeline may freeze again.

One potential buffer against market volatility is Musk's stated plan to allocate 30% of shares to retail investors. By directing a significant portion of the offering away from institutional investors and toward individual buyers, SpaceX may be able to tap into a reservoir of demand that is less sensitive to short-term market conditions. Retail investors, particularly those motivated by brand loyalty rather than fundamental analysis, tend to buy regardless of macro backdrop. Whether that is smart capital allocation or a recipe for post-IPO instability is a question the market will answer in real time.

What Comes Next - Timeline, Risks, and the Road to June

The confidential filing is step one. Here is what happens next.

The SEC will review SpaceX's draft registration statement and provide feedback, likely requesting additional disclosures, clarifications, or revisions. This back-and-forth typically takes several weeks. SpaceX must make its filing public at least 15 days before beginning the IPO roadshow, which means investors will likely see the S-1 sometime in late May.

Musk has reportedly scheduled an investor briefing for April to begin laying the groundwork with institutional buyers. Details are expected to cover valuation rationale, financial projections, the xAI integration, and SpaceX's forward strategy. This briefing will be critical for setting expectations before the formal roadshow begins.

The roadshow itself will likely span two to three weeks, with SpaceX's management team meeting with institutional investors across the U.S., Europe, Asia, and the Middle East. Given the 21-bank syndicate's geographic diversity, the roadshow will be one of the most logistically complex in IPO history.

Pricing is expected in early to mid-June, with shares beginning to trade shortly after. The listing venue has not been confirmed, but the Nasdaq is considered the likely choice given its dominance in technology listings. Some observers have noted that Nasdaq recently changed its rules in ways that could accelerate the onboarding process for mega-listings like SpaceX, potentially allowing index inclusion within 15 days of listing.

The risks between now and June are considerable. The Iran war could escalate, crashing equity markets. The SEC could flag issues with SpaceX's financials or governance structure. The xAI debt repayment timeline could slip. Musk could say something on X that spooks investors. Congressional scrutiny of Musk's government relationships - particularly his role in DOGE and his companies' $24 billion in federal contracts - could generate headlines that complicate the offering.

And then there is the fundamental question that hangs over every mega-IPO: can the market actually absorb $75 billion in new equity issuance? That amount is larger than the GDP of many countries. It requires institutional investors, sovereign wealth funds, pension funds, and millions of retail investors to simultaneously conclude that SpaceX at $1.75 trillion is a reasonable bet. Even in the best market conditions, that is a tall order. In conditions like these, it is an act of faith.

SpaceX has defied conventional expectations at every stage of its existence. It survived near-bankruptcy in 2008. It landed a rocket booster on a barge when the aerospace establishment said it was impossible. It built a satellite internet service with 10 million subscribers in less than five years. It merged with an AI company and a social network in a single transaction. Now it is attempting something that has never been done before: a $75 billion IPO in the middle of a war, during a volatile market, for a company that many investors have never had a chance to own.

The filing is in. The banks are assembled. The codename is Project Apex. Whether the reality matches the name will be determined in the next 60 days.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on TelegramSources: Bloomberg, CNBC, Reuters, TechCrunch, Morningstar, FedScout, Fed-Spend, The Motley Fool, CoinCentral, Seeking Alpha, RevenueMemo, US Reporter, Wikipedia/Starlink