The Invisible $30 Billion: How Stablecoin Cards Are Replacing Cash Across Southeast Asia

StraitsX's 40x volume surge, Visa's 90% dominance, RedotPay's quiet empire, and the U.S. regulation that could kill yield and supercharge payments - all at once.

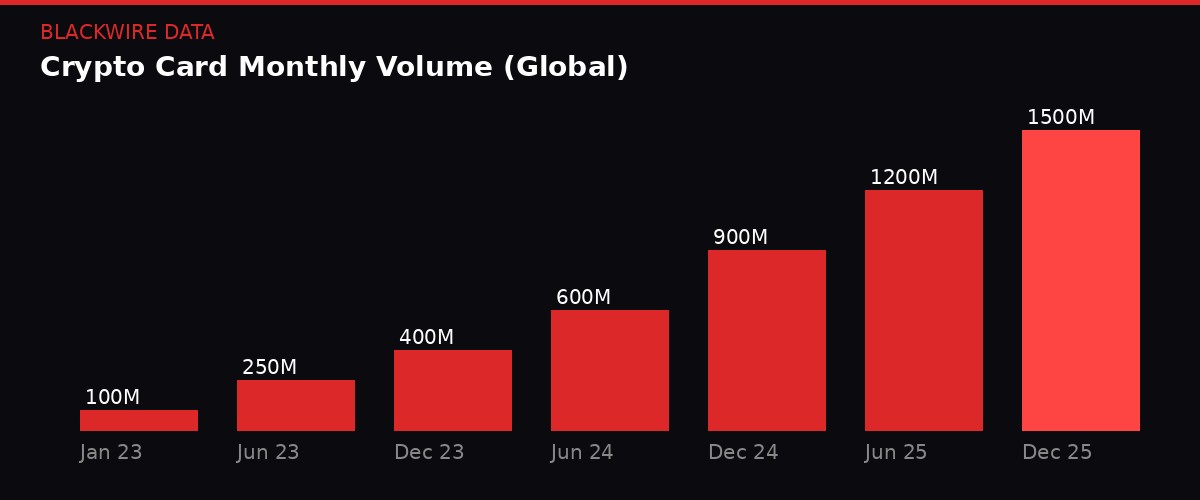

Global crypto card monthly volumes surged from $100M to $1.5B between 2023 and 2025. Source: Artemis Analytics

A tourist from Bangkok taps their phone at a hawker stall in Singapore. The transaction clears in under two seconds. Thai baht leaves the wallet. Singapore dollars hit the merchant. Nobody sees the stablecoin that bridged the gap.

That invisible layer - the one humming beneath $30 billion in cumulative transactions - is the story of 2026's most underrated financial revolution. While bitcoin traders argue about Bitfinex longs and the Fed's next move, the real action is happening at checkout counters across Southeast Asia, where stablecoin-powered debit cards are quietly eating traditional payment rails for breakfast.

The numbers are not subtle. StraitsX, the Singapore-based infrastructure company behind stablecoins XSGD and XUSD, just reported a 40x surge in card transaction volume between Q4 2024 and Q4 2025. Card issuance grew 83x in the same period. Their partner RedotPay processed $2.95 billion in card volume last year - more than four times the combined volume of its 13 closest competitors. And Visa, the legacy payments giant, now captures over 90% of all on-chain card spending.

These are not beta tests. This is replacement infrastructure.

The StraitsX Machine: From Zero to $30 Billion

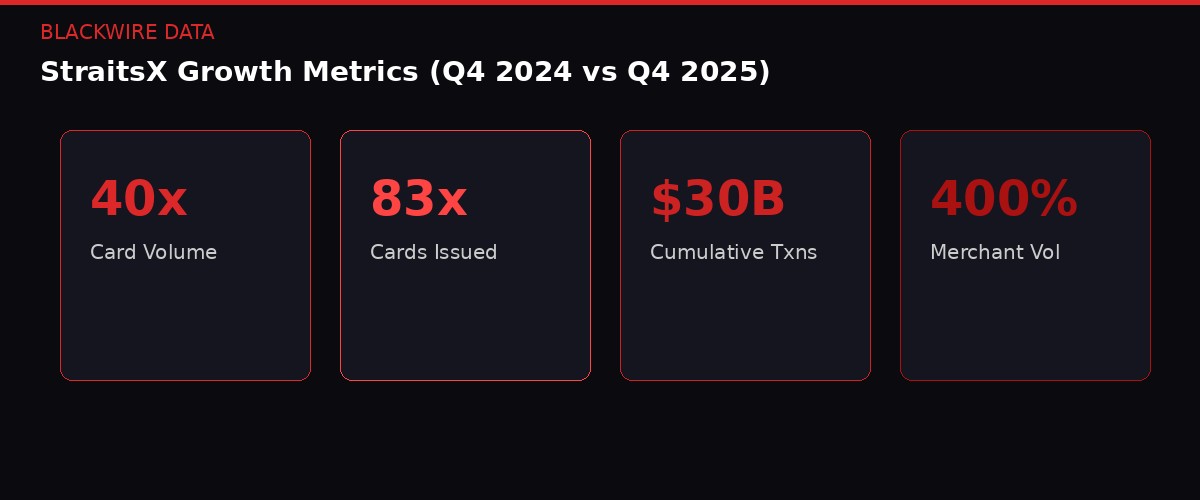

StraitsX key metrics showing explosive growth across every vector. Source: CoinDesk, StraitsX

StraitsX does not build consumer apps. It builds the pipes. The company acts as a Visa BIN sponsor, meaning it provides the underlying infrastructure that allows partners - RedotPay, UPay, and others - to issue cards that settle stablecoin transactions in real time with local fiat arriving instantly on the merchant side.

The model is deliberately invisible. "No user cares about whether a payment runs on stablecoins or fiat; they only care if the payment goes through," CEO Tianwei Liu told CoinDesk.

That philosophy has produced staggering results. The 40x volume surge and 83x card issuance increase between Q4 2024 and Q4 2025 come with important context - their major card partnership with RedotPay only soft-launched in late 2024, making those early quarters a low baseline. But even accounting for that ramp-up effect, the velocity is extraordinary.

StraitsX has now processed nearly $30 billion in cumulative stablecoin transactions. Merchant transaction volume grew 400% recently, with a sixfold jump in unique transacting users month-over-month. These are not vanity metrics from a DeFi dashboard - they represent real people buying real things at real stores.

The company's flagship stablecoin, XSGD, commands more than 70% of the non-USD stablecoin market in Southeast Asia. It maintains a 1:1 peg with the Singapore dollar, backed by monthly audits. That peg gained extra relevance earlier in 2026 when the Singapore dollar hit an 11-year high against the U.S. dollar, making XSGD holders inadvertent FX winners.

"When fees drop close to zero, you can suddenly move very small amounts of money, very frequently," Liu said. "Payments start to look more like internet data flows - continuous, low cost, and embedded directly into applications."

That shift - from payment-as-event to payment-as-stream - is the real thesis behind stablecoin cards. It is not about replacing Visa. It is about making Visa's existing rails carry fundamentally different cargo.

RedotPay's Quiet Empire and the Card Issuer Leaderboard

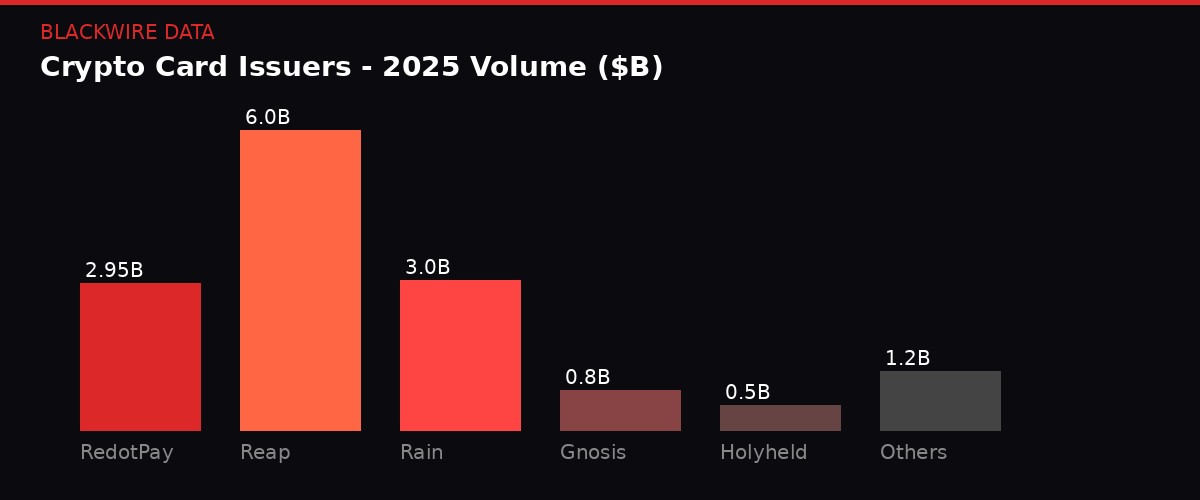

RedotPay dominates the stablecoin card space by transaction volume. Source: Dune Analytics

If StraitsX is the plumbing, RedotPay is the faucet that most consumers actually touch. The Hong Kong-based issuer processed $2.95 billion in card volume in 2025, per Dune Analytics data - a figure that dwarfs every other player in the category combined.

To put that in perspective: the next 13 largest crypto card issuers tracked on-chain collectively moved less than what RedotPay handled alone. The company has built its moat through aggressive geographical expansion, multi-currency support, and a direct partnership with Visa via BIN sponsors like StraitsX.

But RedotPay is not the only player scaling fast. Full-stack crypto card issuers - companies that hold direct Visa principal membership and manage their own settlement rather than relying on BIN sponsors - have posted their own impressive numbers. Rain, a Middle East-focused issuer, reached over $3 billion annualized. Reap, operating across Asia-Pacific, surged past $6 billion annualized. These are not projections or TVL figures. They are settled card transactions at merchants that accept Visa.

The industry structure is stratifying into three tiers. At the top sit full-stack issuers like Rain and Reap with direct Visa membership. In the middle are BIN-sponsored issuers like RedotPay that leverage infrastructure providers like StraitsX. At the bottom are the crypto-native card experiments - Gnosis Pay, Holyheld, and smaller DeFi-integrated products - that have compelling technology but fraction-of-a-percent market share.

Across all tiers, Dune Analytics data shows total on-chain crypto card spending grew 420% in 2025, from roughly $23 million in January to $120 million by December. The compound annual growth rate for the broader industry sits at 106%, per Artemis Analytics.

The competitive dynamic is worth watching closely. RedotPay's volume lead is massive, but full-stack issuers have structural advantages in margin and regulatory positioning. As the U.S. CLARITY Act reshapes the regulatory landscape - more on that shortly - the question of who controls the BIN relationship could determine who survives the next shakeout.

Visa's 90% Lock: The Legacy Giant Wins Again

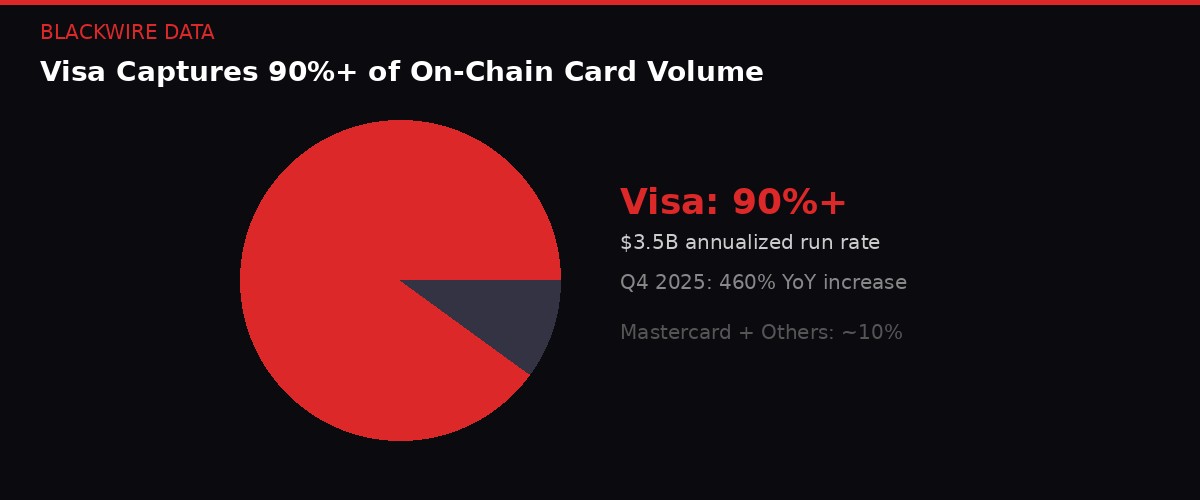

Visa dominates on-chain card volume with $3.5B annualized run rate. Source: Artemis Analytics, Dune

Here is the irony nobody in crypto wants to talk about: the biggest winner of the stablecoin card revolution is a company founded in 1958.

Visa captures over 90% of all on-chain crypto card volume. Its stablecoin-linked card spend reached a $3.5 billion annualized run rate by Q4 2025, a 460% year-over-year increase, per Artemis Analytics research. Mastercard and every other network combined account for the remaining scraps.

Adeline Kim, Visa's Singapore and Brunei country manager, framed it neatly: "It's like driving an electric car versus a car that runs on fuel on the same highway. The vehicle is different, but the road signs, toll booths, and rules don't change."

That analogy is more revealing than Visa might intend. The "road signs and toll booths" are Visa's interchange fees, chargeback infrastructure, and merchant acceptance network - all of which remain firmly under Visa's control regardless of whether the underlying settlement happens in stablecoins or fiat. Crypto changed the engine. Visa still owns the highway.

The implications for crypto's decentralization thesis are awkward. Stablecoin card payments work precisely because they plug into existing centralized rails. The merchant never sees the blockchain. The consumer might not either. The stablecoin is converted to fiat before the receipt prints. Decentralization advocates got a payment revolution - just not the kind they imagined.

Kim told CoinDesk she expects stablecoin cards to evolve beyond utility, with future offerings including real-time spending insights, cross-border perks, and reward systems tailored to user behavior. In other words, Visa's roadmap for stablecoin cards looks identical to its roadmap for regular cards. The blockchain is a backend optimization, not a consumer feature.

For the card networks, this is arguably the best possible outcome. They get the efficiency gains of stablecoin settlement - faster clearing, lower counterparty risk, 24/7 operation - without surrendering any control over the consumer relationship. The "invisible stablecoin" pitch that StraitsX promotes is, from Visa's perspective, exactly the right level of invisibility.

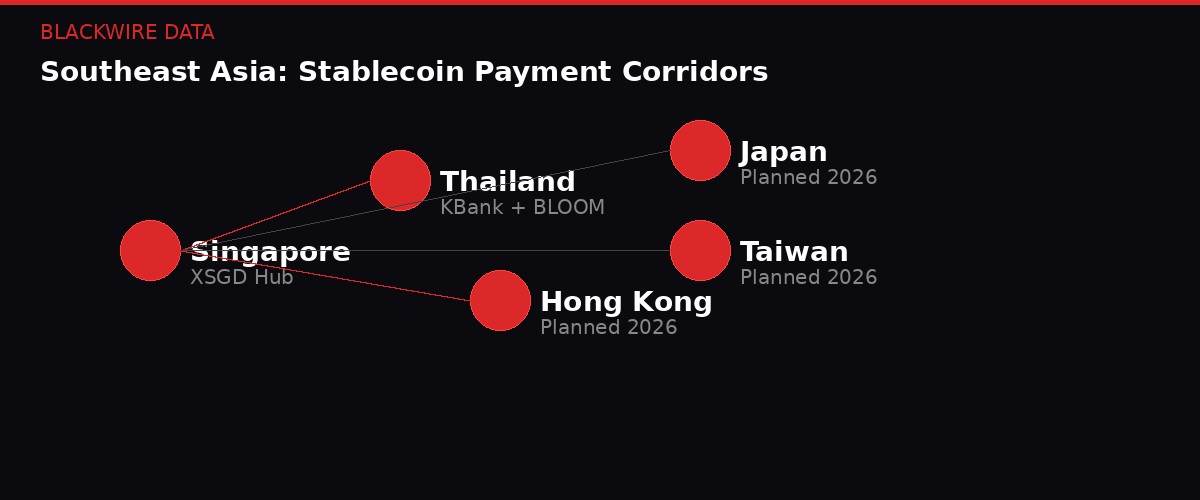

Project BLOOM and the Cross-Border Corridor Play

Active and planned stablecoin payment corridors across Southeast Asia. Source: BLACKWIRE analysis

The next frontier is not card taps. It is cross-border corridors - regulated, government-sanctioned stablecoin bridges between national payment systems.

StraitsX is set to go live under Project BLOOM, a regulatory initiative from Singapore's Monetary Authority of Singapore (MAS). The system will allow Thai travelers to scan QR codes in Singapore using KBank's Q Wallet and pay merchants in their local currency. Behind the scenes, the transaction converts between Thailand's Q-money and StraitsX's XSGD. No exchange booth. No foreign transaction fee. No friction.

This is central bank-blessed stablecoin settlement, not some DeFi experiment. MAS, one of the world's most respected financial regulators, is actively deploying stablecoin infrastructure as part of its national payments strategy. That endorsement carries weight that no amount of crypto Twitter enthusiasm can replicate.

Similar rollouts are planned for Japan, Taiwan, and Hong Kong. Each corridor follows the same playbook: partner with a local e-wallet or banking app, integrate stablecoin settlement in the background, and make the experience indistinguishable from a regular domestic payment.

The model mirrors what already works. GrabPay and Alipay+ integrations required no user retraining and no behavioral change. Users kept doing exactly what they were doing - tapping phones, scanning QR codes - while the underlying settlement shifted from correspondent banking to stablecoin rails.

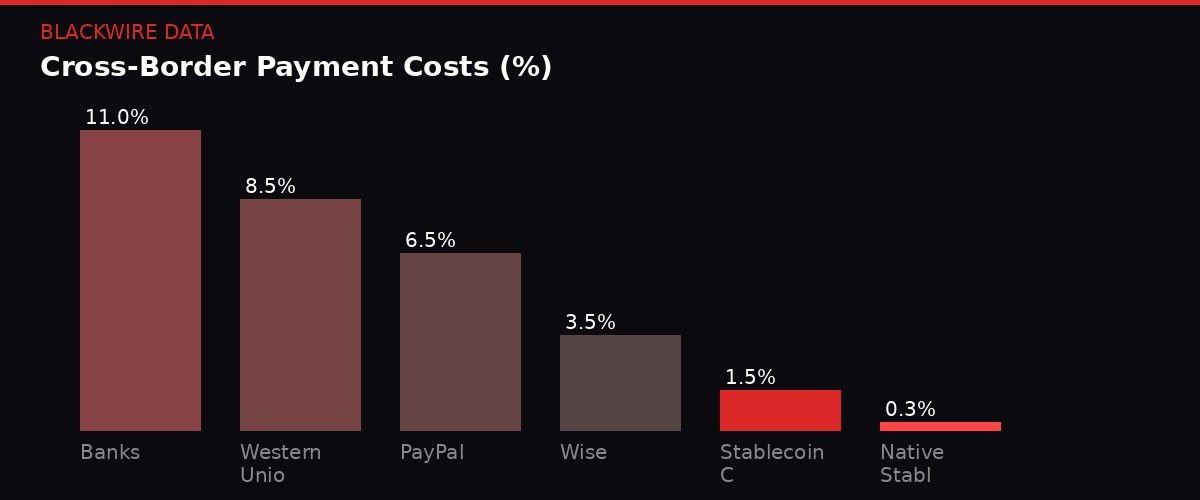

The World Bank estimates that sending $200 internationally still costs an average of 6.49%. For migrant workers sending remittances home - a $700 billion annual market - that fee represents food money, rent money, school fees. Stablecoin cards and corridor payments slash those fees dramatically, in some cases below 1%.

For Southeast Asia specifically, where intra-regional labor migration is massive and financial inclusion remains patchy, stablecoin-powered cross-border payments solve a problem that neither banks nor fintech apps have adequately addressed. The technology exists. The regulatory frameworks are emerging. The only question is speed of adoption.

The CLARITY Act: Washington's Yield Ban Reshapes the Board

The CLARITY Act's stablecoin yield ban creates clear winners and losers. Source: 10x Research, BLACKWIRE

While Asia builds, Washington legislates. And the latest version of the CLARITY Act - the comprehensive crypto market structure bill working its way through the U.S. Senate - contains a provision that could fundamentally reshape the stablecoin landscape: a ban on offering yield on stablecoin balances.

The provision, part of an "agreement-in-principle" announced by Senators Angela Alsobrooks (D-Md.) and Thom Tillis (R-N.C.), would redefine stablecoins as pure payment instruments rather than savings products. No interest. No rewards. No yield of any kind on stablecoin holdings. Period.

Industry representatives saw the language on March 23 and 24. The reaction, per CoinDesk's State of Crypto newsletter, was universal dissatisfaction. Crypto representatives met with legislative staffers on Monday. Banking representatives met Tuesday. Nobody walked out happy.

"This represents a clear re-centralization of yield," wrote Markus Thielen, founder of 10xResearch. The proposal pulls yield back into banks, money market funds, and regulated wrappers, leaving crypto-native platforms with less room to compete on returns.

The logic from Washington is straightforward. Stablecoins that offer yield start to look like securities or bank deposits. Securities require SEC registration. Bank deposits require FDIC insurance and banking charters. By banning yield entirely, Congress sidesteps the classification problem and pushes stablecoins into a clean regulatory box: payment tools, nothing more.

For the stablecoin card industry, the yield ban is paradoxically bullish. If stablecoins cannot compete on returns, they must compete on utility - and payments are the ultimate utility play. Circle's USDC, already positioned as the regulated payment stablecoin, stands to gain the most. StraitsX's infrastructure, built entirely around payment use cases, becomes more valuable, not less.

The losers are DeFi protocols. The initial theory was optimistic: if centralized platforms cannot offer yield, users would migrate on-chain to find it. But Thielen argues the CLARITY framework will likely extend into front-end interfaces and token models, "especially where fee generation or governance starts to resemble equity."

That puts decentralized exchanges like Uniswap, SushiSwap, and dYdX in the crosshairs, alongside lending protocols like Aave and Compound. Tighter constraints on how they operate and distribute value could mean lower volumes, reduced liquidity, and weaker token demand.

Senator Cynthia Lummis (R-Wyo.) said she expects a market structure bill markup - the hearing where lawmakers debate amendments before voting - in the second half of April. Congress goes on Easter recess this week, but the clock is ticking. A counterproposal from industry interests is reportedly in development.

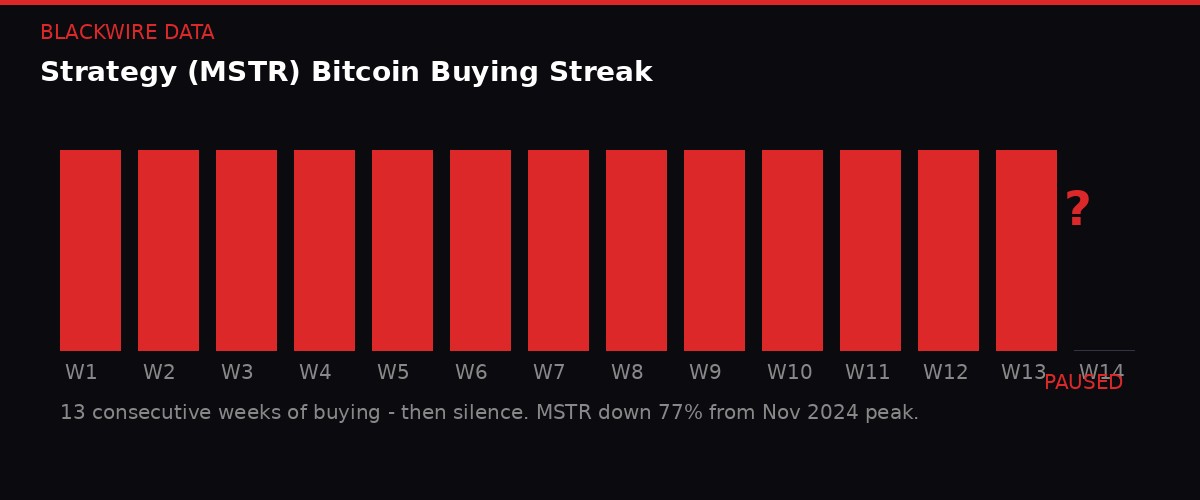

Strategy's Silence and the Bitfinex Contrary Signal

Strategy's 13-week buying streak ends with a pause. MSTR stock down 77% from peak. Source: CoinDesk

The macro backdrop for all of this is hostile. Bitcoin sits at $66,580 as of Sunday evening, trapped in a $65,000-$70,000 range while oil trades at $111 a barrel, the 10-year Treasury yield pushes 4.40%, and markets price in a near-30% chance of a Fed rate HIKE by year-end.

Strategy - formerly MicroStrategy, the company that turned corporate treasury management into a leveraged bitcoin bet - appeared to skip its weekly bitcoin purchase for the first time since late December, ending a 13-consecutive-week buying streak. The company made no announcement. The silence spoke volumes.

MSTR stock is down roughly 77% from its November 2024 peak. The company's bitcoin-treasury strategy, once hailed as visionary, looks increasingly like a momentum trade that worked brilliantly on the way up and is now compounding losses on the way down. When your largest corporate bitcoin buyer goes quiet, the market notices.

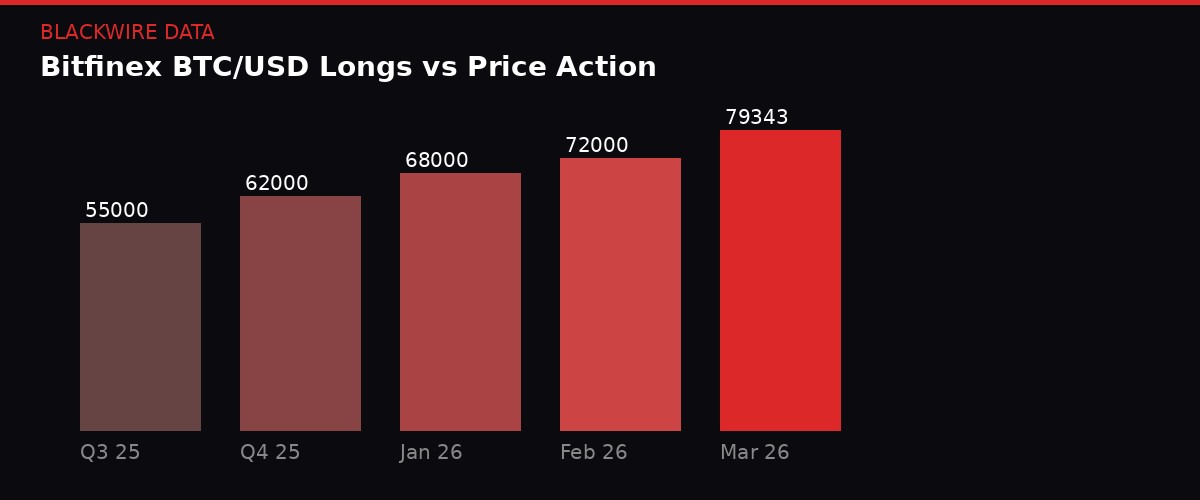

Meanwhile, on Bitfinex - the veteran exchange that has served as a reliable contrary indicator for years - BTC/USD long positions hit 79,343, the highest level since November 2023. History suggests this is bearish. During Q4 2025, Bitfinex longs rose 30% while bitcoin's spot price dropped 23%. The pattern has repeated consistently: price bottoms when longs peak, and rallies when they decline.

Bitfinex longs at 28-month highs - historically a contrary indicator. Source: TradingView, CoinDesk

The crowd, as market analysts like to say, is usually wrong. When retail goes max long, the smart money is typically already positioned for the drop. With oil shock inflation, rate hike fears, and an active war in the Middle East adding to macro uncertainty, the setup favors the bears.

XRP offers another cautionary data point. The token is pinned at $1.33 with rising funding rates and growing leverage suggesting traders are leaning bullish - but repeated rejections near $1.35-$1.36 keep sellers in control. Funding spikes paired with price stagnation typically do not resolve quietly. If $1.33 support breaks, $1.30 comes fast.

Ethereum at $2,008 is struggling to find direction. A new project aimed at fixing the network's layer-2 fragmentation - the sprawl of competing rollups that make the ecosystem feel broken from a user perspective - underscores how far Ethereum remains from the seamless experience that stablecoin card users already enjoy on centralized rails.

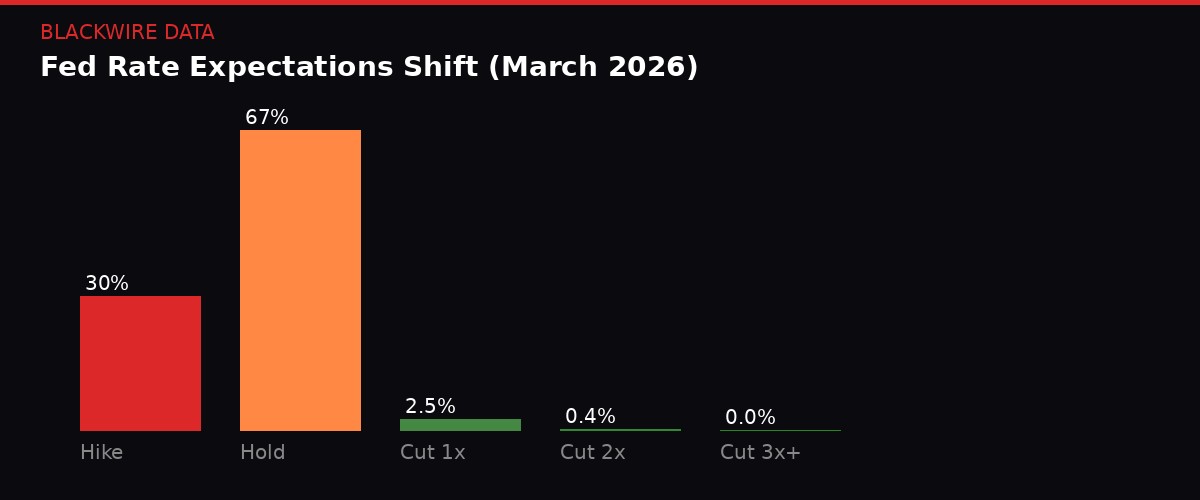

The Fed Flip: From Cuts to Hikes in 30 Days

Rate hike probability has surged to 30% from near-zero in weeks. Source: CME FedWatch

The speed of the monetary policy reversal has been breathtaking. Just weeks ago, markets were pricing in multiple Fed rate cuts for 2026. Now, CME FedWatch data shows a 30% probability that the fed funds rate will be HIGHER by year-end than its current 3.50%-3.75% level. The odds of any rate cut at all have crashed to 2.9%.

The catalyst is oil. Brent crude has surged from $70 per barrel to $111 since the escalation of Middle East tensions at the end of February. That 58% spike in energy costs feeds directly into inflation expectations. Core inflation in February was already running at 2.5% year-over-year, well above the Fed's 2% target. It has not touched that target since April 2021 - five years ago.

Longer-term inflation expectations have also shifted higher, with 5-year breakevens at 2.5% and 10-year at 2.3%. These are market-based measures, not survey opinions. Traders are putting money behind the view that inflation will exceed the Fed's mandate for years to come.

"Food and energy prices are tragically going to climb and remain high for a while, at least until the utter mess of Middle East shipping is sorted out. Even if a peace deal were to be agreed tomorrow (unlikely), that would take months at best." - Crypto is Macro Now Newsletter

The 10-year Treasury yield has ripped to 4.40% from below 4% in a matter of weeks. For risk assets - tech stocks, crypto, growth equity - higher yields mean higher discount rates and lower present values. The Nasdaq entered correction territory on Friday, falling more than 10% from its 2026 highs. Gold, despite being the quintessential safe haven, is down roughly 20% since the U.S. attacks on Iran began - a function of forced selling from leveraged positions and dollar strength.

Bitcoin's "outperformance" during this period is a mirage. Yes, BTC has held roughly steady in the $65,000-$70,000 range while gold and the Nasdaq have fallen. But that comparison ignores the starting positions. Gold had doubled over the preceding year. The Nasdaq was up 50% from its April 2025 lows. Bitcoin was already down 50% from its October 2025 record. The asset that was already beaten down fell less than the assets that were at highs. That is not alpha. That is gravity.

The one genuinely bullish argument for bitcoin in this environment comes from an unexpected angle. Some analysts point to "compressed" valuations - bitcoin trading well below its all-time high while network metrics like hash rate and active addresses remain elevated - as offering reduced downside risk compared to stocks that are just now starting to correct. The logic: there is less air to come out of a balloon that has already deflated.

Whether that compression thesis holds against a genuine rate-hike cycle, $110+ oil, and a Middle East war remains entirely unproven.

The Invisible Thesis: Why Payments Win When Everything Else Breaks

Stablecoin payments slash cross-border costs by 85-95% vs traditional channels. Source: World Bank, BLACKWIRE

Here is the connecting thread through all of this noise: while crypto's speculative layer - the trading, the leverage, the yield farming, the token launches - gets squeezed by macro headwinds and regulatory crackdowns, the payments layer is accelerating.

Stablecoin cards do not need bitcoin at $100,000 to work. They do not need the Fed to cut rates. They do not need the CLARITY Act to pass or fail. They need exactly one thing: people who want to spend money across borders without getting scalped by intermediaries. That demand is not cyclical. It is structural and growing.

The 106% compound annual growth rate in crypto card spending is happening in an environment where bitcoin is down 50%, DeFi yields have compressed, NFTs are effectively dead, and the broader crypto market has been in a grinding bear trend for over a year. The speculative tail is not wagging this dog. The utility is driving itself.

This is why Visa is all-in. This is why MAS is backing Project BLOOM. This is why StraitsX can report 40x volume growth while the rest of crypto argues about whether Bitfinex longs are a sell signal. Different product, different users, different value proposition.

The risk, of course, is regulatory. The CLARITY Act's yield ban might be bullish for payment stablecoins, but Congress has a history of passing legislation with unintended consequences. If the regulatory framework gets too restrictive - if KYC requirements become onerous, if licensing costs become prohibitive, if the yield ban extends to any form of stablecoin innovation - the growth could stall.

There is also competitive risk from central bank digital currencies (CBDCs). Singapore's MAS, the same regulator backing Project BLOOM, has been exploring its own CBDC initiatives. China's digital yuan is already deployed at scale. If CBDCs deliver the same cross-border functionality with state backing, stablecoin cards become redundant infrastructure.

But CBDCs have been perpetually "coming soon" for years now, and the private sector keeps shipping. StraitsX is live. RedotPay is processing billions. Visa cards are in wallets today. CBDCs are in whitepapers and pilot programs. The stablecoin card industry has a massive first-mover advantage in solving a problem that regulators have been talking about addressing for a decade.

The Week Ahead: Macro Landmines and Regulatory Clocks

Congress goes on Easter recess this week, but that pause is deceptive. The CLARITY Act markup is expected in the second half of April, meaning staffers are working through the break to refine language. Industry counterproposals are being drafted. Every lobbyist in Washington with a crypto client is burning weekend hours.

On the macro side, the market will be watching for any signals from the Fed regarding the rate path. With the next FOMC meeting in May, the April data on inflation, employment, and consumer spending will be critical. If oil stays above $100 and core inflation refuses to come down, the rate-hike scenario moves from tail risk to base case.

In crypto-specific developments, Strategy's silence on bitcoin purchases will get louder the longer it lasts. If the company skips a second consecutive week, speculation about balance sheet stress will intensify. MSTR's convertible debt structure - designed for a rising bitcoin environment - looks increasingly fragile in a sideways-to-down market.

For the stablecoin card industry, the StraitsX-Solana deployment of XSGD and XUSD is expected by month-end. If the x402 standard for machine-to-machine micropayments works as advertised, it opens a category of payments that does not exist today: autonomous agents paying other autonomous agents in real time, settling in stablecoins, with no human in the loop.

That might sound like science fiction. But two years ago, so did the idea of a tourist from Bangkok paying a Singaporean street vendor with stablecoins they never knew they were holding.

The invisible is becoming infrastructure. And the market, as usual, is looking at the wrong screen.

Prices as of Sunday March 29, 2026: BTC $66,580 | ETH $2,008 | XRP $1.34 | SOL $82.66 | BNB $613.40 | Brent Crude $111 | 10Y Treasury 4.40%. Sources: CoinDesk, DL News, CME FedWatch, Artemis Analytics, Dune Analytics, World Bank.

Get BLACKWIRE reports first.

Breaking news, investigations, and analysis - straight to your phone.

Join @blackwirenews on Telegram