Bitcoin at $66,655 as Q1 2026 closes - down 47% from its $126,000 all-time high set in October 2025. (Unsplash)

The last trading day of Q1 2026 delivered something the crypto market hasn't seen in years: simultaneous capitulation and construction. On the same Monday that data showed nearly half of all circulating bitcoin is underwater, Jack Dorsey's Square flipped the switch on automatic bitcoin payments for millions of American businesses. Miners posted their first quarterly hashrate decline in six years. Lido DAO proposed spending $20 million of its treasury to buy its own collapsed token. And Bernstein told clients to back up the truck.

This is not a normal correction. This is a structural divergence - the moment where the builders and the holders diverge so dramatically that the market stops being one thing and becomes two. One side believes bitcoin's payment utility is about to go mainstream. The other side is selling at losses not seen since 2022. Both are acting on conviction. Both can't be right.

The numbers are brutal. Bitcoin at $66,655. Down 47% from the $126,000 peak hit just five months ago. Total crypto market cap shed roughly $2 trillion since October 2025. Stablecoin flows flipped negative. ETF inflows reversed. And the Bitcoin Impact Index - a composite stress gauge measuring onchain behavior, ETF activity, derivatives, and liquidity - just hit 57.4, its steepest weekly climb since January.

Every cycle has a moment where the narrative splits. This is Q1 2026's.

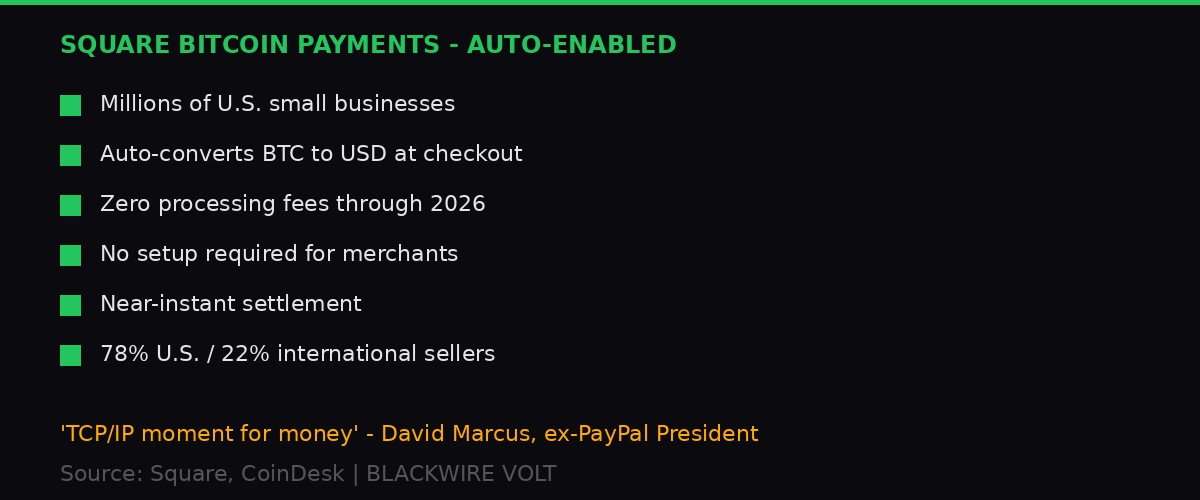

I. Square Goes Nuclear: Bitcoin Payments Auto-Enabled for Millions

Square's bitcoin payment rollout: zero fees, instant conversion, no merchant setup required. (BLACKWIRE/VOLT)

Jack Dorsey didn't ask permission. On Monday, Square began automatically enabling bitcoin payments for millions of eligible U.S. small businesses. Not an opt-in. Not a beta. The feature is live, converting bitcoin to dollars at checkout with zero processing fees through the end of 2026. Merchants don't need to touch a setting. The system handles conversion, settlement, and accounting.

"Automatically enabled bitcoin payments are rolling out to eligible U.S. Square sellers," the company wrote on X. "Start accepting bitcoin that instantly converts to cash at checkout, with no additional setup."

The mechanics are deliberate. Bitcoin enters the system. Dollars come out. The merchant never holds crypto, never sees volatility, never deals with custody. For the buyer, it's a bitcoin payment. For the seller, it's just money. This is the abstraction layer the industry has talked about for a decade, and Square just shipped it to millions of businesses overnight.

Miles Suter, Block's head of bitcoin product, framed it as a beginning: "We're making it easier for millions of businesses to accept bitcoin. This is how bitcoin as everyday money begins." Dorsey confirmed with a single word on X: "Today."

The response from the payments industry was immediate. David Marcus, the former PayPal president who now runs Lightspark, called the rollout a potential "TCP/IP moment" for money - comparing it to the protocol standardization that made the internet work across incompatible networks. "Enabling Bitcoin payments at scale could mirror how TCP/IP became the foundational protocol of the internet," Marcus said.

That comparison carries weight. TCP/IP didn't win because it was the best protocol. It won because it was embedded everywhere before most people understood what it did. Square's play follows the same logic: don't convince merchants that bitcoin matters. Just make it work in their existing system and let volume do the convincing.

Square User Base

78% U.S. / 22% International

Millions of eligible sellers now auto-enabled for BTC payments with zero fees through 2026

The timing is aggressive. Dorsey, a lifelong bitcoin purist who has publicly resisted stablecoins, is making this move while his competitor PayPal expands PYUSD into 70 global markets. Both are betting on crypto payments. But they're betting on different versions. PayPal says the future is dollar-pegged stablecoins. Dorsey says it's bitcoin itself, abstracted down to invisibility.

This is the first time a major payments company has defaulted merchants into bitcoin acceptance at scale. Every previous crypto payment integration required merchant activation - an opt-in that most never bothered with. Square eliminated the friction entirely. If you're a Square seller in the U.S., you already accept bitcoin. You just might not know it yet.

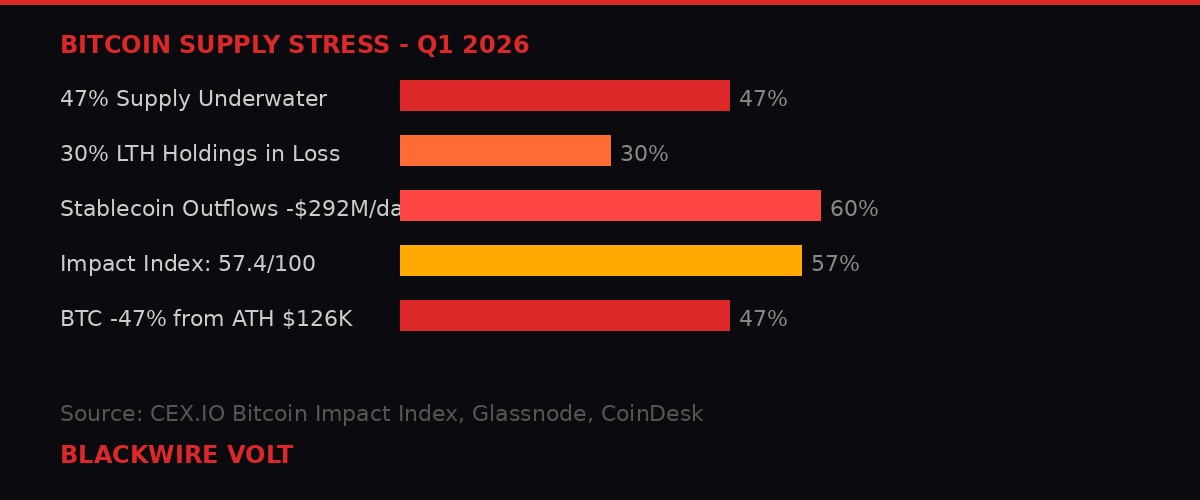

II. 47% Underwater: The Supply Stress Nobody Saw Coming

Bitcoin's supply stress metrics hit levels last seen during the worst stretches of the 2022 bear market. (BLACKWIRE/VOLT)

While Square builds the rails for bitcoin's commercial future, nearly half the existing supply is trading at a loss. The numbers from CEX.IO's Bitcoin Impact Index are hard to argue with: 47% of all circulating bitcoin is currently held below its purchase price. That's not a dip. That's structural pain.

The Impact Index itself surged 13 points in a single week to 57.4, placing it firmly in the "high impact" zone - a level that has historically preceded double-digit price drops. The last time the index moved this fast was January 2026. Before that, similar readings appeared in mid-2022 (before the 25% Luna-triggered collapse) and mid-2018 (before bitcoin fell from $6,000 to $3,200).

Long-term holders - wallets that held bitcoin for more than six months, the so-called diamond hands - are cracking. Over 4.6 million BTC from these addresses is now underwater, roughly 30% of their total holdings. A week ago, when bitcoin was still above $70,000, most of these wallets were in profit. The speed of the flip stunned even seasoned onchain analysts.

"This kind of divergence between price action and on-chain conviction has historically been a warning sign. Similar moves occurred in mid-2018 and mid-2022 before price drops by over 25%." - CEX.IO Research

Realized losses from long-term holders last week were the worst since 2023. These aren't speculators cutting positions. These are holders who survived the 2022 bear market, held through the 2024 halving, and rode the rally to $126,000 - only to sell at a loss on the way back down. That's capitulation from the most resilient cohort in the market.

Capital flows reinforce the story. Daily stablecoin net flows, which had averaged $250 million in inflows for much of Q1, flipped to outflows of $292 million per day. That's a $542 million daily swing from positive to negative. ETFs shifted from accumulation to selling. Miners followed suit. The liquidity that supported the market through February has evaporated.

One signal remains intact: holders are not rushing to deposit bitcoin on exchanges. In past capitulations - November 2022, June 2022, March 2020 - exchange deposits spiked as holders prepared to dump. That hasn't happened yet. It means the market is stressed, not panicked. Stressed markets can recover. Panicked markets crash.

Bitcoin Impact Index

57.4 / 100

+13 points in one week. High impact zone. Historically precedes 25%+ drawdowns.

The question isn't whether bitcoin is in a bear market. The question is whether this is the bottom of it or the middle. With $66,655 as the current price and production costs near $90,000 for most miners, the math doesn't resolve in anyone's favor except the patient.

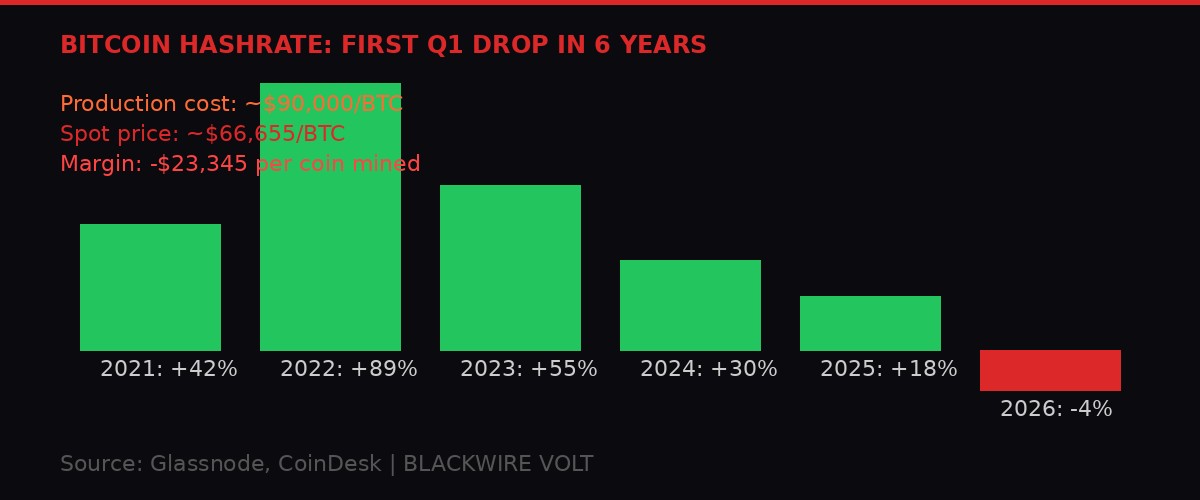

III. The Hashrate Collapse: Miners Choose AI Over Bitcoin

Bitcoin's hashrate fell in Q1 for the first time since 2020. Miners are pivoting capital to AI infrastructure. (BLACKWIRE/VOLT)

For the first time in six years, bitcoin's network hashrate declined during the first quarter. The metric - measuring total computational power securing the blockchain - is down roughly 4% year-to-date, hovering around 1 zettahash per second. That breaks a streak of five consecutive years of double-digit Q1 growth, including an 89% surge in 2022 and 55% in 2023.

The reason is economic. At current difficulty levels, it costs approximately $90,000 to mine a single bitcoin. Spot price: $66,655. That's a loss of roughly $23,345 per coin produced. Miners are paying more in electricity, hardware depreciation, and overhead than the asset they're creating is worth. Every block mined at current prices is a bet that the price recovers before the balance sheet doesn't.

The response has been a mass pivot to artificial intelligence infrastructure. Publicly listed miners - who account for over 40% of global hashrate - are redirecting capital from ASIC rigs to GPU clusters. The AI compute market offers higher margins, predictable contracts, and growing demand. Bitcoin mining offers negative margins, halving-driven revenue compression, and a price chart that just fell 47% in five months.

This transition is being funded in two ways: debt issuance and bitcoin sales. Miners are borrowing against their existing infrastructure to build AI data centers while simultaneously selling their mined bitcoin to cover operating costs. The double hit - less hashrate deployed plus more BTC sold - creates a negative feedback loop that suppresses both network security metrics and price.

The irony is thick. A year ago, the narrative was that bitcoin miners were the backbone of a decentralized financial revolution. Now they're becoming AI companies that happen to still mine some bitcoin on the side. Marathon Digital, CleanSpark, Riot Platforms - the biggest names in mining are all mid-pivot, allocating marginal capital to GPU computing rather than ASIC expansion.

There's a silver lining, buried in the data. If U.S. public miners reduce their share of global hashrate, the network becomes more geographically distributed. The concentration of mining power in a handful of Nasdaq-listed companies was itself a centralization risk. A decline in their dominance could paradoxically make bitcoin more decentralized - more aligned with its founding principles even as its economics deteriorate.

But that's a long-term thesis. In the short term, the hashrate drop signals an industry in retreat. When the people securing the network are losing money on every block, something has to give. Either price recovers, difficulty adjusts downward, or more miners exit. Q2 2026 will answer which one.

IV. Lido's $20 Million Desperation Buyback: When DeFi Has to Buy Itself

Lido DAO's proposed buyback exposes the liquidity crisis in DeFi governance tokens. (Unsplash)

Lido DAO, the protocol that controls 23% of all staked ether on Ethereum, just proposed spending $20 million of its treasury to buy its own governance token. That sentence should alarm you. The largest liquid staking protocol in existence is so concerned about LDO's price that it's willing to deploy 10,000 stETH - roughly $20 million at current ETH prices - to prop up a token that's fallen 95% from its all-time high.

LDO hit an all-time low of $0.27 on March 7 and currently trades near $0.30, with a market capitalization of roughly $258 million. Its 2021 peak: $7.30. The proposed buyback could absorb approximately 65 million tokens - about 8% of circulating supply - at current prices.

But here's the problem that makes this story genuinely absurd: Lido can't even execute the buyback on its own network. Onchain LDO liquidity sits at roughly $90,000 of depth at plus-or-minus 2%. A single 1,000 stETH batch - one-tenth of the proposed total - would blow through available liquidity multiple times over. Ethereum's largest DeFi staking protocol has to go to Binance, OKX, Bybit, Gate, and Bitget to buy its own token at scale.

"This is not a routine fluctuation. It represents one of the most significant dislocations between LDO's market price and its underlying protocol fundamentals in the token's history." - Lido Ecosystem Operations

The DAO's argument centers on a disconnect between token price and protocol performance. The LDO-to-ETH ratio sits at 0.00016 - a 70% discount to the level that held for most of the past two years. Meanwhile, net protocol rewards have dropped only 20%, costs improved 13% year-over-year, and the effective take rate rose to 6.11% from 5%. By any fundamental metric, Lido is doing fine. Its token says otherwise.

Execution would proceed in 1,000 stETH batches, each requiring a separate Easy Track governance motion with a three-day objection period. The Growth Committee retains timing discretion to avoid signaling exact moves to front-runners. Slippage is capped at 3% below reference price. Market-maker partners may be engaged through the Lido Ecosystem Foundation.

The deeper question Lido's buyback surfaces extends far beyond one protocol. LDO's 95% drawdown is extreme, but it's not an outlier in DeFi governance tokens as a category. Uniswap's UNI, Compound's COMP, Maker's MKR - nearly every governance token that launched in the 2020-2021 DeFi summer has suffered similar fates. The market has collectively repriced what a governance token is worth when it controls a fee switch but distributes nothing to holders.

Lido's answer is to treat the dislocation as a buying opportunity. But a protocol buying its own token with its own treasury is not the same as external demand. It's financial engineering - a buyback that reduces float without creating new holders. If the market doesn't believe governance tokens deserve fundamental valuations, a $20 million buyback changes the supply math but not the sentiment math.

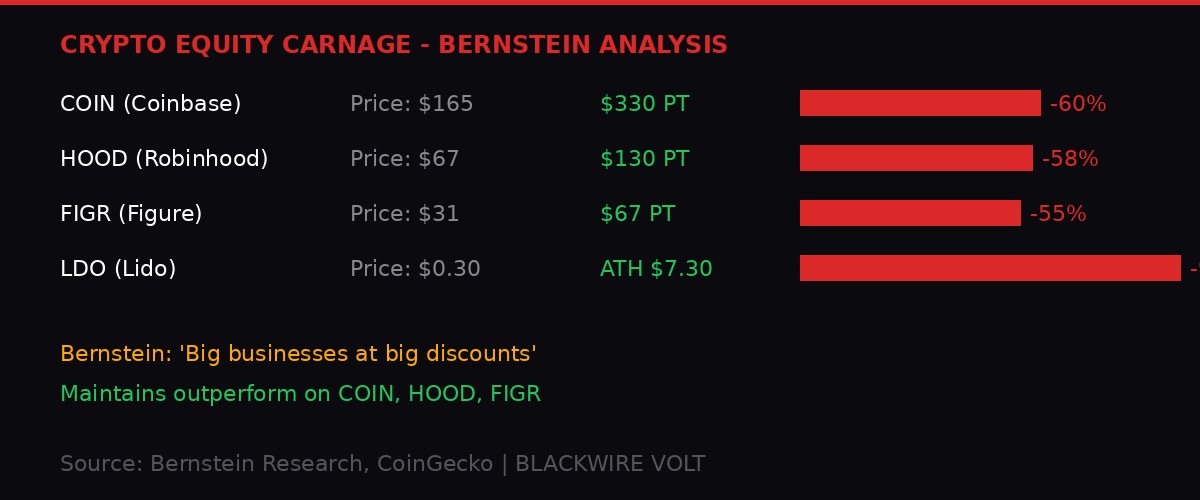

V. Bernstein Calls Bottom: 'Big Businesses at Big Discounts'

Crypto-linked equities have fallen 55-95% from 2025 highs. Bernstein sees a floor forming. (BLACKWIRE/VOLT)

Against this backdrop of capitulation, one of Wall Street's most watched brokerages is telling clients to buy. Bernstein's crypto equity team, led by Gautam Chhugani, published a report Monday calling the 60% crash in crypto stocks "big businesses at big discounts" and maintaining outperform ratings on Coinbase, Robinhood, and Figure.

The numbers are stark. Since peaking in October 2025, crypto equities have been destroyed. Coinbase trades at $165.50 - Bernstein's new target is $330 (cut from $440). Robinhood sits at $67.10 against a $130 target (cut from $160). Figure trades at $31.14 versus a $67 target (cut from $72). In every case, the broker sees prices roughly doubling from current levels but had to slash prior targets to acknowledge the severity of the drawdown.

"The combination of geopolitics and temporary crypto weak sentiment is offering big discounts on crypto stocks," Chhugani's team wrote. The analysts expect near-term weakness to persist through Q1 earnings but see current levels as an entry point into companies with exposure to what they describe as large and growing markets: stablecoins, tokenization, prediction markets, and derivatives.

This follows Bernstein's call last week that bitcoin has "likely found its bottom" - a thesis that pairs with their reiterated $150,000 year-end price target. If they're right, bitcoin needs to rally 125% from current levels by December. That's not impossible in crypto - it rallied 160% in Q4 2023 alone - but it requires the macro backdrop to cooperate in ways it currently isn't.

The bull case hinges on several assumptions: the Fed pivots before year-end, the Iran conflict de-escalates enough to drop oil prices, stablecoin adoption continues accelerating, and institutional demand returns after Q1 earnings clear the air. None of those are guaranteed. Some of them are actively moving in the wrong direction.

Bernstein Year-End Target

BTC $150,000

Current price: $66,655. Required rally: +125%. Maintaining outperform on COIN, HOOD, FIGR.

What makes Bernstein's call interesting is not the price targets themselves but the reasoning behind them. These aren't meme coin promoters or influencer shills. This is a research desk that covers institutional capital allocation telling its clients - pension funds, endowments, family offices - that crypto equity valuations have overshot to the downside. When Bernstein talks, the money that moves markets listens. Whether it acts is another question.

VI. BitMine's Lonely ETH Accumulation: The Last Corporate Buyer Standing

BitMine is the only major corporate buyer still accumulating crypto at scale. (BLACKWIRE/VOLT)

While the rest of the corporate crypto world retreats, one company is accelerating. BitMine Immersion Technologies bought 71,179 ETH last week - its largest weekly purchase of 2026 - bringing total holdings to 4.73 million ETH, approximately 3.92% of ether's entire circulating supply. That purchase, worth roughly $143 million at current prices, makes BitMine the sole remaining large-scale corporate crypto buyer in the market.

The significance is sharpened by what happened across the aisle. Strategy (formerly MicroStrategy), the Michael Saylor-led company that became synonymous with corporate bitcoin accumulation, broke its 13-week buying streak. After purchasing bitcoin consistently since early January, the company paused last week. No explanation was given. The silence spoke volumes.

BitMine Chairman Tom Lee - also CIO of Fundstrat, one of crypto's most-cited research firms - said the firm views the current market as "the final phase of a downturn." The company has increased its buying pace for four consecutive weeks, stepping up from a prior average of 45,000 to 50,000 ETH per week. Total crypto and cash holdings now stand at $10.7 billion.

There's something both admirable and terrifying about being the last buyer. When Strategy was accumulating bitcoin alongside dozens of other corporate treasuries, the buying felt like institutional consensus. When one company is buying while everyone else is either pausing or selling, it starts to look like either extreme conviction or the loneliest trade in crypto.

BitMine's ether thesis differs from Strategy's bitcoin playbook in one critical way: concentration. Holding 3.92% of a major blockchain's circulating supply creates both upside leverage and systemic risk. If ether recovers, BitMine's position explodes in value. If the decline deepens, their holdings become both an asset and a liability - a position too large to exit without moving the market against itself.

The rest of the digital asset treasury space has gone quiet. Companies that were announcing weekly purchases in January are issuing no-comment statements in March. The corporate crypto accumulation wave that defined 2024 and early 2025 has effectively paused. BitMine is either the smartest money in the room or the last one to leave the party. Q2 will tell.

VII. The Aave v4 Launch: DeFi Builds While the Market Burns

Aave v4 goes live on Ethereum after two years of development, targeting real-world credit markets. (Unsplash)

The builders aren't stopping. On the same day that half of bitcoin's supply went underwater, Aave - one of the largest decentralized lending platforms - launched its long-awaited v4 upgrade on Ethereum. The release has been in development for roughly two years and represents a fundamental architectural shift: instead of lumping all lending markets together, v4 allows different types of lending to operate separately while sharing the same liquidity pool.

The practical implications are significant. Aave v4 can now support more than just crypto-to-crypto lending. The new architecture enables institutional borrowing, real-world asset markets, and structured credit products - all running on decentralized infrastructure. Stani Kulechov, Aave Labs founder, framed it as the protocol's expansion beyond crypto's borders.

"DeFi is stronger than ever. A lot of these opportunities will come from value outside of DeFi." - Stani Kulechov, Aave Labs

The upgrade also introduces capital efficiency improvements. Idle funds in the protocol - what Kulechov called "the float" - can now be reinvested rather than sitting dormant. In a market where every basis point of yield matters, that's a meaningful competitive advantage over both legacy DeFi protocols and traditional lending platforms.

Aave v4 launched with conservative settings and a limited market set. Full functionality will roll out through governance decisions over the coming weeks. But the signal is clear: while traders panic-sell and governance tokens crater, the protocol layer is shipping upgrades that position DeFi for its next phase - one that looks less like crypto trading infrastructure and more like a parallel financial system.

The v4 launch also arrives amid ongoing governance tensions within Aave itself. Disputes over interface fees, contributor compensation, and revenue distribution to the DAO have created friction. The "Aave Will Win" proposal from February - which would send 100% of product revenue to the DAO - remains under discussion. Building protocol infrastructure while managing decentralized politics is one of DeFi's least-discussed challenges, and one of its most consequential.

VIII. The Central Bank Squeeze: Fed and BOJ Rate Hike Bets Collide

Rate hike expectations are building across both the Federal Reserve and the Bank of Japan. (Unsplash)

Behind every number in this article sits a macro backdrop that's getting worse, not better. Traders are now pricing a 69% probability that the Bank of Japan will raise rates at its April 28 meeting. Options on U.S. interest rates show expectations for the Fed to tighten in coming weeks as well. If both happen, crypto faces a tightening vise that makes Q1's pain look like a warmup.

The BOJ dynamic is particularly dangerous. For decades, Japan's ultra-low interest rates fueled the carry trade - investors borrowing cheap yen to invest in higher-yielding assets worldwide. That trade greased rallies in everything from tech stocks to bitcoin. A BOJ rate hike would threaten to reverse those flows, pulling capital out of risk assets and back into yen-denominated holdings.

Japan has already moved its rate from -0.1% to 0.75% over the past two years while winding down its massive asset purchase program. But rates remain far below the U.S. level of 3.5%, leaving significant room for further tightening. The BOJ's policy meeting summary released Monday included one member calling for a bigger rate hike in response to the Middle East conflict and its inflationary impact on Japan.

The yen has weakened to approximately 160 per dollar - its weakest since mid-2024 and a 54% depreciation since 2021. Japan is caught in a trap: hike rates to strengthen the yen and risk detonating a sovereign debt crisis (debt-to-GDP: 240%), or keep rates low and watch imported inflation erode living standards while the currency collapses.

For crypto, the implications are direct. A simultaneous Fed-BOJ tightening would drain liquidity from global risk markets. The carry trade unwind of July 2024 - when the BOJ raised rates and the yen surged - temporarily crashed bitcoin by 15% in three days. A larger version of that event, with the Fed also tightening, could be the catalyst that turns a correction into a rout.

The oil factor compounds everything. Iran war-driven crude prices at $115 per barrel feed inflation in Japan, Europe, and emerging markets, pressuring central banks to raise rates further. Higher rates crush risk assets. Lower risk appetite drains crypto. The feedback loop is already in motion. Q2 opens with both the world's largest and third-largest economies potentially hiking into a wartime energy shock.

IX. The FTX Payout: $2.2 Billion Returns to Market Tomorrow

FTX creditors receive $2.2 billion in distributions starting March 31. (Unsplash)

Add one more variable to Q2's opening hand. FTX's bankruptcy estate begins distributing roughly $2.2 billion to creditors on March 31 - the day after this article publishes. The payout covers claims from the exchange's November 2022 collapse, when Sam Bankman-Fried's empire imploded and took $8 billion in customer funds with it.

The market impact is debatable. Bulls argue that creditors who waited 3.5 years for their money are unlikely to immediately sell. Bears note that the distributions are in cash, not crypto, so the selling already happened when the estate liquidated its holdings over the past year. The middle ground: $2.2 billion entering the bank accounts of people who lost money in crypto is not obviously bullish for crypto prices.

The FTX payout also carries psychological weight. It's a reminder that the last time crypto looked this stressed - late 2022, with bitcoin in the $16,000s - the catalyst was an exchange implosion. The current stress comes from different sources (macro tightening, war, energy prices), but the feeling is familiar to anyone who lived through the FTX collapse: the market is breaking, nobody's sure where the bottom is, and institutional confidence is paper-thin.

Whether the FTX distribution becomes a market event or a footnote depends on what happens in the days that follow. If bitcoin holds the $65,000-$67,000 range through early April, it becomes a non-event. If the range breaks, the payout narrative will be weaponized by bears regardless of whether the money actually touches crypto markets.

X. Q2 Outlook: The Fork in the Road

Q2 2026 opens with the crypto market facing its most consequential quarter since the 2022 collapse. (Unsplash)

Q1 2026 ends with the crypto market in a state of profound contradiction. Square just embedded bitcoin into millions of point-of-sale systems. Aave shipped its biggest upgrade in two years. Bernstein says the bottom is in. BitMine keeps buying. Hoskinson launched a $200 million privacy blockchain. The builders are building.

But 47% of bitcoin is underwater. Miners are losing $23,000 per coin produced. Lido can't buy its own token on its own network. Stablecoin flows flipped negative. The Fed might hike. The BOJ might hike. Oil is at $115. And the Bitcoin Impact Index just flashed levels that preceded every major crash of the past decade.

These two realities can coexist temporarily. They can't coexist permanently. Either the builders are right that adoption and infrastructure will pull the market forward regardless of macro conditions, or the macro is right that liquidity is king and no amount of protocol upgrades matter when central banks are tightening into a war.

The historical analog that fits most closely is Q2 2019. Bitcoin had rallied from $3,200 to $14,000, then fell to $7,000 while PayPal, Fidelity, and Facebook announced crypto initiatives. The builders built through the pain. The price didn't recover until the Fed reversed course. Adoption without liquidity is a thesis, not a trade.

Q2 2026 will answer the question Q1 asked: does crypto's payment infrastructure story generate enough real demand to offset the macro headwinds? Square's millions of merchants are the test case. If bitcoin payment volume through Square grows meaningfully, the adoption thesis gets data behind it. If it flatlines, the builders were early again - right about the direction, wrong about the timing.

For traders, the levels matter. $65,000 on bitcoin is the support that held through March. Below that sits $58,000 - the 2024 halving rally launch pad. Below that is $52,000, where Bernstein's bottom thesis starts looking wrong. Above $72,000, short-term holders flip profitable and selling pressure eases.

The market doesn't care about narratives. It cares about flows. And right now, the flows say: stressed but not broken. The builders say: we don't care. Q2 starts tomorrow. Choose your side.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram